Your Spreadsheet Shows a 30% Gross Yield. Mississippi's Yazoo Clay, Class II Tax Trap, and Gulf Coast Regulations Show Something Else.

You found a $50,000 house in Jackson pulling $1,200 a month in Section 8 rent. Or a duplex near Keesler Air Force Base with military tenants paying $1,500 on BAH. Or a beachfront rental in Ocean Springs with projected vacation revenue that makes your coastal California property look anemic. The gross rent multiplier is staggering. You're ready to wire earnest money.

Then Mississippi shows up. The Jackson house was owner-occupied — the listed tax bill reflects Class I assessment at 10% plus a homestead exemption. Once you take ownership, the county reclassifies to Class II at 15% with no exemptions, and the tax bill nearly doubles overnight. The duplex sits on the Yazoo Clay Formation — 30 to 40 feet of expansive smectite clay that swells with 25,000 pounds of pressure per square foot when wet and contracts when dry. Slabs crack, plumbing lines shear, doors stop closing. Minor foundation leveling costs $3,000 to $4,500. Moderate to severe piering runs $15,000 to $30,000. The Ocean Springs rental needs three separate insurance policies — landlord dwelling, specialized wind/hail (south of I-10), and FEMA flood — and the combined premiums erase the cash-flow margin your Airbnb calculator promised.

Here's the problem: Mississippi combines the lowest acquisition costs in the nation with a bifurcated property tax system that penalizes investment properties, a geological formation that destroys foundations across the entire Jackson metro, a termite bond system where major corporate providers have been caught skipping chemical barriers and hiking rates 459% to shed liability, attorney-state closing requirements with no centralized title company option, and Gulf Coast municipalities that ban short-term rentals in residential zones and hard-cap total permits at 125 units citywide. Every one of these has cost real investors thousands — not because the information didn't exist, but because it was scattered across county tax assessor portals, BiggerPockets threads from 2019, Biloxi zoning PDFs, and FEMA flood maps that nobody checked before the due diligence period expired.

The Mississippi Investment Property Guide is a Mississippi Investor Due Diligence System — not a motivational overview of real estate investing, but a structured risk-assessment framework that maps every Mississippi-specific tax trap, environmental hazard, regulatory restriction, and closing requirement into a process you work through before you commit capital. It replaces months of cross-referencing county records, municipal zoning ordinances, insurance agent quotes, and forum anecdotes with a single reference that tells you exactly what to verify, exactly what the numbers should look like, and exactly where deals go wrong in this state.

What's Inside the Mississippi Investor Due Diligence System

A 15-chapter guide, a standalone 27-item due diligence checklist, and six printable standalone worksheets and reference cards — covering every stage from market selection through post-purchase operations, built specifically for the geological, fiscal, and regulatory complexity that makes Mississippi different from every other state:

Class I vs. Class II Property Tax Analysis

The single most common underwriting failure in Mississippi real estate investing. When you buy a former owner-occupied home, public records reflect Class I assessment at 10% of true value plus a homestead exemption. The moment you close as an investor, the property is reclassified as Class II — assessed at 15% with no exemptions. On a $100,000 property at 125 mills, the owner's tax was roughly $950. Yours will be $1,875. The guide provides the step-by-step Class II tax calculation using true value, the 15% assessment ratio, and your county's millage rate — so you underwrite your actual tax burden, not the number you see on Zillow or the MLS listing.

Yazoo Clay Foundation Risk Assessment

Central Mississippi sits on the Yazoo Clay Formation — an expansive smectite clay that runs 30 to 40 feet deep and makes over-excavation impossible. The swelling and contraction cycle destabilizes every type of residential foundation, from pier-and-post to slab-on-grade. The damage patterns include slab heaving, plumbing shear lines, wall separation, and doors that permanently misalign. Experienced Jackson investors maintain strict perimeter moisture management protocols to slow the damage, but out-of-state owners who can't train tenants on drainage maintenance face accelerating structural degradation. The guide maps the Yazoo clay exposure zones, the remediation cost tiers from minor leveling ($3,000-$4,500) through full helical pier installation ($15,000-$30,000), and why a structural engineer's foundation inspection — not a general home inspection — is mandatory for every Jackson metro acquisition.

Termite Bond Selection Framework

Mississippi's Gulf Coast is optimal breeding territory for Formosan subterranean termites, and the termite bond you choose determines whether structural damage costs you $0 or $50,000+. A retreat-only bond (starting at ~$495/year) covers zero dollars in structural repair — only re-application of chemicals. A retreat-and-repair bond ($500-$2,500/year) covers both retreatment and physical repairs with caps from $25,000 to over $1,000,000. The guide explains how to select the correct bond, how to verify a provider's treatment history independently after major corporate providers were caught in litigation for skipping complete chemical barriers, and what the pre-closing WDI inspection (NPMA-33 clear termite letter) actually tells you versus what it doesn't.

Gulf Coast Insurance Stack and STR Regulations

Coastal Mississippi requires a three-layer insurance stack that most out-of-state investors fail to model: landlord dwelling policy, specialized wind/hail policy (mandatory south of I-10), and FEMA flood insurance for properties in AE or VE zones. On the regulatory side, Biloxi bans STRs outright in all single-family residential zones and hard-caps conditional-use permits at 125 units citywide with a 4-unit-per-parcel maximum. Gulfport mandates formal registration, $500,000 liability insurance, annual fire inspections, and neighbor notification. The guide provides the insurance modeling framework and the complete zoning map so you know whether your STR thesis is legal before you make an offer.

Six Submarket Deep Dives

Jackson metro (high yield, high risk — the Yazoo clay, crime, and infrastructure story), Madison and Rankin County suburbs (executive-class tenants, strong schools, appreciation play), Gulf Coast (military demand near Keesler AFB, tourism-driven STR revenue, strict zoning), Tupelo (Toyota manufacturing corridor, 7.6% unemployment recovery), Columbus (Columbus AFB and ERDEC demand), and DeSoto County (Memphis spillover, Southaven's population boom). Each section covers current median prices, rental yields, cap rate proxies, economic anchors, and which strategies work — and which ones don't.

Landlord-Tenant Law and Eviction System

Mississippi is one of the most landlord-friendly jurisdictions in the country: no rent control, no security deposit cap, and an eviction timeline that runs two to four weeks from initial default to physical recovery. The 3-day notice to pay or quit, the Justice Court filing and hearing schedule (5-10 days), the immediate Writ of Execution on favorable judgment — every step is mapped out. For investors coming from tenant-friendly states like New York or California, this is a fundamentally different operating environment and one of Mississippi's strongest structural advantages.

Financing, Entity Structure, and Tax Strategy

DSCR loans (no income verification, 80% LTV, $100K minimum loan), community bank portfolio loans through Trustmark, Renasant, and BankPlus for sub-$100K acquisitions, hard money for BRRRR rehab deals, and conventional Fannie/Freddie options with their 10-property limit. Mississippi LLC formation, registered agent requirements, and the critical foreign LLC registration requirement for out-of-state entities — without it, you can't enforce contracts or file evictions in Mississippi courts. The Build-Up Mississippi Act tax schedule showing rates dropping from 4.0% in 2026 to 0% by 2030, plus 1031 exchange conformity with zero transfer tax on the disposition side.

Who This Guide Is For

This guide is for real estate investors targeting Mississippi markets who:

- Are analyzing a Mississippi property and need to verify whether the deal actually works once you account for Class II property tax assessment, Yazoo clay foundation risk, actual insurance costs (including wind/hail and flood layers), and the attorney-closing requirement — not the generic underwriting assumptions that work in states without expansive clay soil and bifurcated tax classifications

- Are evaluating Jackson metro deals and need to understand why a $50,000 property commanding $1,200/month in Section 8 rent still loses money when you factor in foundation piering at $15,000-$30,000, the Class II tax reclassification, and property stripping risk during 48-72 hour vacancies

- Plan to operate short-term rentals on the Gulf Coast and need to verify which zones allow STRs before making an offer, understand the Biloxi 125-unit cap and 4-unit-per-parcel limit, comply with Gulfport's registration and insurance requirements, and model the three-layer insurance stack that determines actual net revenue

- Are an out-of-state investor who needs to register a foreign LLC in Mississippi before you can enforce contracts or file evictions, find an investor-friendly closing attorney (you have the legal right to choose under the Fair Lending Act), and calculate your actual property tax using the Class II formula rather than the Class I number shown on public records

- Are comparing Mississippi against Alabama and Tennessee and need the specific tax, regulatory, and yield differences — Alabama's 10% rental assessment ratio vs. Mississippi's 15%, Tennessee's 0% income tax vs. Mississippi's phase-out to 0% by 2030, and each state's eviction timeline and closing requirements

- Want every Mississippi-specific regulation, tax calculation, environmental risk assessment, and due diligence requirement in one reference — instead of assembling it from county tax assessor websites, FEMA flood maps, BiggerPockets threads, Biloxi zoning PDFs, and pest control litigation records that may be outdated or incomplete

Why Not Free Tools and Forums?

Free information on Mississippi real estate investing exists across dozens of sources. Here's what it actually delivers:

- BiggerPockets forums contain genuinely useful experience reports from Jackson and Gulf Coast investors — alongside polarized arguments where newcomers post spreadsheets showing 30% gross yields and veterans respond with warnings about Yazoo clay, the 2022 water crisis, and $4,000-per-door portfolio liquidations. Sorting current operational intelligence from outdated anecdotes across a dozen threads takes longer than reading a guide that has already verified every procedure against current statute and market data.

- County tax assessor portals show you a parcel's current tax bill. They don't explain that the bill reflects the previous owner's Class I rate with homestead exemption, don't calculate what your Class II liability will be at 15% assessment with no exemptions, and don't quantify the near-doubling that catches every unprepared out-of-state buyer. You get a number without the formula that determines whether your deal actually cash-flows.

- FEMA flood maps and insurance quote tools tell you a property's zone designation. They don't explain the three-layer insurance stack required for Gulf Coast investment property, don't model how combined premiums affect your cash-flow projection, and don't tell you that you can assume a seller's existing NFIP policy at closing to inherit their capped rate. They give you a zone, not an underwriting framework.

- National investing courses ($997 to $5,000+) teach cap rate, DSCR, and 1031 mechanics that apply everywhere. They don't mention Yazoo clay, Mississippi's Class I/II assessment gap, termite bond types and provider litigation history, the Build-Up Mississippi Act income tax phase-out, Gulf Coast STR permit caps, or the attorney-state closing mandate. Applying national frameworks to Mississippi-specific risks is how investors discover five-figure surprises after closing.

This guide fills the Mississippi-specific gap — the space between knowing how to analyze a rental property in general and knowing how to underwrite one in a state where expansive clay destroys foundations, tax reclassification doubles your bill, termite bond selection determines six-figure liability exposure, three insurance layers stack on every coastal property, and municipal zoning caps can make your entire STR thesis illegal. It's the analysis that would take a Mississippi real estate attorney, a structural engineer, a Gulf Coast insurance agent, and a local property manager to assemble — structured as a reference you own permanently.

— Less Than One Foundation Inspection

A single Yazoo clay foundation failure you didn't budget for costs $15,000 to $30,000 in piering — wiping out years of projected cash flow on a low-cost Jackson acquisition. A Class II tax reclassification you didn't calculate adds $900+ per year to your carrying costs for as long as you own the property. A retreat-only termite bond you chose because it was cheaper leaves you fully liable for structural damage that can reach six figures. A Gulf Coast STR you purchased without checking the zoning map is an asset you legally cannot operate for its intended purpose.

This guide doesn't replace your Mississippi closing attorney, your structural engineer, or your insurance agent. But it gives you the Class II tax formula, the Yazoo clay risk assessment framework, the termite bond selection criteria, the Gulf Coast insurance modeling system, and the STR regulatory map that ensure you identify every Mississippi-specific risk before you're contractually committed — instead of discovering them on your first real tax bill, your first foundation crack, or your first zoning violation notice.

If it catches a single tax reclassification, prevents a single under-insured termite bond, or saves you from buying a Jackson property without a foundation contingency budget, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't sharpen your underwriting and protect your capital in Mississippi's unique investment environment, you pay nothing.

Your download includes 8 PDFs: the 15-chapter guide, the 27-item due diligence checklist, plus six standalone tools — a Deal Analysis Worksheet (Class II tax + insurance stack + cash flow model), Submarket Comparison Card, Closing Cost Worksheet, Eviction Timeline Reference, Termite Bond Comparison Card, and Gulf Coast STR Compliance Reference. Print the worksheets and bring them to property inspections, attorney meetings, and insurance agent consultations.

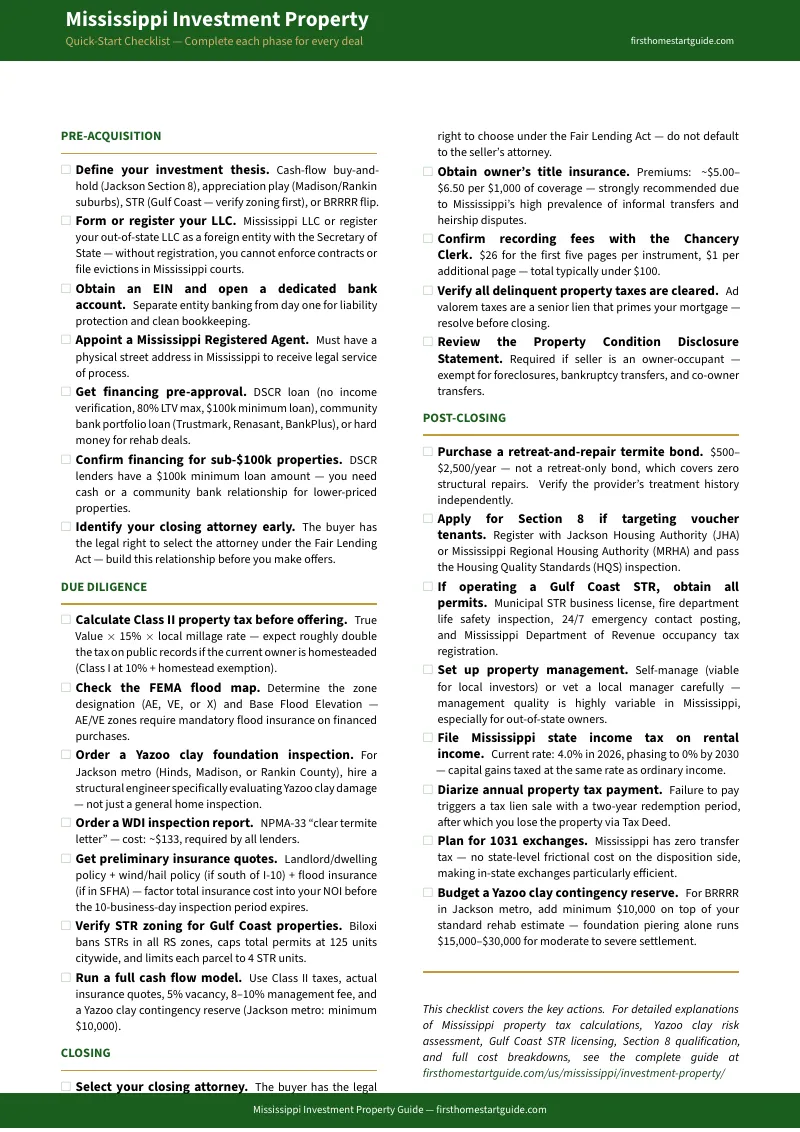

Download the free Mississippi Quick-Start Checklist to see the 27-item due diligence framework covering pre-acquisition research, entity setup, due diligence procedures, closing requirements, and post-closing operations including Section 8 applications and Gulf Coast STR licensing. When you're ready for the full tax analysis, Yazoo clay risk assessment, submarket deep dives, and 15-chapter investment guide, the complete guide is here.

The deal looks good on the spreadsheet. This guide tells you whether Mississippi agrees.