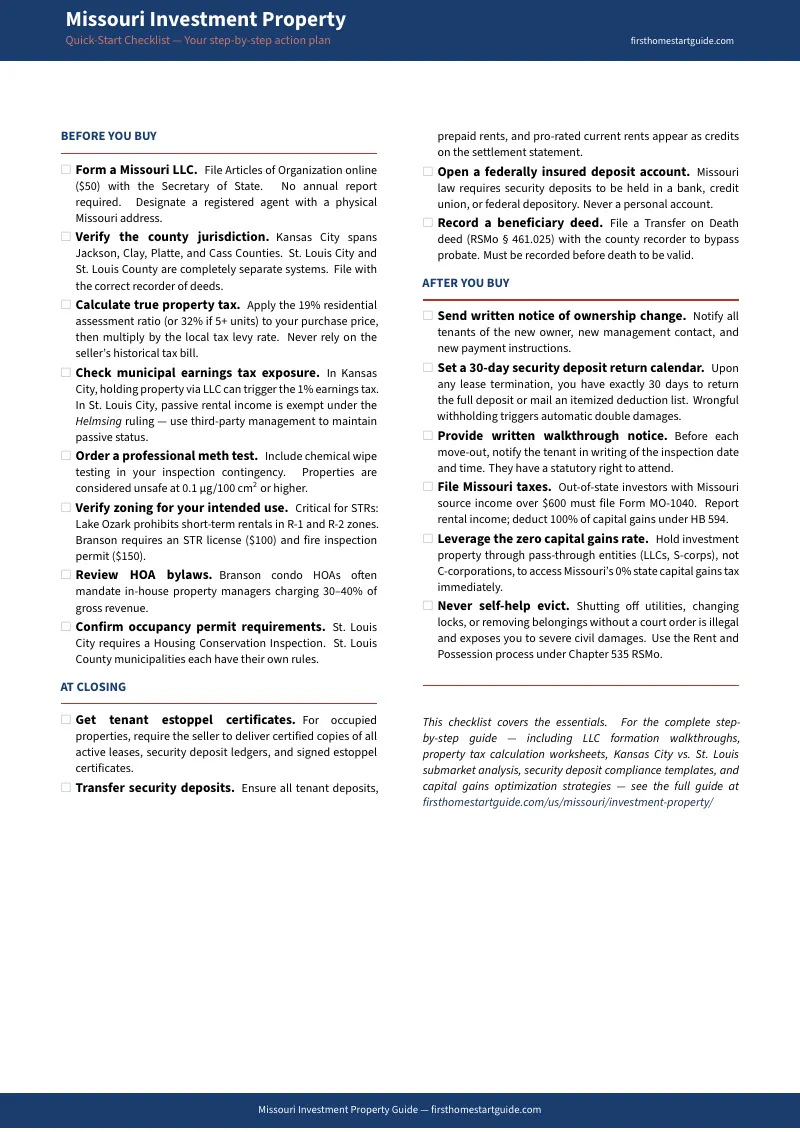

The Spreadsheet Says Cash Flow. The Earnings Tax Says Otherwise.

You found a duplex in Gravois Park throwing off an 8% gross yield against a $145,000 acquisition price. Or a four-family flat in Shaw where the rent-to-price ratio clears the 1% rule and the neighborhood is gentrifying. Or a foreclosure in Independence where the power-of-sale auction delivered a deed for 25% of fair market value and there's no statutory redemption period. The numbers work. The cap rate is solid. You're ready to wire earnest money.

Then you run the real numbers. The Kansas City duplex sits inside city limits, and you formed an LLC to hold it — which triggers Kansas City's 1% municipal earnings tax on your net rental income, even though you have a full-time W-2 job. Across the state line in Overland Park, the same property type in the same metro pays zero municipal earnings tax — but Kansas assesses at 11.5% versus Missouri's 19%, charges a $55 annual LLC report, and imposes a 5.58% state income tax versus Missouri's 4.70%. Meanwhile, the St. Louis City property generates passive rental income that you assumed was exempt under the Helmsing ruling — until you realize you're self-managing tenants and approving every maintenance call, which means you're operating an active trade or business and owe the 1% earnings tax after all. The four-family flat in Shaw crosses the 5-unit commercial threshold if you buy the adjacent duplex — resetting your assessment ratio from 19% to 32% overnight and increasing your annual property tax bill by thousands. The Independence foreclosure closed through non-judicial power of sale in under 60 days, but the prior owner's attorney is now arguing the sale price "shocks the conscience" under Missouri case law, and your title is in limbo until the court rules on the equitable challenge. And the Branson vacation rental that penciled out at $62,000 in annual STR revenue is now subject to a mandatory HOA property management fee of 35% of gross — a $21,700 annual cost that didn't appear on any spreadsheet.

Here's what no single resource explains: Missouri layers a zero-state-capital-gains-tax exit advantage (HB 594, retroactive to January 2025) with a 1% municipal earnings tax in its two largest cities that applies or doesn't based on entity formation decisions and management posture, a property tax assessment system where residential properties are assessed at 19% but the ratio jumps to 32% when you cross the 5-unit commercial threshold, a non-judicial foreclosure process with no statutory redemption that makes acquisition fast but exposes buyers to "shocks the conscience" equitable challenges, a meth contamination disclosure regime with a 0.1 μg/100 cm² threshold that can require $8,000-$15,000 HAZWOPER remediation on an otherwise profitable flip, a security deposit law that imposes automatic double damages for late return and requires FDIC-insured accounts, and a vacation rental regulatory patchwork where Lake Ozark prohibits STRs in residential zones entirely while Branson permits them but HOAs extract 30-40% management fees — into an operating environment that massively rewards investors who structure correctly and punishes everyone who applies generic assumptions from national investing forums.

The Missouri Investment Property Guide is a Show-Me State Underwriting System — not a motivational overview of rental property investing, but a structured due diligence framework that maps every Missouri-specific financial trap, tax advantage, and regulatory requirement into a process you work through before you wire earnest money. It replaces months of cross-referencing RSMo landlord-tenant statutes, county assessor levy tables, Kansas City Revenue Division forms, St. Louis Housing Conservation inspection requirements, and conflicting BiggerPockets threads from 2023 with a single reference that tells you exactly what to verify, exactly what the numbers should look like, and exactly where deals go wrong.

What's Inside the Show-Me State Underwriting System

An 18-chapter guide, a quick-start checklist, and 8 standalone printable tools — covering every stage from entity formation through exit strategies, built specifically for the tax advantages, regulatory traps, and submarket dynamics that make Missouri different from every other state:

HB 594: The Zero Capital Gains Tax Advantage

On July 10, 2025, Governor Kehoe signed House Bill 594, making Missouri the first state to eliminate state capital gains taxes on qualifying capital assets while maintaining a standard income tax. The exemption is retroactive to January 1, 2025. For individual investors and pass-through entities — single-member LLCs, partnerships, S-corporations — this means zero state tax on property sale profits that were previously taxed at up to 4.8%. The guide covers the critical entity structuring requirement: C-corporations remain subject to the 4.0% corporate rate until the individual rate drops to 4.50%, meaning you must hold investment real estate through pass-through entities to access the exemption immediately. It walks through the comparison that makes Missouri's exit economics unique: Illinois sellers pay thousands in transfer taxes plus state capital gains; Kansas sellers pay 5.58% state income tax on gains; Missouri sellers pay zero transfer tax and zero state capital gains tax. On a $200,000 gain, the Missouri advantage over Illinois is $10,000 or more in combined savings.

The 1% Earnings Tax: When It Applies and When It Doesn't

Both Kansas City and St. Louis City impose a 1% municipal earnings tax, but the rules differ between the two cities — and the application depends entirely on how you structure ownership and management. In Kansas City, the Revenue Division evaluates five factors to determine whether rental operations constitute a taxable "business activity": whether you formed an LLC, whether income comes from the regular course of a trade or business, the degree of active management, the volume and frequency of transactions, and the physical time devoted to operations. Forming an LLC specifically to hold a rental property and retaining approval authority over tenants and expenditures triggers the tax — even if you have a separate full-time job. In St. Louis City, the April 2025 Helmsing v. City of St. Louis ruling established that passive rental income is entirely exempt from the earnings tax. "Earnings" under the city's ordinance are strictly limited to active compensation for work or services. Investors who use professional third-party property management and maintain a purely passive posture pay zero municipal earnings tax on St. Louis rental income. Self-managed landlords whose activities cross into active trade or business remain subject. The guide maps the exact structuring decisions that determine whether you owe 1% of net rental income or zero — a difference of thousands annually on a multi-property portfolio.

The Property Tax Assessment System and the Multi-Unit Tax Cliff

Missouri assesses residential property at 19% of appraised value — but the classification shifts to commercial at 32% once a property reaches five or more units. A four-unit building assessed at 19% pays dramatically less property tax than a five-unit building assessed at 32%, even when the per-unit value is identical. The guide covers the parcel-level levy variation that makes Missouri property tax uniquely complex: Kansas City's rate averages $7.49 per $100 assessed value, but the actual rate depends on which combination of school district, fire protection district, and library district overlays the parcel. St. Louis City's rate exceeds $8.00 per $100, while Clayton in St. Louis County runs above $9.00. Across the metro, the exact same structure can face a 30-40% property tax difference depending on which side of a municipal boundary it sits on. The guide provides the three-step calculation — appraised value multiplied by assessment ratio multiplied by total levy rate — and explains why you must calculate from your acquisition price, not from the seller's historical tax bill.

Kansas City State-Line Arbitrage

The Kansas City metro straddles Missouri and Kansas, and every investment decision on the state line involves a direct comparison of regulatory frameworks. The guide maps the complete arbitrage: Missouri's 19% assessment ratio versus Kansas's 11.5%, Missouri's $50 LLC formation with no annual report versus Kansas's $165 formation plus $55 annual report, Missouri's 4.70% income tax versus Kansas's 5.58%, Missouri's zero capital gains versus Kansas's full taxation, and Kansas City MO's 1% earnings tax versus no equivalent on the Kansas side. It covers the school district quality differential — Missouri's 30th-ranked system versus Kansas's 13th — and how that gap affects tenant demand, rent ceilings, and exit pricing by neighborhood. For KC metro investors, the guide makes the cross-border math concrete: same metro, different regulatory frameworks, different returns.

St. Louis City vs. County: The 1876 Split

St. Louis City separated from St. Louis County in 1876 and operates as an independent city with its own assessor, tax structure, and regulatory framework — separate from the 88-90 municipalities that comprise St. Louis County. The guide covers the practical investment implications: Housing Conservation Inspections required for St. Louis City occupancy permits, the earnings tax exemption under Helmsing for passive investors in the city, property tax rates that vary by parcel across the county's patchwork of municipalities and school districts, and the gentrification dynamics in neighborhoods like Gravois Park and Shaw where entry prices remain under $150,000 but appreciation trajectories are accelerating. It maps which St. Louis submarkets favor buy-and-hold cash flow, which favor value-add renovation, and which carry regulatory overhead that erodes returns.

Methamphetamine Contamination Due Diligence

Missouri ranks among the top states for historical meth lab activity, and RSMo § 442.606 requires sellers to disclose known contamination. The guide covers the testing protocol: professional chemical wipe testing during the inspection contingency period, the 0.1 μg/100 cm² threshold established by Crestwood, Missouri as the standard for habitable remediation, and the HAZWOPER-certified remediation process that costs $8,000 to $15,000 depending on contamination severity. It explains why the voluntary disclosure list maintained by the Missouri Department of Natural Resources is incomplete — properties remediated before mandatory reporting fall through the gaps — and why professional testing is non-negotiable on any property with indicators (chemical staining, discoloration, unusual HVAC modifications). Skipping the meth test to save $300-$500 on an otherwise clean inspection can result in a $15,000 remediation bill and potentially unmarketable property.

Landlord-Tenant Law: The Chapter 535 Eviction Framework

Missouri's Rent and Possession statute (Chapter 535 RSMo) governs the eviction process. The guide covers the complete procedural framework: Missouri has no statutory grace period — rent is due on the date specified in the lease. The landlord serves a written demand for unpaid rent (10 days is customary, though the statute is flexible for lease-specified terms), then files a Rent and Possession action in Associate Circuit Court. The court sets a hearing, and if the tenant fails to appear or loses, the court issues a Writ of Restitution directing the sheriff to remove occupants. Total timeline: 3-6 weeks from notice through lockout. The guide covers the security deposit requirements that trip up out-of-state landlords: deposits must be held in a federally insured account, the landlord has exactly 30 days after lease termination to return the deposit or provide an itemized deduction list, and wrongful withholding triggers automatic double damages — twice the amount improperly withheld, plus attorney's fees. It covers the self-help eviction prohibition: changing locks, shutting off utilities, or removing tenant property without a court order exposes the landlord to severe civil liability.

Non-Judicial Foreclosure and Tax Sale Opportunities

Missouri is a power-of-sale state where foreclosure proceeds through the deed of trust rather than the courts, typically completing in under 60 days. Third-party buyers at foreclosure auction receive no statutory redemption period — the prior owner's equity of redemption is extinguished at the sale. The guide covers the legal standard: Missouri courts have upheld sale prices as low as 20-30% of fair market value, applying a "shocks the conscience" test that creates substantial acquisition discounts for investors who understand the threshold. It walks through the trustee's sale mechanics, the notice requirements, the title insurance challenges on foreclosure-acquired properties, and the equitable defenses that prior owners occasionally raise. For tax sale investing, it covers the August auction calendar, the certificate-of-purchase process, the one-year redemption period on tax liens, and the title clearing process required before resale or financing.

Vacation Rental Markets: Branson and Lake of the Ozarks

Missouri's two primary vacation rental markets operate under fundamentally different regulatory frameworks. Lake Ozark prohibits short-term rentals in R-1 and R-2 residential zones, limiting STR operations to commercially zoned properties. Branson is more permissive, requiring an STR license ($100) and fire inspection permit ($150), but HOA-governed condominiums frequently mandate in-house property management at 30-40% of gross revenue — a cost that reduces net operating income by a third or more compared to self-managed STR operations. The guide covers the seasonal cash flow dynamics: peak summer occupancy of 85-95% at Lake of the Ozarks versus 15-25% winter occupancy, Branson's dual-peak pattern around summer tourism and the Christmas season, and the blended annual occupancy rates that determine whether a vacation property cash-flows or requires subsidization from your primary income during shoulder months.

Section 8 Housing, Fix-and-Flip, and Cash Flow Modeling

The guide covers the Kansas City and St. Louis Housing Authority voucher programs — Fair Market Rent ceilings, Housing Quality Standards inspection requirements, the 30-45 day inspection timeline, and the guaranteed payment mechanics that make Section 8 a viable strategy for cash-flow investors in specific Missouri submarkets. The fix-and-flip chapter maps the renovation cost benchmarks for Missouri properties, the city permit and inspection requirements that vary across KC and STL jurisdictions, the holding cost calculations including insurance during renovation, and the exit timing considerations under HB 594's zero capital gains environment. The cash flow modeling chapter provides the complete worksheet: gross rent, vacancy (5-8% for Class B residential, 15-25% for seasonal vacation), property management (8-10% for long-term, 30-40% for Branson HOA-managed STR), property tax using acquisition price and correct assessment ratio, insurance, maintenance reserves, debt service, and the earnings tax variable that depends on your management posture and city of operation.

8 Standalone Printable Tools

Every tool works as a self-contained reference you print and use on every deal — no need to flip through the guide during a closing, an inspection, or a tenant turnover:

- Property Tax Assessment Calculator — fillable worksheet with the three-step calculation, the 4-unit vs. 5-unit tax cliff comparison, and blank rows for your target properties

- Cash Flow Modeling Worksheet — the complete income and expense model with every Missouri-specific line item: earnings tax, correct assessment ratio, HOA STR management fees, and vacancy benchmarks by submarket

- Due Diligence Checklist — 15-item acquisition checklist with checkboxes, grouped by category — print one per property

- Earnings Tax Decision Tree — Kansas City's five-factor Revenue Division test alongside St. Louis City's Helmsing exemption — determine your exposure before entity formation

- Meth Testing Protocol — testing procedure, the 0.1 μg/100 cm² threshold, HAZWOPER remediation costs, and the disclosure safe harbor — bring to every inspection

- Security Deposit Compliance Reference — RSMo § 535.300 rules at a glance: FDIC account mandate, 30-day return deadline, double damages penalty, and a setup checklist

- KC State-Line Comparison — Missouri vs. Kansas side-by-side on income tax, capital gains, property tax, LLC costs, school rankings, and earnings tax exposure

- Eviction Process Timeline — the Chapter 535 Rent and Possession process from rent due date through Writ of Execution, with the KC Tenants Bill of Rights

Who This Guide Is For

This guide is for real estate investors targeting Missouri markets who:

- Are underwriting a Kansas City or St. Louis property and need to understand whether the 1% municipal earnings tax applies to their specific ownership structure and management posture — because forming an LLC in Kansas City can trigger the tax while passive investors in St. Louis City are entirely exempt under the Helmsing ruling, and the structuring decision you make before closing determines your cash flow for the life of the hold

- Are an out-of-state investor from Illinois, California, or the coasts drawn to Missouri's rent-to-price ratios and need the complete operating framework — entity formation, earnings tax exposure, property tax assessment calculation, landlord-tenant compliance, meth contamination testing, and security deposit rules — in one reference instead of fragments scattered across Chapter 535 RSMo, county assessor websites, Kansas City Revenue Division forms, and contradictory BiggerPockets threads

- Are operating in the KC metro and need the state-line arbitrage math: Missouri versus Kansas assessment ratios, income tax rates, LLC maintenance costs, school district rankings, and how each variable compounds across a multi-property portfolio to produce dramatically different after-tax returns on properties separated by a single street

- Are evaluating a St. Louis investment and need to understand the 1876 City-County split — why property tax rates, occupancy permit requirements, and Housing Conservation Inspections vary across 90 independent municipalities, and which neighborhoods offer the strongest entry-price-to-appreciation trajectory

- Are considering a Branson or Lake of the Ozarks vacation rental and need the actual regulatory and cost structure before your revenue model depends on assumptions that don't survive contact with R-1/R-2 zoning prohibitions, mandatory HOA management fees, or seasonal occupancy curves that drop to 15-25% in winter

- Are planning a flip or exit and want to structure it through a pass-through entity to capture HB 594's zero state capital gains tax — combined with Missouri's constitutional prohibition on transfer taxes — for an exit cost structure that no neighboring state can match

- Are acquiring foreclosure or tax sale properties and need to understand the power-of-sale mechanics, the "shocks the conscience" price standard, the absence of statutory redemption for third-party buyers, and the title clearing process required before refinancing or resale

Why Not Free Tools and Forums?

Free information on Missouri real estate investing exists across dozens of sources. Here's what it actually delivers:

- BiggerPockets forums are where someone in a 2022 thread says Kansas City is "the best cash flow market in the Midwest" and someone in 2024 asks why their net income is 1% lower than projected — and nobody identifies the municipal earnings tax as the cause, because the thread doesn't distinguish between properties inside KC city limits and properties in the broader metro. St. Louis threads mention the earnings tax without referencing the Helmsing decision that exempts passive investors, or without explaining what "passive" actually requires in practice. Meth contamination comes up in anecdotes ("I bought a property that tested hot") without the testing protocol, the 0.1 μg/100 cm² threshold, or the $8,000-$15,000 remediation cost range. HB 594 gets mentioned as "Missouri eliminated capital gains!" without the C-corporation exclusion or the pass-through entity requirement. You'll find experience reports from operators who have been doing this for years mixed with advice from people who have never modeled the earnings tax, never ordered a meth wipe test, and never calculated property tax from acquisition price instead of the seller's historical bill. Sorting current from outdated takes longer than reading a guide that has already done it.

- Local REIA meetings — the KC and STL investor associations provide networking with wholesalers, property managers, and hard money lenders. They don't produce comprehensive written guides accessible outside the meeting room, don't provide systematic due diligence frameworks covering the earnings tax structuring, meth testing protocol, security deposit compliance mechanics, or the property tax assessment cliff at five units. You get connections without the regulatory framework.

- National investing books and courses teach cap rate, DSCR, and 1031 mechanics that apply everywhere. They don't mention the KC earnings tax trigger when you form an LLC, the Helmsing exemption for passive STL investors, the 19%-to-32% assessment jump at five units, the meth contamination testing protocol, the constitutional prohibition on transfer taxes, or HB 594's zero capital gains through pass-through entities. Applying national frameworks to Missouri-specific problems is how investors lose five figures on their first deal.

- Turnkey operators sell packaged KC and STL rentals to out-of-state buyers. They quote gross yields and projected cash flow without modeling the earnings tax, without specifying whether the property has been meth-tested, without calculating property tax from your acquisition price instead of the historical bill, and without explaining the occupancy permit requirements in St. Louis City versus the county municipalities. You get a marketed return, not an underwritten one.

This guide fills the Missouri-specific gap — the space between knowing how to analyze a rental property in general and knowing how to underwrite one in a state where a 1% earnings tax that depends on entity formation and management posture, a property tax assessment cliff at five units, a meth contamination regime with $15,000 remediation costs, a zero-state-capital-gains exit through pass-through entities, and a vacation rental patchwork that ranges from outright prohibition to 40% mandatory management fees can each independently determine whether a deal creates wealth or destroys it. It's the analysis that would take a Missouri real estate attorney, a tax advisor, a property manager, and a contamination specialist to assemble — structured as a reference you own permanently.

— Less Than One Earnings Tax Surprise

A single year of the Kansas City earnings tax on a portfolio generating $80,000 in net rental income costs $800 — triggered because you formed an LLC without understanding the Revenue Division's five-factor test. A property tax bill modeled from the seller's historical assessment instead of your acquisition price multiplied by the correct assessment ratio understates your holding costs from year one. A meth-contaminated property purchased without a $300-$500 wipe test during due diligence can require $8,000-$15,000 in HAZWOPER remediation before it's legally habitable. A security deposit returned one day past Missouri's 30-day deadline triggers automatic double damages — twice the amount withheld, plus the tenant's attorney's fees. A Branson vacation rental modeled without the HOA's mandatory 35% management fee overstates your net operating income by $21,700 per year on a $62,000 gross revenue property.

This guide doesn't replace your Missouri real estate attorney, your CPA, or your property manager. But it gives you the earnings tax structuring framework, property tax assessment methodology, meth testing protocol, landlord-tenant compliance system, foreclosure acquisition process, and submarket analysis that ensure you identify every Missouri-specific risk before you're contractually committed — instead of discovering them on your first tax filing, your first tenant turnover, your first meth test, or your first earnings tax audit.

If it catches a single earnings tax structuring error, prevents a single security deposit compliance violation, or saves you from skipping a single meth wipe test, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't sharpen your underwriting and protect your capital in Missouri's operating environment, you pay nothing.

Download the free Missouri Quick-Start Home Buying Checklist to see the due diligence framework covering entity formation, earnings tax exposure, property tax calculation, meth contamination testing, and security deposit compliance. When you're ready for the full earnings tax structuring analysis, submarket mapping, landlord-tenant compliance navigator, and 18-chapter investment guide, the complete guide is here.

The deal looks good on the spreadsheet. This guide tells you whether Missouri agrees.