You Just Wired $15,000 to a Stranger. You Haven't Even Inspected the House Yet.

Your offer was accepted on a three-bedroom ranch in Cary for $425,000. Your agent congratulated you. Then she told you to wire a $12,000 Due Diligence Fee directly to the seller's personal account --- by 5:00 PM tomorrow. Non-refundable. You asked what happens if the inspection finds termite damage, foundation cracks, or a failing HVAC system. She said you lose the $12,000 either way. You asked what happens if your appraisal comes in $30,000 low. Same answer. You asked what happens if your VA loan falls through because of a deployment change. Same answer.

You turned to Google and discovered that North Carolina is the only state in the country where buyers pay a non-refundable fee directly to the seller just to earn the right to inspect a property. You found Reddit threads where buyers lost $5,000, $15,000, even $50,000 in Due Diligence Fees on houses they never purchased. You found military families at Fort Liberty who secured zero-down VA loans but still needed $10,000 in cash they did not have. You found buyers who paid the fee, discovered catastrophic structural damage, and had to choose between losing their deposit or buying a house that needed $40,000 in repairs.

The problem is not that North Carolina is expensive. The problem is that North Carolina uses a Due Diligence Fee system that puts tens of thousands of dollars of non-refundable cash at risk before you complete a single inspection, a closing attorney system where the lawyer you hire and pay does not actually represent your legal interests, county-specific NCHFA income limits that can disqualify you for $15,000 in down payment assistance if a spouse's side income pushes your household total above the threshold, a triple-tiered coastal insurance structure that can add $5,000 to $8,000 per year in Wilmington or the Outer Banks, and a caveat emptor disclosure framework that gives sellers almost no legal obligation to reveal defects --- and no single resource explains how these systems interact or what each one costs you when you get it wrong.

The North Carolina First-Time Home Buyer Guide is a Due Diligence Protection System --- a structured walkthrough of every NC-specific contract mechanic, fee, legal risk, assistance program, and regional market dynamic that determines whether your home purchase protects your capital or quietly puts it at catastrophic risk. It replaces months of cross-referencing the NCHFA website, NCREC bulletins, county assessor databases, closing attorney blogs, and frantic Reddit threads about Due Diligence Fees with a single reference that tells you exactly how much to risk, exactly when your money goes hard, and exactly what North Carolina transactions look like when they go wrong.

The complete guide, a quick-start checklist, and eight standalone reference tools --- covering the Due Diligence Fee and Earnest Money system, NCHFA down payment programs ($15,000 and $8,000), the closing attorney representation gap, coastal insurance layers, inspections, deed types, closing costs, regional market intelligence across five metros, and a day-by-day transaction timeline. Ten printable files total:

- guide.pdf — The full 12-chapter guide

- checklist.pdf — Quick-start home buying checklist

- ddf-strategy-card.pdf — DDF vs Earnest Money comparison, regional DDF ranges, and negotiation strategy

- nchfa-eligibility-worksheet.pdf — NCHFA program comparison ($15K/$8K/CPLP) with fillable eligibility checklist

- inspection-checklist.pdf — Due Diligence Period inspection priority list with costs and scheduling order

- closing-cost-worksheet.pdf — Fillable closing cost breakdown with property tax rates and tax deduction reference

- coastal-insurance-reference.pdf — Triple-tier insurance system breakdown with fillable budget worksheet

- closing-timeline.pdf — Day-by-day transaction timeline from offer to keys with fillable dates

- regional-market-reference.pdf — Five-market comparison: Triangle, Charlotte, Triad, Asheville, and Coastal/Military

- key-contacts-reference.pdf — NCHFA, VA, USDA, municipal DPA contacts with fillable "Your Team" section

What's Inside the Due Diligence Protection System

A comprehensive 12-chapter guide with a quick-start checklist --- covering every stage from financial preparation through post-closing, built specifically for the contract mechanics, legal risks, assistance programs, and regional market dynamics that make North Carolina fundamentally different from every other state:

The Due Diligence Fee System Decoded

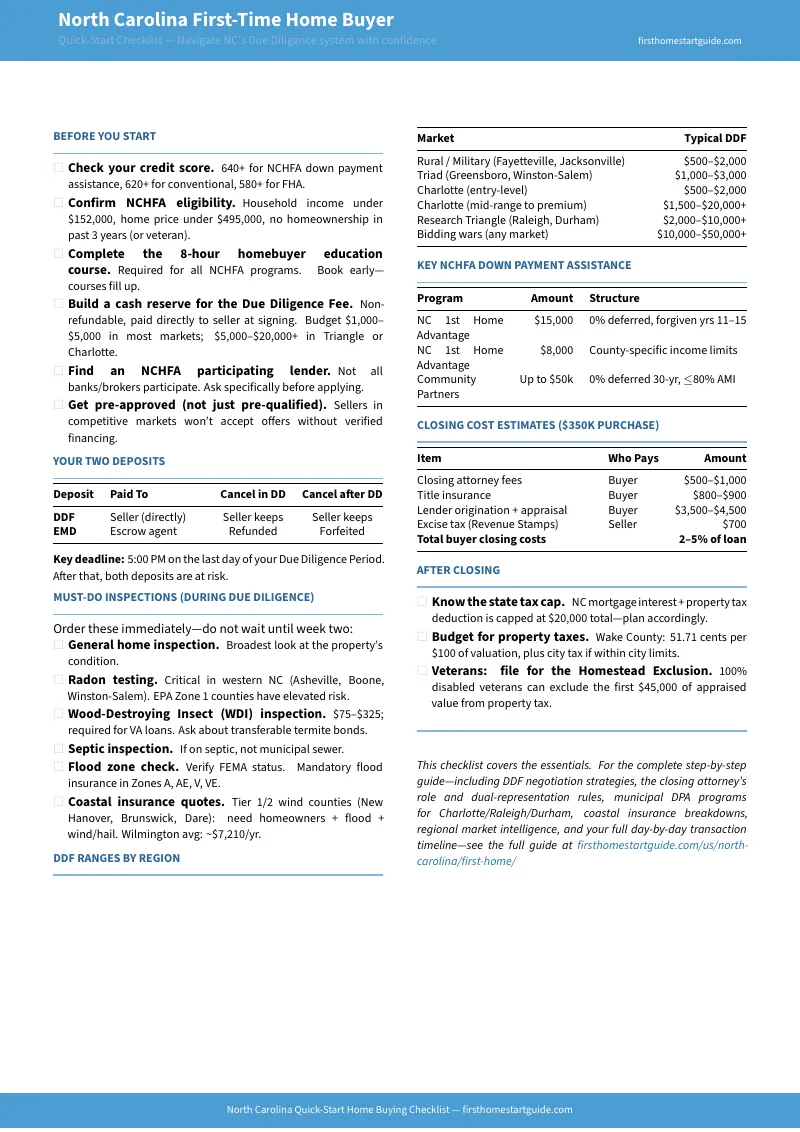

Generic home buying guides tell you about earnest money deposits. In North Carolina, earnest money is only half the story. The guide gives you the complete mechanics of the two-payment system under Form 2-T --- the non-refundable Due Diligence Fee paid directly to the seller versus the refundable Earnest Money Deposit held in escrow, when each payment goes hard, the 5:00 PM deadline that determines whether you lose one deposit or both, and the strategic framework for calibrating your DDF by region ($500 to $2,000 in military markets, $2,000 to $10,000+ in the Triangle, $10,000 to $50,000+ in bidding wars). You get the timeline diagram showing exactly when your capital becomes irretrievable --- and the negotiation strategy for offering a higher purchase price with a lower DDF to protect your liquid cash without weakening your offer.

The Closing Attorney Truth

You hire the closing attorney. You pay the closing attorney. But the closing attorney does not represent you. North Carolina mandates attorney-supervised closings, and by custom the buyer selects and compensates the attorney --- but that attorney's legal duty runs to the lender, not to you. The guide explains the fiduciary gap, what the closing attorney actually does (title search, lien verification, document preparation), what they cannot do (advocate for you in a dispute, sue the seller on your behalf, give strategic legal advice), and exactly when you need to hire your own independent real estate attorney before a contract dispute costs you everything.

NCHFA Down Payment Assistance Navigator

North Carolina offers two tiers of forgivable assistance through the Housing Finance Agency --- $15,000 (NC 1st Home Advantage) and $8,000 (Home Advantage) --- structured as zero-interest deferred second mortgages with unique forgiveness schedules. The guide maps both programs against their eligibility matrices: the 640 minimum credit score, the county-by-county household income limits based on everyone living in the home (not just the borrower), the 45% DTI cap, the first-time buyer definition (no ownership in 3 years or veteran), and the 15-year residency requirement for full forgiveness. You get the trap warnings --- how overtime pay, a spouse's side income, or a mid-transaction raise can silently push you above the county income limit and trigger denial days before closing.

Additional Assistance Programs

Beyond NCHFA, the guide covers Charlotte's House Charlotte program ($15,000 to $30,000 in down payment and closing cost assistance), Raleigh's DPA loans (up to $50,000 for households under 80% AMI), Durham's CDBG-funded assistance, and the Community Partners Loan Pool for public service workers. Plus VA loan strategy specific to North Carolina --- how the federal VA Escape Clause protects you from overpaying but does not protect your Due Diligence Fee, and the specific tactics military buyers at Fort Liberty, Camp Lejeune, and Seymour Johnson need to minimize upfront cash exposure on compressed PCS timelines.

Coastal Insurance: The Triple Threat

Standard homeowners insurance in Wilmington averages $7,210 per year --- 242% above the national average. But that policy still excludes flood and wind damage. In Tier 1 and Tier 2 coastal counties (New Hanover, Brunswick, Dare, Onslow), buyers need three separate policies: standard homeowners, standalone flood (NFIP or private), and standalone wind/hail (often through the NC Joint Underwriting Association). The guide breaks down the full triple-tier cost structure, the percentage-based wind/hail deductibles that can leave you with a $15,000 out-of-pocket after a hurricane, and how to budget for coastal insurance before you discover the gap between the national-average estimate in your mortgage calculator and the actual annual premium.

Inspections During Due Diligence

Every inspection must happen during your Due Diligence Period --- there are no separate inspection contingencies. The guide gives you the priority-ordered inspection schedule: general home inspection, radon testing (critical in EPA Zone 1 western counties around Asheville, Boone, and Winston-Salem), wood-destroying insect inspection, septic inspection, flood zone and elevation assessment for coastal and floodplain properties, and mountain-specific inspections for well water, grading, and slope stability. You get the timeline showing which inspections to order on Day 1 versus Day 5, and the cost benchmarks so your budget can absorb all required testing within the Due Diligence window.

The Caveat Emptor Framework

North Carolina is a buyer-beware state. The seller's disclosure obligation is limited to the Residential Property and Owners' Association Disclosure Statement (RPOADS) --- a form where sellers can legally mark "No Representation" on almost every question. The guide explains what the RPOADS actually requires sellers to disclose, what the Mineral and Oil and Gas Rights (MOGS) supplement covers, lead-based paint obligations for pre-1978 homes, and why the combination of caveat emptor and the Due Diligence system makes thorough inspections not optional but existentially necessary.

NC Deed Types and Title Protection

Not all deeds provide the same protection. The guide covers General Warranty Deeds (maximum protection --- seller warrants against all title defects), Special Warranty Deeds (limited protection --- seller only warrants during their ownership period), and Quitclaim Deeds (zero warranty --- common in family transfers and foreclosures). You learn which deed type to insist on, when a Special Warranty Deed is acceptable, and why title insurance is essential regardless of deed type in a state where mineral rights, timber rights, and historical easements can survive across generations.

Closing Costs and Tax Structure

North Carolina's Excise Tax (Revenue Stamps) runs $1.00 per $500 of purchase price --- $850 on a $425,000 home. The guide provides the full closing cost breakdown: attorney fees ($500 to $1,500), title insurance, recording fees, property tax proration, HOA transfer fees, and prepaid escrow. You get the property tax rate comparison across metros (Charlotte 1.04%, Raleigh 0.96%, Asheville 0.65%), the Disabled Veteran Property Tax Exclusion for 100% VA-rated veterans, and the state income tax implications including the $20,000 mortgage interest deduction cap unique to NC's flat 4.5% rate.

Five-Market Regional Intelligence

What $400,000 buys varies dramatically across North Carolina. The guide covers the Research Triangle ($420,000 median, tech economy, highest DDF competition), Charlotte Metro ($380,000 median, financial sector, aggressive bidding with waived inspection requests), the Triad ($285,000 median, manufacturing transition, lower DDF requirements), Asheville and Western NC ($450,000+ median, tourism economy, radon and slope risks), and Coastal/Military markets (Wilmington $340,000, Fayetteville $250,000, Jacksonville $270,000 --- flood zones, wind insurance, compressed VA timelines). Each region includes typical DDF ranges, dominant buyer profiles, and the specific risks that trip up first-time buyers in that market.

Day-by-Day Transaction Timeline

The full 30-to-45-day closing process mapped from pre-approval through your first month of ownership: the Due Diligence Period schedule (which inspections to order on Day 1, when to expect the appraisal, when financing must be confirmed), the 5:00 PM termination deadline mechanics, financing finalization, the closing attorney's document preparation timeline, and your walk-through and closing day protocol. Every critical date mapped with what happens if you miss it.

Who This Guide Is For

- First-time buyers in the Triangle or Charlotte who just learned they need to wire $5,000 to $15,000 in non-refundable cash to a seller before seeing an inspection report --- and want a framework for calibrating the right amount to offer without over-risking their liquid reserves

- Military families PCSing to Fort Liberty, Camp Lejeune, or Seymour Johnson who secured VA loan pre-approval but are being told they need thousands in cash for a Due Diligence Fee that their zero-down loan does not cover --- and need strategies to compete without draining their emergency fund

- Out-of-state relocators moving to Raleigh, Durham, or Charlotte from states where inspection contingencies and earnest money escrow are standard --- who need to understand why national real estate advice is dangerously wrong for North Carolina

- Buyers targeting NCHFA's $15,000 down payment assistance who need to navigate household income limits, county-specific thresholds, the 15-year forgiveness timeline, and the eligibility traps that disqualify applicants weeks before closing

- Coastal buyers considering Wilmington, the Outer Banks, or Onslow County who need to budget for triple-tiered insurance (homeowners + flood + wind/hail) that can add $5,000 to $8,000 per year beyond what any national mortgage calculator estimates

- Anyone buying in western NC (Asheville, Boone, mountain communities) who faces elevated radon risk, slope stability concerns, well water testing requirements, and premium pricing driven by limited buildable land

Why Not Free Tools and Forums?

Free information on buying a home in North Carolina exists. Here is what it actually delivers:

- The NCHFA website gives you program descriptions, income limits, and a list of participating lenders. It does not explain how household income is calculated, warn you that a spouse's side income counts even if they are not on the mortgage, show you the forgiveness timeline trap if you sell before year eleven, or help you decide between the $15,000 and $8,000 programs based on your specific financial situation. You get eligibility criteria without the decision framework.

- Reddit threads (r/raleigh, r/Charlotte, r/NorthCarolina) contain genuine warnings about Due Diligence Fees from buyers who lost thousands. But they are mixed with outdated fee ranges from 2020, incorrect claims about getting DDF refunds, confusion between the DDF and earnest money, and advice from other states that does not apply here. Sorting current from dangerous takes longer than reading a guide that already did it.

- Real estate agent blogs explain what the Due Diligence Fee is. They do not tell you how to negotiate a lower one, when a higher DDF is strategically correct, how to use purchase price versus DDF tradeoffs to win a bidding war, or what to do if your inspection reveals catastrophic damage after you have already paid $15,000. Agents are incentivized to close transactions, not to help you walk away from bad ones.

- National home buying guides describe earnest money, contingencies, and inspection periods that do not exist in North Carolina. Following their advice here --- assuming you can back out after a failed inspection and get your deposit back --- will cost you thousands of dollars. North Carolina's contract system is structurally incompatible with generic national advice.

This guide fills the North Carolina-specific gap --- the space between knowing how to buy a home in general and knowing how to buy one in a state where a non-refundable Due Diligence Fee gambles your cash before any inspection, the closing attorney you pay represents the lender instead of you, NCHFA income limits disqualify families for a single undisclosed income source, coastal insurance triples the national average, sellers can legally mark "No Representation" on every disclosure question, and the 5:00 PM termination deadline is enforced to the minute. It is the risk analysis that would take a North Carolina real estate attorney, a NCHFA program specialist, and an insurance agent to assemble --- structured as a reference you own permanently.

--- Less Than Your Closing Attorney's Filing Fee

A single consultation with a North Carolina real estate attorney runs $150 to $300 per hour. Missing the Due Diligence Period deadline by one day can cost you your entire Earnest Money Deposit on top of a $10,000+ DDF you already lost. Failing to understand NCHFA's household income calculation can mean losing $15,000 in free down payment assistance at the worst possible moment. Buying coastal without budgeting for triple-tiered insurance can add $400 to $700 per month to your carrying costs that your mortgage calculator never showed you.

This guide does not replace your real estate agent, your lender, or your closing attorney. But it gives you the Due Diligence Fee calibration framework, the NCHFA eligibility navigator, the coastal insurance calculator, the inspection priority timeline, and the day-by-day transaction map that ensure you identify every North Carolina-specific risk before your money goes hard --- instead of discovering them when you are already under contract and the 5:00 PM deadline is counting down.

If it prevents a single over-sized Due Diligence Fee, catches a single NCHFA eligibility trap, or alerts you to coastal insurance costs before you commit to a Wilmington purchase --- it pays for itself before you finish reading it.

30-day money-back guarantee. If the guide does not sharpen your North Carolina home buying analysis and protect your capital, you pay nothing.

Download the free North Carolina Quick-Start Home Buying Checklist to see the step-by-step framework covering pre-approval, Due Diligence Period management, inspections, and closing. When you are ready for the full DDF negotiation strategy, NCHFA program navigator, regional market intelligence, and the complete 12-chapter guide, the full toolkit is here.

North Carolina's Due Diligence system rewards buyers who understand it and punishes those who don't. This guide makes sure you're on the right side.