You Got Pre-Approved. But Nobody Told You That Your New Address Triggers a 4.25% Municipal Income Tax, Your School District Levies an Additional 1.75% on Top of That, and the City Won't Let You Close Until You Escrow 150% of the Cost of Fixing a Cracked Driveway.

You found a three-bedroom in Lakewood with a finished basement. Or a renovated colonial in Cleveland Heights that's finally in your price range. Or a new-build in Delaware County where your Columbus commute is 35 minutes and you can use Dublin schools. You ran the numbers through Zillow's mortgage calculator, your lender pre-approved you for $310,000, and you're ready to write your first offer.

Then Ohio happens. Your mortgage calculator estimated your monthly payment based on principal, interest, property taxes, and insurance. It didn't account for the 2.5% workplace income tax Cleveland deducts from every paycheck, the 2.25% residence tax Shaker Heights levies on top of that with only a 0.5% credit, or the 1.75% School District Income Tax you now owe because your new address sits inside one of 210 districts that levy a separate tax on residents. Your lender never mentioned RITA or the CCA. Your employer only withholds the workplace tax. Nobody told you to file an Ohio IT 4 with your four-digit school district code. Your take-home pay drops by $4,500 a year and the first notice from RITA arrives with a penalty and interest.

Here's what no single free resource explains: Ohio layers a municipal income tax system administered by RITA and the CCA — where your workplace city and your residence city each claim a percentage of your gross pay and the credit between them may cover half, all, or none of the overlap — against a School District Income Tax levied by 210 individual districts using two different tax bases that your employer's payroll system doesn't automatically withhold, against a county conveyance fee structure where closing on a $300,000 home costs $1,200 in Cuyahoga County and $600 in Montgomery County, against mandatory municipal Point-of-Sale inspections in Northeast Ohio where the city requires you to escrow 125% to 150% of the repair estimate in cash on top of your down payment and closing costs, against an OHFA YourChoice! down payment assistance program where choosing 5% over 2.5% saves you cash at closing but permanently raises your mortgage rate enough to cost $25,000 in additional interest over 30 years, against a closing process that gives you the keys at the table in Columbus but makes you wait 48 hours in Cleveland because the two regions use entirely different systems. Each of these has cost real Ohio first-time buyers thousands of dollars because the information existed — scattered across RITA municipal tax tables, county auditor portals, OHFA program matrices, Reddit threads from buyers who received their first delinquency notice, and city building department violation lists — but nobody assembled it into a single decision system calibrated to how Ohio actually works.

The Ohio First-Time Home Buyer Guide is an Ohio Tax Navigation System — not a motivational overview of the Buckeye State housing market, but a structured reference that maps every Ohio-specific municipal tax, school district tax, down payment program, closing custom, inspection requirement, and county fee variation into a process you work through before your earnest money is at risk. It replaces months of cross-referencing RITA tax tables, OHFA program sheets, county auditor conveyance fee schedules, and municipal building department escrow requirements with a single guide that tells you exactly what to verify, exactly what the numbers should look like, and exactly where deals go wrong in this state.

What's Inside the Ohio Tax Navigation System

A comprehensive guide, a quick-start checklist, and 8 standalone printable tools (10 PDFs) — covering every stage from pre-approval through post-closing, built specifically for the tax structures, assistance programs, closing customs, and municipal regulations that make Ohio different from every other state:

RITA/CCA Municipal Income Tax Decision Matrix

Ohio's municipal income tax system is nationally unusual and financially devastating when misunderstood. Every city and village sets its own tax rate — administered through either RITA or the CCA — and you owe tax to both your workplace municipality and your residence municipality simultaneously. The guide breaks down exactly how the workplace/residence credit system works, why the credit rarely covers the full overlap, and how to calculate your actual combined municipal tax liability before you commit to an address. It includes the specific example that catches most buyers: working in Cleveland (2.5% workplace tax) and buying in Shaker Heights (2.25% residence tax with only a 0.5% credit) means surrendering 4.25% of your gross income to two city governments. It covers the mandatory Ohio IT 4 filing for employer withholding, the quarterly estimated payment schedule for residence taxes your employer doesn't deduct, the seven-year audit window for unfiled municipal returns, and the Columbus city-tax-suburban-schools anomaly where specific addresses pay Columbus tax rates while zoning for Dublin or Hilliard school districts — a premium that educated buyers actively seek and uneducated buyers accidentally stumble into.

School District Income Tax (SDIT) Trap Identifier

On top of municipal income tax, 210 Ohio school districts levy their own separate income tax on residents — ranging from 0.5% to 2.0% of household income. This tax is entirely based on your physical address, completely divorced from where you work, and your employer almost certainly isn't withholding it. The guide explains the two different tax bases (Traditional vs. Earned Income) that determine whether your investment income, retirement distributions, and capital gains are also taxed, shows you how to use the Ohio Department of Taxation's "Finder" tool to verify any address's SDIT status before you submit an offer, and walks through the IT 4 filing process to set up withholding with the correct four-digit school district code. Moving across a single street can trigger an unbudgeted 1.5% tax on your entire household income — and the state will retroactively bill you with penalties if you fail to file.

OHFA YourChoice! Down Payment Assistance Calculator

Ohio's primary down payment assistance program lets eligible first-time buyers choose either 2.5% or 5% of the purchase price toward their down payment and closing costs. But both options are forgivable second mortgages with a seven-year residency cliff — sell, refinance, or convert to rental before year seven and you repay the entire amount. The guide runs the amortization math that loan officers skip: choosing the 5% tier provides more upfront cash but locks you into a permanently higher primary mortgage interest rate. On a $250,000 home, that rate premium costs over $25,000 in additional interest over the life of the loan. It covers the credit score thresholds (640 for Conventional/VA/USDA, 650 for FHA), the county-specific income and purchase price caps, the Grants for Grads 20%-per-year prorated forgiveness (within 48 months of graduation), and the Mortgage Tax Credit that returns up to $2,000 per year as a direct federal tax credit — including how to layer MTC with DPA without tripping the qualification matrices.

Cleveland Point-of-Sale (POS) Inspection Survival Guide

In Northeast Ohio, you cannot close on a home until the municipality inspects it and issues a Certificate of Inspection. Cities deploy inspectors who cite everything from cracked driveway aprons and peeling garage paint to unpermitted rear decks and loose handrails. In a seller's market, sellers refuse to make repairs — and the buyer must fund an assumption escrow at 125% to 150% of the estimated repair cost, in cash, on top of the down payment and closing costs. The guide includes the escrow multiplier and base inspection fee for every major Cleveland suburb, explains why FHA and VA underwriters routinely refuse to fund loans on properties with unresolved POS violations (forcing buyers into higher-interest 203(k) renovation loans or deal collapse), covers the dye test requirements for sewer lines, and provides the negotiation framework for shifting POS repair costs back to the seller or structuring a credit that preserves your liquidity.

County Conveyance Fee Calculator

Ohio's real property conveyance fee varies dramatically by county. The state mandates $1 per $1,000 of sale price, but 87 of 88 counties add a permissive fee of $1 to $3 per $1,000 on top. Buying a $300,000 home in Cuyahoga County costs $1,200 in conveyance fees. The same home in Montgomery County costs $600. In Franklin County, if the seller receives a homestead exemption, the permissive fee is waived entirely. The guide includes a county-by-county reference covering the Columbus, Cleveland, Cincinnati, and Dayton metros with the exact fee rates, exemptions, and the specific line items that appear on your Closing Disclosure — so your closing cost estimate reflects reality, not a national calculator's approximation.

Roundtable vs. Escrow Closing Customs

Ohio is culturally and procedurally split in how real estate closings work. In Central Ohio and most rural counties, you close at a roundtable — everyone gathers in a conference room, signs documents simultaneously, and you walk out with the keys. In Northeast Ohio, the escrow model prevails — buyer and seller never meet, documents are executed separately over days, and the title must be recorded with the county auditor before keys are released, creating a 24-to-48-hour wait. The guide explains both systems so you know exactly what to expect, covers the attorney vs. title company decision (Northeast Ohio's century-old housing stock and POS assumption escrows make attorney representation highly advisable), and calculates the additional legal costs that Cleveland-area buyers face compared to Columbus or Dayton transactions.

Cincinnati vs. Northern Kentucky Cross-Border Analysis

Cincinnati-area buyers routinely evaluate properties on both sides of the Ohio River, drawn to Northern Kentucky by perceived lower property taxes and the absence of municipal income tax. The guide exposes the vehicle trap: Kentucky levies a 6% usage tax when you first register an out-of-state vehicle, followed by an annual ad valorem property tax of approximately 1% of the vehicle's NADA value. For a household with two newer vehicles, that's thousands of dollars annually — often negating the property tax savings entirely. The cross-border analysis covers Ohio's Cincinnati 1.8% city income tax against Kentucky's vehicle tax burden, county-level property tax comparisons, and the commuter tax credit implications for workers who live in one state and work in the other.

Dayton/Wright-Patterson Military Buyer Profile

Montgomery and Greene counties attract active-duty personnel, civilian defense contractors, and veterans using VA home loans. The guide covers the VA loan parameters for the Dayton market, the OHFA Homeownership for Heroes rate discount, Montgomery County's lower $2 per $1,000 conveyance fee (versus $4 in Cuyahoga), and USDA Rural Development eligibility for buyers pushed into exurban Licking, Knox, and Fairfield counties by Columbus's appreciation — including the income limits ($119,850 for 1-4 person households, $158,250 for larger families) and the 100% financing structure.

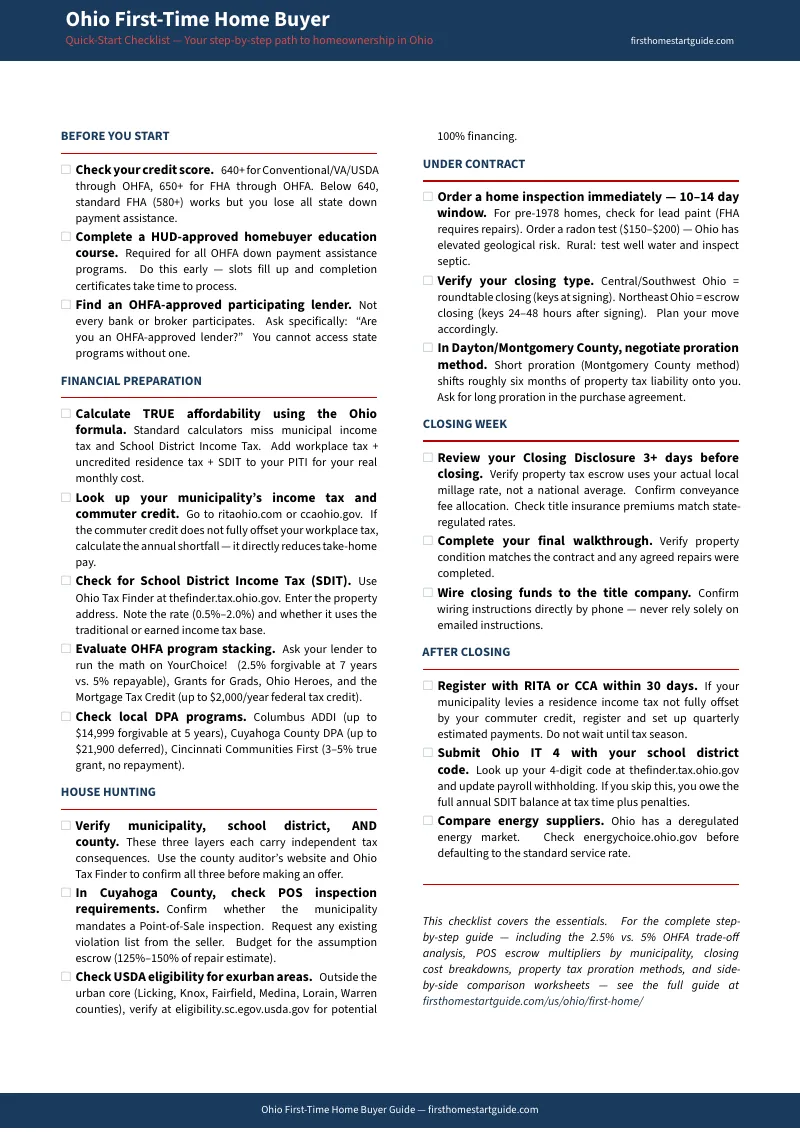

29-Item Quick-Start Checklist

A structured checklist covering five phases — pre-qualification, house hunting, making an offer, closing, and after closing — with Ohio-specific deadlines, RITA/SDIT verification steps, OHFA program requirements, POS inspection preparation, and county-level closing cost checks at each stage. Print it and check items off as you go.

8 Standalone Printable Tools

Print-ready reference cards and worksheets you can bring to lender meetings, property showings, inspections, and closing appointments:

- Closing Cost Calculator Worksheet — Line-by-line fillable worksheet covering county conveyance fees, title insurance, lender fees, prepaid items, OHFA DPA credits, POS assumption escrow, and seller concessions

- Inspection Checklist — Standard inspection items plus Ohio-specific checks for POS compliance, sewer dye tests, radon, termites, and lead paint (pre-1978 housing stock prevalent in Cleveland and Cincinnati)

- OHFA Program Comparison Card — Side-by-side reference for 2.5% vs. 5% YourChoice! DPA, Grants for Grads, Mortgage Tax Credit, Heroes discount, and qualification requirements

- Municipal Tax Calculator Card — RITA/CCA workplace-residence credit worksheet with the Shaker Heights 4.25% worked example, quarterly estimated payment schedule, and IT 4 filing instructions

- School District Income Tax Lookup Card — How to use the Ohio Finder tool, Traditional vs. Earned Income tax base explained, IT 4 school district code instructions, and the penalty structure for non-filing

- County Conveyance Fee Reference Card — County-by-county fee table for the 15 most common first-time buyer counties, homestead exemption waiver rules, and fee calculation formula

- POS Inspection Preparation Card — Municipality-by-municipality escrow multiplier table, base inspection fees, common violation categories, assumption escrow negotiation tactics, and FHA/VA underwriting disqualifiers

- Regional Closing Customs Quick Reference — Roundtable vs. escrow process side by side, attorney vs. title company comparison, and Northeast Ohio attorney fee ranges

Who This Guide Is For

This guide is for first-time home buyers in Ohio who:

- Are buying their first home anywhere in Ohio and need to understand how RITA, the CCA, and School District Income Taxes will reduce their take-home pay — before the pre-approval letter becomes a purchase agreement and the municipal tax bills start arriving

- Are considering OHFA YourChoice! down payment assistance and need to decide between 2.5% and 5% — with the actual amortization math showing the long-term interest cost of the higher tier, the seven-year forgiveness cliff, and the Grants for Grads and Mortgage Tax Credit layering options

- Are buying in Cuyahoga County or Northeast Ohio and need to understand Point-of-Sale inspections — the assumption escrow multipliers, the dye test requirements, the FHA/VA underwriting refusals, and the negotiation strategies that preserve their liquidity

- Are relocating from another state and need to decode Ohio's closing customs — why Columbus gives you the keys at the table but Cleveland makes you wait 48 hours, why Northeast Ohio buyers typically hire attorneys while Central Ohio buyers use title companies, and why the conveyance fee on a $300,000 home ranges from $600 to $1,200 depending on the county

- Are evaluating Cincinnati versus Northern Kentucky and need the real cross-border tax comparison — including the vehicle ad valorem trap that negates perceived property tax savings for households with newer cars

- Want every Ohio-specific tax, program, inspection requirement, and regional closing custom in one reference — instead of piecing it together from RITA tax tables, OHFA program PDFs, county auditor websites, municipal building department notices, and Reddit threads from buyers who learned the hard way

Why Not Free Tools and Forums?

Free information on buying a home in Ohio exists. Here's what it actually delivers:

- OHFA's website publishes program guidelines, income limits, and lender directories. It doesn't compare the 2.5% vs. 5% DPA tiers with the long-term interest cost calculation, doesn't explain the seven-year cliff forgiveness with no prorated scale, and doesn't walk through how to layer Grants for Grads with the Mortgage Tax Credit. You get the program specs without the decision framework.

- Zillow and Realtor.com show estimated monthly payments based on principal, interest, property taxes, and insurance. They don't factor in the municipal income tax your workplace city deducts, the residence tax your home city levies on top, or the School District Income Tax that 210 districts charge separately. You get a monthly number that can be $300 to $500 lower than reality.

- Real estate agent blogs mention OHFA assistance and Ohio's affordability. They don't explain how RITA's residence tax credit works, don't disclose the POS assumption escrow multipliers that drain $10,000 to $15,000 in liquid cash at closing, and don't cover the county-by-county conveyance fee differences that can save or cost you hundreds of dollars by crossing an invisible border. The content is designed to generate leads, not to warn you about the tax bill that arrives three months after closing.

- Reddit threads (r/Columbus, r/Cleveland, r/cincinnati) contain genuine buyer experiences — people sharing RITA delinquency notices, POS inspection rage, and Kentucky vehicle tax shock. But advice from 2023 doesn't reflect current OHFA income limits, updated SDIT rates, or the latest municipal tax credit structures. Sorting current from outdated information across four metro-specific subreddits takes longer than reading a guide that has already done it.

This guide fills the Ohio-specific gap — the space between knowing how to buy a house in general and knowing how to buy one in a state where your residence city and your workplace city each tax your income separately, where 210 school districts levy their own tax that your employer doesn't withhold, where the municipality can block your closing until you escrow 150% of a driveway repair, where OHFA's "free" down payment assistance costs $25,000 in additional interest if you pick the wrong tier, and where the closing process itself changes depending on whether you're in Columbus or Cleveland. It's the analysis that would take an Ohio real estate attorney, a RITA/CCA tax specialist, and an OHFA-approved lender to assemble — structured as a reference you own permanently.

— Less Than One RITA Penalty Notice

A single RITA delinquency notice with penalties and interest on unfiled municipal taxes runs hundreds of dollars — and can be assessed retroactively for seven years. Choosing the wrong OHFA DPA tier costs over $25,000 in additional mortgage interest. A Point-of-Sale assumption escrow in Cleveland Heights can drain $12,500 in liquid cash on top of your down payment. Buying in Cuyahoga County instead of Montgomery County costs an extra $600 in conveyance fees on a $300,000 home. A School District Income Tax you didn't know existed costs 0.5% to 2.0% of your household income every year until you sell.

This guide doesn't replace your real estate agent or your lender. But it gives you the RITA/CCA municipal tax calculator, the SDIT boundary verification process, the OHFA DPA amortization comparison, the POS inspection escrow multiplier tables, the county conveyance fee reference, and the regional closing custom breakdown that ensure you identify every Ohio-specific financial risk before your earnest money is committed — instead of discovering them on your first RITA tax bill, your first school district penalty notice, or your first assumption escrow cash call at the closing table.

If it catches a single municipal tax credit gap, prevents a single SDIT filing penalty, or saves you from choosing the wrong OHFA tier, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't sharpen your decision-making and protect your investment in Ohio's unique tax and regulatory landscape, you pay nothing.

Download the free Ohio Quick-Start Home Buying Checklist to see the 29-item action plan covering pre-qualification, tax verification, offer strategy, closing preparation, and post-closing protection. When you're ready for the full RITA/CCA tax calculator, OHFA decision framework, POS inspection survival guide, and county-by-county closing cost analysis, the complete guide is here.

The house looks perfect on Zillow. This guide tells you whether Ohio's tax code agrees.