Your Lender Will Pre-Approve You. Nobody Will Mention That Your Spouse's Car Loan Just Killed Your FHA Qualification.

You have checked the MFA website and compared FIRSTHome rates. You have browsed Zillow listings in Albuquerque, scrolled through Santa Fe prices wondering if anything under $400,000 exists, and read Reddit threads about whether USDA loans work in Las Cruces. But nobody has explained that buying a house in New Mexico as a married couple means your spouse's debts count against your mortgage qualification on every government-backed loan — even if your spouse is not on the mortgage, not on the title, and has no intention of ever being on either.

New Mexico is not a difficult state to buy a home in. It is a difficult state to buy a home in correctly. The real estate market is shaped by community property laws that void any mortgage signed without both spouses present, land grants from the 1600s that can freeze your ability to sell or refinance overnight, water rights that are legally separate from the land and carry mandatory labor obligations, and adobe construction that collapses from the inside when wrapped in the wrong stucco. Add an MFA system with two different down payment assistance programs that have completely different forgiveness terms — and you have a state where the cost of not knowing one rule can exceed the cost of the house itself.

Here is the core problem: New Mexico layers a community property spousal-debt mandate, Spanish-colonial land grant title disputes, prior-appropriation water rights with acequia labor obligations, mandatory adobe-specific inspections, and an MFA system with three overlapping programs — and the free resources that cover each topic are scattered across the MFA website, county assessor portals, Office of the State Engineer databases, Reddit threads, and broker blogs that each explain one piece without connecting it to the rest. There is no single resource that maps how community property law affects your DTI calculation, how land grants interact with title insurance, how to verify water rights through the OSE before you lose your earnest money, or how cement stucco traps can turn a $300,000 adobe home into a $450,000 remediation project. Until now.

The New Mexico First-Time Home Buyer Guide is a New Mexico Buyer Navigation System — a structured decision framework that connects every New Mexico-specific legal trap, financial program, and property risk into a single step-by-step roadmap from pre-approval through key collection.

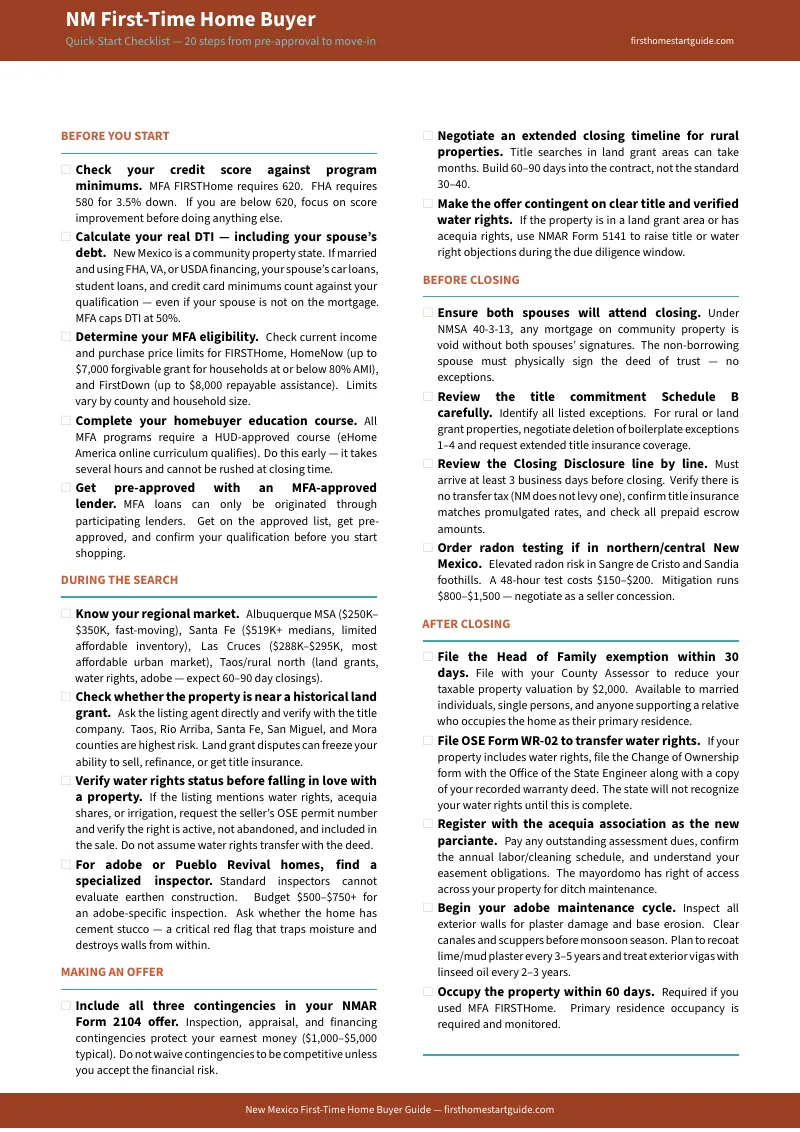

What's Inside the New Mexico Buyer Navigation System

A 13-chapter guide, a printable quick-start checklist, and 5 standalone worksheets — covering every stage from calculating your real spousal-debt DTI through post-purchase acequia registration, plus the adobe inspection protocol and land grant due diligence process you will not find anywhere else:

Community Property Laws and the Spousal DTI Trap

New Mexico is one of nine community property states. Under NMSA 40-3-13, any mortgage on community real property signed by only one spouse is void and of no effect. But the real trap is not at closing — it is during underwriting. If you are married and applying for an FHA, VA, or USDA loan, your lender is federally required to pull your non-borrowing spouse's credit report and add every one of their monthly debt payments to your DTI calculation. Your spouse's $350 car payment and $150 credit card minimums can disqualify you from the MFA's 50% DTI ceiling before the mortgage amount even enters the picture. The guide includes a worked DTI example showing exactly how this calculation works, when to pursue a conventional loan instead, and how to structure debt paydown before applying.

Land Grant Title Complexity and Quiet Title Actions

In northern New Mexico — Taos, Rio Arriba, Santa Fe, San Miguel, and Mora counties — property titles intersect with Spanish and Mexican land grants dating back to the 1600s. In Arroyo Hondo, a land grant board filed warranty deeds claiming 20,000 acres of private land, paralyzing hundreds of homeowners who could no longer sell, refinance, or get title insurance. Standard title searches go back 40 to 60 years and will not catch these claims. The guide covers deep chain-of-title searches, quiet title actions under NMSA 42-6-1, how to negotiate deletion of boilerplate exceptions 1-4 from your title insurance policy, and why extended title insurance is not optional in these counties.

Water Rights and Acequia Obligations

Water rights in New Mexico are legally separate from the land. Owning property with an irrigation ditch does not mean you own the right to use the water. Under the Doctrine of Prior Appropriation, the Office of the State Engineer controls all water rights, and those rights can be severed from the land and sold separately. If the previous owner stopped irrigating, the rights may have been abandoned and permanently forfeited. If you buy irrigated land without verifying the water rights through the OSE, you may have purchased dry, barren acreage at irrigated-land prices. And if you become a parciante on an acequia, you owe annual dues, mandatory spring ditch-cleaning labor, and unrestricted easement access to the mayordomo across your property. The guide covers OSE record verification, the use-it-or-lose-it forfeiture rule, acequia governance, and how to make your offer contingent on verified water rights.

Adobe and Pueblo Revival Inspection Protocol

Adobe homes are culturally iconic and thermally efficient. They are also structurally vulnerable in ways that standard home inspectors cannot evaluate. The singular greatest threat is moisture: cement stucco applied over breathable earthen walls traps water inside the adobe matrix, causing matric suction to plummet from 30 MPa to 0.03 MPa. The walls soften, bulge outward, and fail. The guide provides a complete adobe-specific inspection checklist covering base erosion, efflorescence, cement stucco identification, flat roof drainage, viga degradation, and seismic bond beam verification — plus how to budget $500-$750+ for a specialist inspector and what to negotiate as seller concessions.

MFA Programs: FIRSTHome, HomeNow, and FirstDown

The MFA runs the most important first-time buyer programs in the state, but the eligibility matrices are dense and the two down payment assistance programs have completely different terms. HomeNow provides up to $7,000 as a 0% interest non-amortizing loan with full forgiveness after 10 years — if you do not sell, refinance, or transfer. FirstDown provides up to $8,000 but as real debt with amortizing payments. Income limits vary by county and household size. The guide translates the MFA tables into a diagnostic workflow, covers how to pair these programs with FHA, VA, USDA, and conventional financing, and explains the $500 minimum borrower contribution and the 50% DTI ceiling that trips up most applicants.

Regional Market Analysis

New Mexico is three distinct housing markets. Albuquerque MSA ($250K-$350K, military and tech employment, fast-moving inventory). Santa Fe ($519K+ medians, severe affordability constraints, tourism and government economy). Las Cruces and southern New Mexico ($288K-$295K, most affordable urban market, strong NMSU and military base employment). Taos and rural north (land grants, acequia water systems, adobe construction, 60-90 day closings). The guide maps each market with price ranges, buyer challenges, dominant loan products, and location-specific strategies.

Closing Process, Costs, and Tax Advantages

New Mexico uses title companies for closings, not attorneys. There is no state real estate transfer tax — which means free closing cost calculators built for other states overestimate your cash to close. Property is assessed at one-third of market value, and the Head of Family exemption reduces your taxable valuation by a further $2,000. The guide provides an itemized closing cost breakdown, explains the title insurance rate schedule (promulgated statewide), and covers the Head of Family exemption filing deadline so you do not miss the window.

Who This Guide Is For

This guide is for first-time buyers in New Mexico who:

- Are married and need to understand how community property law will affect their mortgage qualification — specifically how a non-borrowing spouse's debts get factored into DTI on FHA, VA, and USDA loans, why both spouses must physically attend closing, and when a conventional loan is the better path

- Are looking at properties in northern New Mexico — Taos, Rio Arriba, Santa Fe, San Miguel, or Mora counties — and need to understand land grant title risks, quiet title actions, and why standard title insurance coverage is not sufficient

- Are buying rural property with water rights or acequia access and need to verify the rights through the OSE, understand their obligations as a parciante, and protect their earnest money with proper contract contingencies

- Are considering an adobe or Pueblo Revival home and need an inspection protocol that goes beyond what a standard home inspector can evaluate — covering cement stucco traps, base erosion, viga degradation, flat roof drainage, and seismic bond beams

- Are military families at Kirtland AFB, Sandia National Laboratories, or White Sands Missile Range who need to navigate VA loan community property requirements and understand which MFA programs they qualify for

- Want to maximize MFA down payment assistance and need a clear map of how FIRSTHome, HomeNow, and FirstDown interact — including the income limits by county, the forgiveness terms, and the 50% DTI ceiling

- Want every cost, every deadline, every statute, and every decision point in one document — so they walk into lender meetings, title company appointments, and property viewings knowing exactly what to ask and what to verify

Why Not Free Resources?

Free information on buying your first home in New Mexico is everywhere. Here is what each source actually delivers:

- New Mexico Mortgage Finance Authority (housingnm.org) publishes program parameters — loan types, income limits, purchase price caps. What it does not do: explain how community property law interacts with FIRSTHome eligibility, how to calculate your real DTI when spousal debt is included, how HomeNow's 10-year cliff forgiveness differs from FirstDown's amortizing repayment, or which MFA-approved lenders actually process these loans efficiently. The eligibility tables are there. The decision framework for choosing and combining programs is not.

- Office of the State Engineer (ose.nm.gov) maintains the state water rights database. It does not explain to a first-time buyer how to verify whether a seller's advertised water rights are active, abandoned, or already severed and sold to a municipality. It does not explain the use-it-or-lose-it forfeiture rule, the acequia governance structure, or how to make an offer contingent on verified water rights. The database is there. The buyer's due diligence process is not.

- Reddit (r/NewMexico, r/Albuquerque, r/FirstTimeHomeBuyer) is where real New Mexico buyers share unfiltered experience — and where someone's 2022 advice about MFA income limits sits alongside current numbers, where "water rights transfer with the deed" is posted by people who have never checked an OSE record, and where "adobe homes are fine, just get a regular inspection" comes from owners who have never dealt with moisture-trapped cement stucco. The signal is real. So is the noise.

- Local real estate agent blogs cover market conditions with genuine local insight — from the perspective of professionals who earn a commission when you buy. They will tell you to "get pre-approved" and "move fast in Albuquerque" but will rarely walk you through the community property DTI calculation, the land grant quiet title process, or the acequia labor obligations — because those topics slow deals down and do not generate referral fees.

This guide fills the navigation gap — the space between knowing New Mexico has community property law, land grants, water rights, and adobe construction, and understanding how they all interact across a single home purchase. It is the analysis an independent advisor with no commission to earn would give you, structured as a permanent reference you own.

— Less Than One Hour of a Specialized Adobe Inspector's Time

A specialist adobe inspection costs $500 to $750. A quiet title action in a land grant area costs $3,000 to $10,000 and takes 6 to 12 months. Purchasing irrigated land without verified water rights means paying irrigated-land prices for dry acreage. A non-borrowing spouse's hidden debt can disqualify you from an FHA loan three weeks into underwriting — after you have paid for the appraisal, the inspection, and the earnest money deposit.

This guide does not replace your lender, your title company, or your real estate agent. But it gives you the community property DTI calculation, the land grant due diligence protocol, the water rights verification process, the adobe inspection checklist, and the MFA program comparison that ensure you walk into every appointment knowing exactly what to ask, exactly what to verify, and exactly what to insist on — instead of discovering expensive traps in real time.

If it prevents a single spousal-debt DTI surprise, catches a land grant title defect before closing, or saves you from purchasing dry land at irrigated prices, it pays for itself before you have finished reading it.

30-day money-back guarantee. If the guide does not make your New Mexico home buying process clearer and your financial position stronger, you pay nothing.

Download the free New Mexico Quick-Start Checklist to see the step-by-step action plan covering community property requirements, land grant title verification, water rights due diligence, and MFA program eligibility. When you are ready for the full navigation system — complete with the DTI calculator, MFA eligibility worksheet, closing cost estimator, adobe inspection checklist, water rights tracker, and the 13-chapter guide — the complete toolkit is here.

You have been saving for this. Now make sure you know what New Mexico requires before you sign.