You Signed the Contract. The Seller Just Raised the Price by $50,000, Your Attorney Has Three Days to Kill the Deal, and the Property Tax Bill You Budgeted Around Belongs to the Previous Owner.

You found a three-bedroom colonial in Maplewood. The listing says $12,500 in annual property taxes. You ran the numbers against your NYC rent, factored in the NJ Transit monthly pass, and the PITI looked doable. You made an offer. Both sides signed the contract. You told your parents. You started measuring rooms on Zillow's floor plan.

Then New Jersey happens. Your attorney calls the next morning and says, "The contract is not binding. We have three business days to review it, and so does their attorney. Either side can cancel for any reason, or no reason at all." You check the listing -- the house is still marked active, and the asking price just went up $50,000. Your agent says that's normal. Meanwhile, your lender calculates your property tax escrow based on the purchase price times Maplewood's effective tax rate, not the seller's old tax bill from a 1998 assessment -- and your monthly payment jumps $400 beyond what you modeled. Then the title search comes back flagging an abandoned underground oil tank in the backyard. Your homeowner's insurance doesn't cover it. Under New Jersey's strict liability statute, you would own the remediation bill the moment you close -- $3,000 to $25,000 depending on whether the tank leaked into the groundwater.

Here's what no single free resource explains: New Jersey layers a mandatory 3-day attorney review period where a signed contract is not binding and the seller can accept a higher offer with zero penalty, against the highest property taxes in America where budgeting from the seller's tax bill instead of the municipal effective tax rate can destroy your monthly affordability by hundreds of dollars, against NJHMFA down payment assistance of $10,000 to $22,000 that is structured as a forgivable zero-interest second mortgage but requires navigating Gold vs. Blue county tiers and First-Generation eligibility and Urban Target Area boundaries that most buyers never check, against strict environmental liability for underground oil tanks where the current owner pays for remediation regardless of who buried the tank, against municipal Certificate of Occupancy requirements that vary from town to town and can derail your closing because the seller's smoke detectors use removable batteries instead of sealed 10-year units, against a 2025 Mansion Tax overhaul that eliminated the buyer's 1% fee but made sellers above $1 million fiercely resistant to price negotiations, against 2024 flood disclosure laws and FEMA Risk Rating 2.0 premiums that escalate 18% annually toward a full-risk rate averaging $2,129/year, against a North-South procedural divide where half the state uses attorneys and the other half doesn't. Each of these has cost real first-time buyers thousands of dollars because the information existed -- scattered across NJHMFA program sheets, municipal CCO websites, NJ Division of Taxation rate tables, NJDEP environmental guidance, FEMA flood maps, and Reddit threads from buyers who went through attorney review four times -- but nobody had assembled it into a single decision system calibrated to how New Jersey actually works.

The New Jersey First-Time Home Buyer Guide is a Garden State Closing Blueprint -- not a generic overview of the home buying process, but a structured reference that maps every NJ-specific legal mechanism, tax calculation, assistance program, environmental liability, and municipal requirement into a process you work through before your earnest money is at risk. It replaces months of cross-referencing NJHMFA income limit matrices, NJ Division of Taxation effective rate tables, municipal CCO requirements, NJDEP oil tank regulations, and forum posts with a single guide that tells you exactly what to verify, exactly what the numbers should look like, and exactly where deals go wrong in this state.

What's Inside the Garden State Closing Blueprint

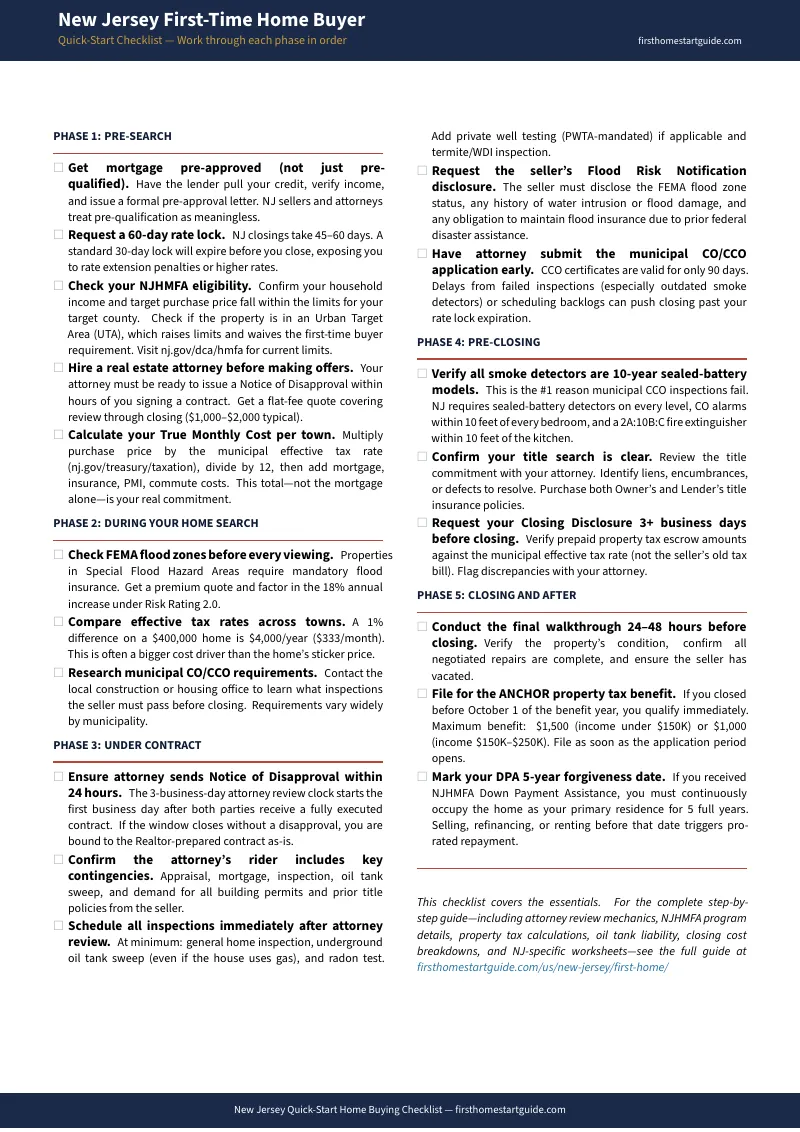

A comprehensive 15-chapter guide, a quick-start checklist, and 3 NJ-specific worksheets -- covering every stage from pre-approval through post-closing, built specifically for the legal mechanisms, tax structures, assistance programs, environmental liabilities, and municipal requirements that make New Jersey the most complex real estate market in the country:

The 3-Day Attorney Review Mechanics

The single most misunderstood part of buying in New Jersey. Every residential contract prepared by a real estate agent includes a mandatory 3-business-day window where either attorney can cancel or rewrite the deal with zero penalty. The guide explains the exact timeline -- when the clock starts, what business days exclude, how the Notice of Disapproval works, and what happens when the 3-day window expires without one filed. It covers what your attorney's rider should add (appraisal contingency, mortgage contingency clarification, inspection contingency, oil tank sweep requirement), the Conley v. Guerrero precedent allowing electronic delivery of disapproval notices, and the critical vulnerability window where the seller can continue showing the home, accept a higher offer, and cancel your deal. Buyers on NJ forums report going through attorney review 3-4 times before successfully closing. The guide prepares you for this reality and shows you how to minimize your exposure.

NJHMFA Down Payment Assistance Decision Framework

New Jersey's primary assistance program provides $10,000 to $15,000 in down payment assistance structured as a zero-interest second mortgage with no monthly payments, fully forgiven after 5 years of owner-occupancy. The guide breaks down the Gold county tier ($15,000 -- Bergen, Essex, Hudson, Hunterdon, Mercer, Middlesex, Monmouth, Morris, Ocean, Passaic, Somerset, Union) versus the Blue county tier ($10,000 -- all others). It covers the First-Generation Homebuyer expansion adding $7,000 on top of the base DPA, bringing the maximum combined assistance to $22,000 in Gold counties and $17,000 in Blue counties. It maps the income and purchase price limits by county grouping and household size, explains how Urban Target Area designations raise both limits and waive the first-time buyer requirement, and walks through the specialized programs: PFRS Mortgage for police and firefighters (below-market rates plus a 6-month rate lock), Homeward Bound, HFA Advantage, and Smart Start. Plus municipal programs in Jersey City (up to $150,000 total subsidy through GNHP), Trenton (up to $20,000), and Newark/Camden.

Property Tax Decoder

New Jersey has the highest property taxes in the nation, and first-time buyers consistently make the catastrophic error of budgeting based on the seller's current tax bill instead of calculating from the purchase price times the municipal effective tax rate. The guide explains the ad valorem assessment system, the critical distinction between assessed value and market value, and why a home that has been in the same family for decades will have its assessed value spike to match your purchase price after a revaluation. It includes town-by-town effective tax rate comparisons showing that a $400,000 home in Bridgeton carries $14,468 in annual taxes while the same purchase price in Far Hills carries $4,888 -- a $798/month difference on identical mortgage payments. It covers Added Assessments (the post-closing supplemental tax bill that arrives when you buy a recently renovated flip or make improvements), the ANCHOR property tax relief program ($1,500 for homeowners earning $150,000 or less), and the Senior Freeze program for multi-generational households.

Underground Oil Tank Liability

New Jersey's environmental liability for underground oil tanks is strict, joint, and several. If an abandoned heating oil tank is on the property and it has leaked, the current owner pays for all remediation costs -- regardless of who buried the tank, who caused the leak, or whether you even knew the tank existed. Standard homeowner's insurance does not cover it. Remediation runs $3,000 to $6,000 for low-level contamination (10-20 cubic yards of soil removal), $6,000 to $12,000 for moderate contamination with lateral soil spread, and $12,000 to $25,000+ when petroleum has reached the groundwater and requires long-term NJDEP monitoring. The guide explains why every property should receive a tank sweep ($250-$400) even if the house currently uses natural gas, how your attorney should make the deal contingent on the sweep results, and the NJDEP "No Further Action" letter process required when contamination is found.

Municipal CO/CCO Requirements

Over 80% of NJ municipalities require a Certificate of Occupancy or Certificate of Continued Occupancy before a home sale can close. The title cannot transfer and you cannot occupy the home until this certificate is issued. Requirements vary wildly -- Cherry Hill enforces extensive exterior inspections, Monroe and Manchester conduct interior safety checks, and Hillsborough requires no CO at all. The guide covers the statewide fire safety mandates (10-year sealed-battery smoke detectors on every level, CO alarms within 10 feet of every bedroom, fire extinguisher in the kitchen) and the sealed-battery smoke detector trap -- the single most common reason CCO inspections fail and closings get delayed. CCO certificates are valid for only 90 days. The guide shows you why your attorney should submit the application immediately after attorney review concludes, before scheduling delays push your closing past your mortgage rate lock expiration.

2025 Mansion Tax Shift

Effective July 2025, the old 1% buyer-paid "Mansion Tax" on purchases over $1,000,000 was eliminated entirely. The new Graduated Percent Fee falls on the seller: 1% on sales between $1M-$2M, 2% on $2M-$2.5M, escalating to 3.5% above $3.5M -- applied to the entire purchase price, not just the amount above the threshold. For buyers, this is a direct savings of $12,000+ at closing on a $1.2 million purchase. But sellers in this range are absorbing massive new costs and are far more resistant to price negotiations, repair credits, and concessions during attorney review. The guide explains how this shift changes buyer negotiation strategy in high-value markets.

Closing Cost Breakdown

NJ closing costs run $8,475 to $13,825 on a $400,000 purchase, and the composition surprises buyers. The largest single line item is prepaid property tax escrow -- 4 to 6 months of taxes pre-funded at closing. At a 2.5% effective tax rate, that's $3,000+ in cash at the closing table just for the escrow baseline. The guide itemizes every buyer cost: attorney fees ($1,000-$2,000), title insurance at promulgated rates (state-set, identical across all title companies), lender origination and appraisal fees, land survey, recording fees, and inspections. It explains the Realty Transfer Fee schedule (seller's responsibility on resale homes, but routinely shifted to the buyer on new construction), and covers the NJ Bargain and Sale Deed -- why its limited warranty means you need Owner's Title Insurance.

Flood Disclosure and Insurance

The 2024 Flood Risk Notification Law requires sellers to disclose FEMA flood zone status, any prior water intrusion or flood insurance claims, and any legal obligation to maintain flood insurance permanently. The guide explains FEMA's Risk Rating 2.0 framework, which moved from broad zone-based pricing to property-specific risk analysis. In New Jersey, 64% of existing NFIP policyholders saw premium increases. The average risk-based cost is approximately $2,129/year -- a 97% increase from historical subsidized premiums. Congressional caps limit annual increases to 18%, creating a multi-year "glide path" where your flood insurance costs can nearly triple within 5-7 years. The guide shows you how to factor this escalation into your 5-year and 10-year affordability projections before you make an offer on a shore or riverine property.

Private Well Testing Act (PWTA)

If the property uses a private well, the seller is legally required to test the water and provide certified lab results at least 30 days before closing. Required testing parameters include Total Coliform, Nitrates, Lead, Arsenic, PFAS ("forever chemicals"), and Gross Alpha Particle Activity -- plus Mercury in southern counties and Uranium in northern counties. Closing cannot legally occur until both parties sign a certification acknowledging receipt. The guide covers the remediation cost ranges ($1,500 for standard filtration to $10,000+ for complex reverse osmosis systems) and how to negotiate treatment costs before you're contractually committed.

NYC Expatriate Calculus

If you're migrating from New York City to the New Jersey suburbs, the guide dismantles the rent-vs-mortgage comparison that convinces buyers they're saving money. It maps the full cost of suburban ownership: mortgage payment plus property taxes ($600-$1,200+/month), NJ Transit monthly pass ($200-$450 by zone), station parking ($50-$150/month), and vehicle ownership costs ($800-$1,600/month per car) that didn't exist in your NYC budget. The suburban transportation stack alone can run $1,000-$2,000 per month. The guide covers the hybrid work adjustment (commuting 2-3 days changes the math significantly), transit-adjacent town recommendations by rail line (Morris & Essex, Northeast Corridor, North Jersey Coast, Montclair-Boonton), and the Three-Variable Framework for choosing towns: effective tax rate, total commute cost, and school district quality.

NJ-Specific Worksheets

Three standalone worksheets you can print and use immediately:

- True Monthly Cost Calculator -- Goes beyond PITI to include property taxes calculated from the effective tax rate, flood insurance, NJ Transit pass, station parking, vehicle costs, and utilities. Includes the 40% gross income test that catches the overextension your lender's DTI ratio misses.

- NJHMFA Eligibility Checker -- Six-question assessment covering ownership history, credit score, occupancy timeline, income limits, purchase price limits, and homebuyer education requirement. Identifies your DPA amount by county tier and First-Generation eligibility.

- Closing Cost Estimator -- Fillable worksheet itemizing every NJ-specific cost: attorney fees, title insurance at promulgated rates, lender fees, land survey, inspections (general + oil tank sweep + radon), prepaid tax escrow, and the net cash-to-close after DPA and seller credits.

Who This Guide Is For

This guide is for first-time home buyers in New Jersey who:

- Are leaving a New York City rental and crossing the Hudson -- and need to understand why comparing your $3,500/month rent to a NJ mortgage payment will lead you to overextend, how the suburban transportation stack adds $1,000-$2,000/month to costs you've never carried, which NJ Transit rail-line towns balance tax rates against commute times for hybrid workers, and why the seller's listed tax bill is irrelevant to what you'll actually pay

- Are buying in South Jersey and wondering whether you even need an attorney -- and need to know why the Burlington/Camden/Gloucester closing process skips attorney review entirely, how the procedural simplicity creates different risks around title defects and contract terms, and why the effective tax rates in South Jersey municipalities can be statistically higher than affluent North Jersey towns despite lower home values

- Are targeting NJHMFA down payment assistance and can't figure out whether you qualify -- and need the income and purchase price limits decoded by county grouping and household size, the Gold vs. Blue tier DPA amounts compared, the First-Generation $7,000 expansion explained, and the Urban Target Area boundaries that raise the limits and waive the first-time buyer requirement

- Are buying near the Jersey Shore or along a riverine floodplain -- and need to understand the 2024 Flood Risk Notification disclosure requirements, how Risk Rating 2.0 calculates your specific premium, the 18% annual increase glide path that can triple your flood insurance within 5-7 years, and why standard homeowner's insurance covers zero flood damage even from one inch of water

- Are a NJ Transit commuter targeting towns along the Morris & Essex, Northeast Corridor, or North Jersey Coast lines -- and want the effective tax rate comparisons, commute cost calculations, and school district quality assessments for each corridor so you can choose a town based on total monthly cost, not listing price alone

- Want every NJ-specific legal mechanism, tax calculation, assistance program, environmental liability, and municipal requirement in one reference -- instead of assembling it from NJHMFA fact sheets, municipal CCO websites, NJ Division of Taxation rate tables, NJDEP oil tank guidance, FEMA flood maps, and Reddit threads designed to vent frustration, not structure a transaction

Why Not Free Tools and Forums?

Free information on buying a home in New Jersey exists. Here's what it actually delivers:

- NJHMFA's website publishes program guidelines, income limits, and county-specific fact sheets. It doesn't explain the strategic difference between Gold and Blue county DPA tiers, doesn't show how to stack the First-Generation $7,000 expansion with the base DPA to reach $22,000 in forgivable assistance, and doesn't map which properties fall inside Urban Target Area boundaries that raise both income and purchase price limits. You get program specifications without a decision framework for using them.

- Zillow and Realtor.com show estimated monthly payments using approximate tax figures. In a state where the effective tax rate ranges from 0.79% in Alpine to 3.62% in Bridgeton, and where the seller's listed tax bill may reflect a decades-old assessment that will spike to match your purchase price, those estimates can be off by $500-$800/month. No listing site warns you about Added Assessments, oil tank liability, or the 90-day CCO validity window. You get a number that looks affordable and may not be.

- Real estate agent blogs highlight charming downtowns, top school districts, and NJ Transit convenience. They don't explain that your signed contract is non-binding for three business days, don't mention that the seller can accept a higher offer during attorney review with zero penalty, and never discuss the strict environmental liability that transfers with the deed if an underground oil tank is found. The content generates leads. It doesn't identify reasons to slow down.

- Reddit threads (r/newjersey, r/FirstTimeHomeBuyer) contain genuine buyer experiences -- attorney review horror stories, property tax shock, oil tank nightmares, CCO inspection failures. But advice from 2023 doesn't reflect the 2025 Mansion Tax shift, current NJHMFA income limits, or the 2024 Flood Risk Notification Law. One buyer documented going through attorney review four separate times, losing thousands in accumulated legal fees. The emotional resonance is real, but sorting current guidance from outdated venting takes longer than reading a guide that has already done it.

This guide fills the New Jersey-specific gap -- the space between knowing how to buy a house in general and knowing how to buy one in a state where signing a contract doesn't mean you bought the house, where property taxes can exceed $14,000/year on a $400,000 home, where an underground oil tank you never knew about can cost you $25,000 in remediation, where your closing can stall because a smoke detector has a removable battery, and where $22,000 in forgivable down payment assistance is available but requires navigating a matrix of county tiers, income limits, and Urban Target Area boundaries that most buyers never decode. It's the analysis that would take a NJ real estate attorney, an NJHMFA-approved lender, and a certified appraiser to assemble -- structured as a reference you own permanently.

-- Less Than One Hour With a NJ Real Estate Attorney

A New Jersey real estate attorney charges $1,000 to $2,000 for review through closing. An underground oil tank remediation runs $3,000 to $25,000. Budgeting from the seller's old tax bill instead of the municipal effective tax rate can blindside you with $400-$800/month more than you planned. Missing the NJHMFA First-Generation expansion means leaving $7,000 in forgivable assistance on the table. Letting the 3-day attorney review window lapse without filing a Notice of Disapproval locks you into a Realtor-prepared contract that may lack appraisal, inspection, and oil tank contingencies.

This guide doesn't replace your real estate attorney or your lender. But it gives you the attorney review mechanics, NJHMFA program analysis, property tax calculations, oil tank liability guidance, municipal CCO requirements, flood disclosure framework, and closing cost breakdown that ensure you identify every New Jersey-specific risk before your earnest money is committed -- instead of discovering them during attorney review, on your first quarterly tax bill, or when a municipal inspector fails your closing over a smoke detector.

If it catches a single property tax miscalculation, prevents a single oil tank surprise, or helps you claim $22,000 in forgivable assistance you qualified for, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't sharpen your decision-making and protect your investment in America's most complex real estate market, you pay nothing.

Download the free New Jersey Quick-Start Home Buying Checklist to see the action plan covering pre-approval, attorney selection, property search, closing preparation, and post-closing protection. When you're ready for the full attorney review mechanics, NJHMFA decision framework, property tax decoder, oil tank liability guidance, and closing cost breakdown, the complete guide is here.

The house looks perfect on Zillow. This guide tells you whether New Jersey agrees.