You found the house. You got pre-approved. Then the closing statement arrived.

A $350 HOA transfer fee. A $185 resale certificate charge. Two months of prepaid dues you never budgeted for. A capital contribution to a reserve fund you did not know existed. And a Clark County transfer tax calculated at a rate 30% higher than the one Google told you about.

None of these fees appeared on the listing. None of them showed up in your mortgage calculator. And your real estate agent did not mention them until the closing disclosure landed three days before signing.

This is buying a home in Nevada. Approximately 77% of residential listings in the Las Vegas Valley are governed by an HOA under NRS Chapter 116. Every one of those transactions comes with administrative fees, layered dues, and reserve fund obligations that first-time buyers consistently fail to budget. The gap between "monthly mortgage payment" and "actual monthly cost of owning this home" is wider in Nevada than in most states — and the buyers who discover it at the closing table are the ones who end up scrambling for cash or watching their deal fall apart.

The Nevada Closing Cost Survival System

The Nevada First-Time Home Buyer Guide is a step-by-step system for navigating every Nevada-specific fee, program, and regulatory quirk that first-time buyers encounter — from HOA transfer fee anatomy to the Assessor's postcard that determines whether your property taxes compound at 3% or 8% for the next decade.

This is not a generic "how to buy a home" pamphlet repackaged with a Nevada label. Every chapter addresses the structural friction that is unique to Nevada real estate: the NRS 116 HOA ecosystem, the Clark County transfer tax surcharge, the FHA condo approval bottleneck, the DPA programs with forgivable and non-forgivable mechanics that are routinely misunderstood, and the desert-specific inspection issues that do not exist anywhere else in the country.

What's Inside

The HOA Financial Anatomy

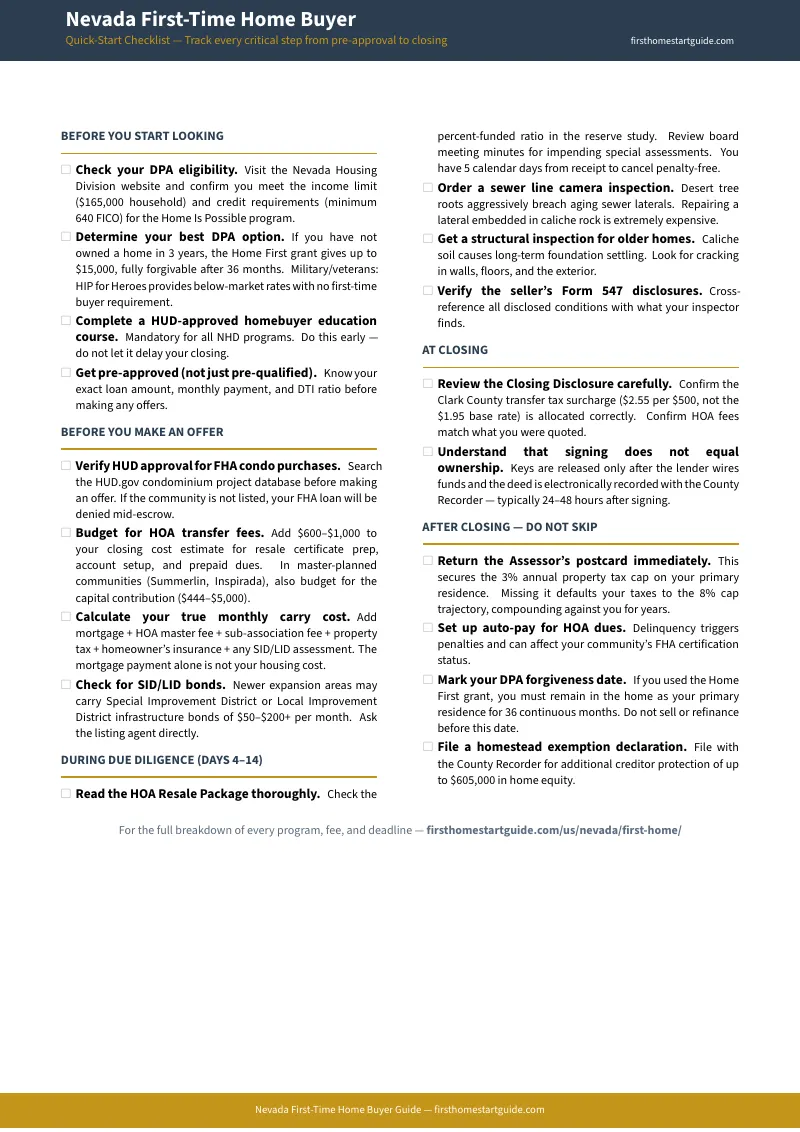

Every closing fee itemized: resale certificate ($185 cap), expedited processing ($100 cap), account setup ($350 base with CPI increases), prepaid dues, and capital contributions ranging from $444 in standard Summerlin neighborhoods to $5,000 in age-qualified communities. The master vs sub-association fee structure explained — because in Summerlin, you pay two HOA bills simultaneously. How to read a reserve study and identify an underfunded HOA before a $10,000 special assessment lands on your doorstep. Your 5-day right of rescission: the contractual exit window that most buyers do not know they have.

Every DPA Program Decoded

The Home Is Possible standard program (non-forgivable, no first-time buyer requirement). The Home First $15,000 forgivable grant (fully forgiven after 36 months). HIP for Heroes (below-market VA rates for military near Nellis and Creech AFB). Worker Advantage ($20,000 for essential workers with a unique rate buydown option). HIP for Teachers ($7,500 forgivable over 5 years). NRHA Home At Last (rural areas). The MCC program pause that eliminates a tax credit new buyers can no longer access. Each program compared side-by-side: who qualifies, how much, forgivable or not, and which loan products they pair with.

The Tax Trap Nobody Mentions

The Clark County transfer tax surcharge: $2.55 per $500 vs the $1.95 base rate that national calculators show. The 3% vs 8% property tax cap and the Assessor's postcard that determines your trajectory. How buying from an investor resets your tax baseline — and the proactive step you must take to fix it. The house-hacking exception that lets landlords qualify for the 3% cap. Worked calculations at $350K, $400K, $480K, and $600K purchase prices.

The FHA Condo Minefield

Why your FHA loan can be denied mid-escrow even if your credit is spotless. The HUD certification requirements that Las Vegas condos routinely fail. How to check approval status before you submit an offer and waste money on appraisals for non-certified communities. The single-unit approval workaround. The condotel warning: properties at Palms Place, The Signature, and Trump International that require exotic financing with shorter terms and higher rates.

Desert Due Diligence

Caliche soil: the sedimentary rock layer beneath the valley that doubles pool excavation costs and creates long-term foundation settling. The sewer line camera inspection you should never skip — desert tree roots aggressively breach aging laterals, and repairing one embedded in caliche rock is devastating. The plumbing trap: subterranean leaks that travel laterally under your slab because caliche prevents absorption, eroding your foundation before you see any surface signs.

The Closing Process, Demystified

Nevada's escrow-based closing timeline from offer to keys (30-45 days). The Grant, Bargain, and Sale Deed — why it gives you less protection than a warranty deed and why title insurance is essential. The critical fact that signing documents does not equal ownership: keys are released only after the lender wires funds and the deed is electronically recorded. Your complete closing cost breakdown for a $350,000 home in Clark County.

Submarket Intelligence

Henderson vs Summerlin vs North Las Vegas — median prices, HOA structures, and which areas fit which buyer profiles. Reno and Washoe County (tech-driven, inventory-constrained). Carson City (growth-limited). Rural Nevada (NRHA-eligible). Condo vs single-family decision framework with financing, HOA, and appreciation trade-offs.

7 Printable Worksheets

Closing cost estimator with Clark County surcharge and HOA line items. NHD program eligibility self-assessment. HOA financial health evaluation worksheet. Property tax cap action plan with 10-year compounding table. Submarket comparison guide. Desert-specific inspection checklist with Form 547 review. Quick-start checklist with all 18 critical steps.

Who It's For

- Las Vegas valley buyers navigating the HOA-dominated landscape for the first time — whether you are looking in Summerlin, Henderson, North Las Vegas, or the urban core

- California transplants who assume no income tax means low overall costs and need to understand the HOA fees, transfer tax surcharges, and property tax mechanics that offset it

- Military families stationed at Nellis or Creech AFB who want to stack VA zero-down financing with HIP for Heroes rates

- Service and hospitality workers who need DPA programs to bridge the gap between their savings and the closing table

- FHA condo buyers who need to verify HUD approval before committing to an offer and losing money

- Remote workers relocating to Reno or Washoe County who face severe inventory constraints and competitive bidding in a tech-driven market

Why Not Just Google It?

The Nevada Housing Division website tells you the income limits for Home Is Possible. It does not tell you that the standard program is non-forgivable while the Home First grant is — a distinction worth $15,000 to buyers who qualify for both.

Zillow and NerdWallet cover "Nevada closing costs" with national averages. They do not mention the Clark County transfer tax surcharge, the HOA capital contribution, or the SID/LID bonds that add $50-$200 per month to your carrying costs in newer expansion areas.

Your real estate agent is incentivized to close the deal. They are not incentivized to teach you how to read a reserve study, identify an underfunded HOA, or exercise your 5-day right of rescission.

This guide consolidates every Nevada-specific variable into one document. It was built from regulatory filings, statutory caps, and the actual fee structures that hit closing tables — not from generic articles recycled with a Las Vegas header image.

Risk-Free Purchase

The guide comes with a satisfaction guarantee. If you do not find it useful, email [email protected] for a full refund.

— Less Than One HOA Transfer Fee

The HOA transfer fee alone on most Las Vegas properties ranges from $350 to over $600. This guide shows you every fee, every program, and every deadline you need to know — for a fraction of a single line item on your closing statement.

Download the free Quick-Start Checklist to see the 18 critical steps, or get the full guide with complete program breakdowns, worksheets, and closing cost calculators.