The Spreadsheet Says Cash Flow. The Tornado Premium Says Otherwise.

You found a triplex in Midwest City throwing off 9% gross yield against an E-5's $1,605 BAH ceiling. Or a single-family in Moore where the rent-to-price ratio clears the 1% rule with room to spare. Or a tax sale property in Oklahoma County where you can acquire a fee simple deed for pennies on the dollar at the June auction. The numbers work. The cap rate is solid. You're ready to wire earnest money.

Then you run the real numbers. The Midwest City triplex comes back with an annual landlord insurance quote of $4,200 — not the $1,200 you modeled from national averages. Your wind and hail deductible is set at 2% of dwelling value, which means $8,000 out of pocket before the primary policy pays a cent on the next hailstorm. The Moore single-family sits on expansive clay soil that has already produced stair-step cracking in the exterior brick veneer, and the foundation repair company that showed up uninvited is quoting $18,000 for steel pier underpinning — but you haven't hired an independent structural engineer to determine whether the $18,000 job is actually necessary or whether you're looking at $800 in cosmetic patching. The tax sale property has zero post-sale redemption period, which sounds like instant equity — until you learn that title insurance underwriters universally refuse to insure tax deeds, that you need a Quiet Title lawsuit costing $2,750 or more and taking 90 to 120 days, and that an unknown heir or IRS lien can contest the action and drag you into full litigation. Meanwhile, you just discovered that the mineral rights on your Norman rental were severed in 1947, and an operator with a valid lease can legally enter the property to drill under the dominant mineral estate doctrine — and the Surface Damages Act does not give you veto power.

Here's what no single resource explains: Oklahoma layers insurance premiums that run 2-3x the national average with percentage-based wind and hail deductibles that create $5,000-$10,000 out-of-pocket exposure per claim, a geological reality where expansive clay soil moves every foundation in the state and independent structural engineer evaluations cost $310-$780 while commissioned repair salesmen quote $10,000-$30,000 for work that may not be necessary, a mineral rights regime where the mineral estate is legally dominant and operators can commence drilling on your residential lot after posting a $25,000 bond even while compensation is being litigated, security deposit escrow requirements where commingling funds is a criminal offense punishable by up to six months in county jail and a fine of twice the misappropriated amount, a property tax assessment that resets to your purchase price upon transfer regardless of the seller's historically capped bill, and a five-year capital gains exemption that eliminates the state's 4.5% tax entirely on patient holds — into an operating environment that rewards investors who model Oklahoma-specific risks and punishes everyone who applies national assumptions. Every one of these has cost real investors five to six figures because the information existed — scattered across Title 41 landlord-tenant statutes, Title 52 oil and gas code sections, Oklahoma Tax Commission rate tables, DoD BAH lookup tools, and BiggerPockets threads from 2023 — but nobody had assembled it into a single underwriting system.

The Oklahoma Investment Property Guide is a Sooner State Underwriting System — not a motivational overview of rental property investing, but a structured due diligence framework that maps every Oklahoma-specific financial trap, environmental risk, and regulatory requirement into a process you work through before you wire earnest money. It replaces months of cross-referencing insurance broker quotes, county assessor websites, Title 41 code sections, foundation repair estimates, mineral rights abstracts, and DoD BAH tables with a single reference that tells you exactly what to verify, exactly what the numbers should look like, and exactly where deals go wrong.

What's Inside the Sooner State Underwriting System

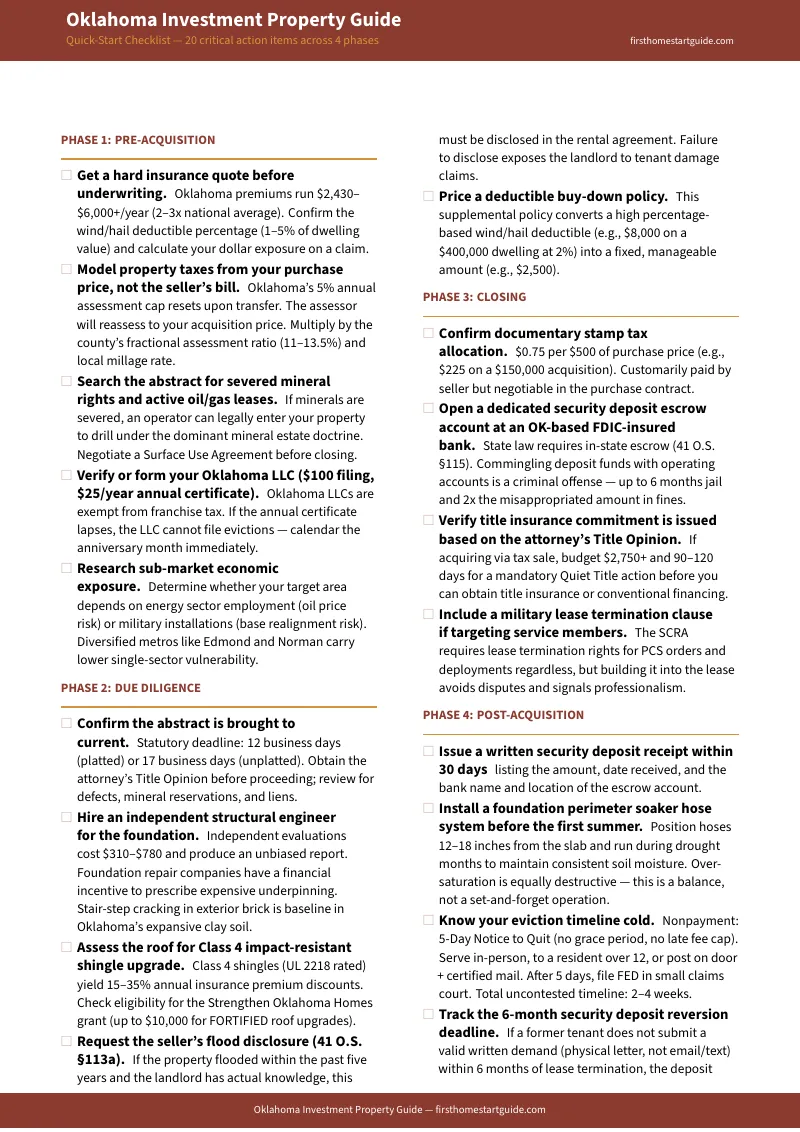

A 20-chapter guide, a quick-start checklist, and 4 standalone printable worksheets and reference cards — covering every stage from entity formation through exit strategies, built specifically for the financial traps and environmental realities that make Oklahoma different from every other state:

The Tornado Premium: Insurance Underwriting

Oklahoma sits in the corridor of maximum convective storm activity, and the financial consequences for investors who model insurance at national averages are immediate and severe. The guide covers the actual premium range for Oklahoma investment properties — $2,430 to over $6,000 annually — and explains the percentage-based wind and hail deductible structure that creates $5,000 to $10,000 out-of-pocket exposure on a single claim. It walks through deductible buy-down policies that convert a variable catastrophic risk into a fixed operating expense: a $10,000 deductible bought down to $2,500, with the supplemental policy covering the $7,500 gap. It covers Class 4 impact-resistant shingles rated under UL 2218, which yield annual premium discounts of 15% to 35%, and the FORTIFIED Home certification program that can push total premium reductions to 42%. It maps the Strengthen Oklahoma Homes grant program offering up to $10,000 for FORTIFIED roof upgrades — free money that simultaneously reduces your operating expenses and increases exit value. Every property acquisition should start with a hard insurance quote, not end with one.

Red Dirt Realities: Foundation Assessment and Maintenance

Oklahoma's iron-rich expansive clay soil moves every foundation in the state. Stair-step cracking in exterior brick veneer, separated baseboards, and doors that refuse to latch are baseline conditions, not deal-killers — but an out-of-state investor who has never seen these symptoms will panic and either walk away from a solid deal or accept an $18,000 repair quote from a commissioned salesman without getting an independent assessment. The guide covers the geological shrink-swell cycle that causes differential settlement, the critical distinction between cosmetic settling and active structural failure, and the cost spectrum from drainage corrections at $2,000-$5,000 through polyurethane foam injection at $3,000-$10,000 to full steel pier underpinning at $10,000-$30,000. It explains why an independent structural engineer evaluation at $310-$780 is mandatory — and why a previously repaired foundation backed by a transferable lifetime warranty and a clean engineering report is often a better investment than an unrepaired foundation of unknown condition. It covers the soaker hose protocol: automated hoses positioned 12-18 inches from the foundation perimeter during summer drought months to maintain consistent soil moisture, preventing the catastrophic shrinkage phase that causes the worst differential settlement.

Mineral Rights and Surface Rights Due Diligence

Oklahoma's century of petroleum extraction means the surface estate and mineral estate on your investment property are frequently severed — and under established common law, the mineral estate is the dominant estate. The guide covers the Surface Damages Act (Title 52, Sections 318.2-318.9): an operator must negotiate in good faith and provide compensation for surface damages, but fundamentally cannot be blocked from drilling if they hold a valid mineral lease. If negotiations fail, the operator posts a $25,000 corporate surety bond with the Secretary of State, petitions the court to appoint appraisers, and commences drilling operations immediately — even while final compensation is being litigated. Willful failure to negotiate can result in treble damages. The guide walks through the abstract review protocol for identifying active mineral leases, negotiating surface use agreements, and underwriting the potential disruption of surface access when acquiring land in active geological basins.

Landlord-Tenant Law: The Five-Day Notice Advantage

Oklahoma is one of the fastest landlord-friendly jurisdictions in the country, but the speed only works with flawless procedural compliance. Under Title 41 of the Oklahoma Statutes, rent is due on the exact date specified in the lease — no statutory grace period, no late fee cap. The landlord serves a 5-Day Notice to Quit: personally delivered, left with a resident family member over age 12, or posted conspicuously on the property and simultaneously sent via certified mail. After five days without payment or vacancy, the landlord files a Forcible Entry and Detainer action in small claims court. The sheriff serves summons at least 3 days before the hearing. If the tenant fails to appear, automatic default judgment. The Writ of Assistance gives the tenant 48 hours to vacate before the sheriff physically removes occupants. Total uncontested timeline: 2-4 weeks from notice to lockout. The guide covers non-rent violations (15-day notice with 10 days to cure), month-to-month terminations (30 days), criminal activity terminations (24 hours to 5 days), and the procedural mistakes in service of process that routinely result in dismissal and force the landlord to restart the entire timeline.

Security Deposit Compliance: The 45-Day Countdown and the Six-Month Reversion

Oklahoma's security deposit laws contain strict compliance traps that investors frequently trigger out of ignorance. All deposits must be held in a dedicated escrow account at a federally insured financial institution located within the State of Oklahoma (41 O.S. Section 115). Commingling deposit funds with operating capital is not just a civil violation — it is a criminal offense punishable by up to six months in county jail and a fine of twice the misappropriated amount. Landlords must provide a written receipt within 30 days specifying the amount, date received, and the bank name and location. Upon lease termination, the tenant must initiate return with a valid written demand — emails and text messages do not satisfy this requirement. Once received, the landlord has exactly 45 days to return the full deposit or provide an itemized statement of deductions. But here's the provision that most out-of-state landlords miss entirely: if the tenant fails to make a valid written demand within six months after lease termination, the deposit legally reverts to the landlord in full under 41 O.S. Section 115. The tenant's claim is permanently extinguished.

Property Tax Assessment and the Reset Trap

Oklahoma's property taxes rank among the lowest in the nation, with average effective rates around 0.79% to 0.94% depending on county. Under Article X, Section 8B of the Oklahoma Constitution, the taxable value of a non-homestead investment property cannot increase by more than 5% in any given year — providing unparalleled holding cost predictability. But the cap resets upon transfer. When you purchase a property, the county assessor resets the fair cash value to your actual acquisition price. Investors who model future property taxes based on the seller's historically capped bill face a severe cash flow shortfall when the new, uncapped assessment hits. The guide provides county-level effective rates (Oklahoma County at 0.94%, Tulsa County at 0.90%, Rogers County at 0.71%, Pottawatomie County at 0.64%), the three-step ad valorem calculation using fractional assessment ratios of 11% to 13.5%, and the pending State Question 847 that would reduce the non-homestead cap from 5% to 4%.

Military Housing Markets: Tinker AFB and Fort Sill

Oklahoma's two premier military installations provide landlords with disciplined tenants whose housing expenses are directly subsidized by the Department of Defense. The guide provides 2026 BAH rates for every relevant pay grade at both installations: Tinker AFB in the OKC metro (E-4 at $1,536, E-5 at $1,605, E-6 at $1,668, O-3 at $1,830 — all with dependents) and Fort Sill in Lawton (E-4 at $1,170, E-5 at $1,248, E-6 at $1,455, O-3 at $2,106). It maps the sub-markets surrounding each base — Edmond at $1,035 average rent for officers seeking premium school districts, Moore at $950 for family housing, Midwest City at $803 for maximum proximity to Tinker's gate, Del City at $790-$814 for the highest cash-on-cash yield. It covers the Balfour Beatty on-base housing competition, the SCRA military lease termination clause requirement, and the fundamental strategic difference: Tinker is a diversified metro play with appreciation upside, while Lawton is a pure cash-flow market with minimal appreciation potential and high vulnerability to base realignment decisions.

Tax Sale Investing and the Quiet Title Reality

Oklahoma's county tax resale auctions occur on the second Monday of June with zero post-sale redemption period — the prior owner's right to reclaim the property is permanently extinguished at the gavel (Title 68, Section 3113). But the county issues a Treasurer's Tax Deed, not a warranty deed, and title insurance underwriters universally refuse to insure it. To achieve marketable title, you must file a Quiet Title action in District Court — naming all prior owners, lienholders, and interested parties as defendants — at an approximate cost of $2,750 or more, with an uncontested timeline of 90 to 120 days. If contested by a former heir or institutional lienholder like the IRS, the action becomes standard litigation with escalating costs and timelines. Under Title 12, Section 1141, if an adverse claim is found to be sham legal process, the court can award treble damages to the prevailing plaintiff. The guide mandates building quiet title legal fees and a 4-6 month holding period into your maximum bid calculation — a tax sale acquisition is not liquid until the quiet title judgment is entered.

Entity Formation, Financing, and Exit Strategies

Oklahoma LLC formation at $100 ($25 expedited), with no franchise tax and a $25 annual certificate filing that must never lapse — because an LLC out of good standing cannot file evictions in Oklahoma courts. DSCR loan mechanics showing how Oklahoma's insurance premiums directly impact the coverage ratio and can push a property from loan-eligible to loan-denied between underwriting and closing. The five-year Oklahoma capital gains exemption: hold investment property for at least five consecutive years and deduct 100% of the capital gain from Oklahoma taxable income, eliminating the state's 4.5% tax entirely. BRRRR alignment: acquire, force appreciation through renovation, refinance, cash flow for 60 months, sell at month 61 with zero state capital gains tax. Conventional, DSCR, hard money, and community bank financing compared with Oklahoma-specific considerations. 1031 exchange execution. Seller financing with power of sale clause for rapid reclamation through non-judicial foreclosure.

Who This Guide Is For

This guide is for real estate investors targeting Oklahoma markets who:

- Are underwriting an Oklahoma City or Tulsa property and need the actual insurance premium range ($2,430-$6,000+) with wind/hail deductible exposure calculations — not the national average placeholder that turns a cash-flow-positive deal into a cash-flow-negative one overnight

- Are evaluating a property with foundation symptoms — stair-step cracking, separated baseboards, sticking doors — and need to understand whether they're looking at $800 in cosmetic patching or $18,000 in structural underpinning, and why hiring an independent structural engineer at $310-$780 instead of a commissioned repair salesman is the difference between accurate assessment and manufactured panic

- Are an out-of-state investor from Texas, California, or the coasts drawn to Oklahoma's rent-to-price ratios and need the complete operating framework — insurance, foundation maintenance, mineral rights, eviction mechanics, security deposit compliance, and property tax assessment resets — in one reference instead of fragments scattered across Title 41, Title 52, BiggerPockets threads, and county assessor websites

- Are targeting the military housing market at Tinker AFB or Fort Sill and need BAH rates reverse-engineered into maximum acquisition prices by rank, with sub-market mapping that identifies where E-5 families actually want to live versus where they're priced to live

- Are a Texas investor fleeing doubled property tax bills and need the direct comparison: Oklahoma's 5% annual assessment cap, 0.79-0.94% effective tax rate, and 4.5% income tax versus Texas's uncapped assessments, 1.60-1.80% effective rate, and zero income tax — with the analysis showing which trade-off favors long-term hold strategies

- Are evaluating a tax sale acquisition at the June auction and need to model quiet title costs ($2,750+), the 90-120 day timeline, the litigation risk from contested claims, and the holding costs that determine whether the discount justifies the illiquidity

- Want to structure a five-year hold that eliminates Oklahoma's 4.5% capital gains tax entirely through the state's 100% capital gains deduction for property held five consecutive years — and need the BRRRR execution timeline that aligns renovation, refinancing, and disposition with this exemption

Why Not Free Tools and Forums?

Free information on Oklahoma real estate investing exists across dozens of sources. Here's what it actually delivers:

- BiggerPockets forums are where someone in a 2022 thread says Oklahoma foundations are "no big deal — everyone has cracks," someone in 2024 posts in a panic about an $18,000 repair quote, and nobody reconciles the two positions with the engineering distinction between cosmetic settling and active structural failure. Insurance threads mention "Oklahoma is expensive" without specifying the percentage-based wind/hail deductible structure that creates $5,000-$10,000 out-of-pocket exposure on a single claim, without explaining deductible buy-down policies that convert that variable risk into a fixed expense, and without calculating the 15-35% premium discount from Class 4 impact-resistant shingles. Mineral rights discussions reference the Surface Damages Act without walking through the $25,000 bond mechanism that allows an operator to commence drilling while compensation is still being litigated. You'll find experience reports from operators who have been doing this for years mixed with advice from people who have never dealt with Oklahoma's expansive clay soil, percentage-based deductibles, or severed mineral estates. Sorting current from outdated takes longer than reading a guide that has already done it.

- Local REIA meetings — the OKC REIA and Tulsa REIA provide networking with wholesalers, title attorneys, and hard money lenders like BridgeWell Capital. They don't produce comprehensive written guides accessible to the digital consumer, don't provide systematic due diligence frameworks, and don't cover the statutory details of Title 41 security deposit escrow requirements, the criminal penalties for commingling, or the six-month reversion rule. You get connections without the compliance framework.

- National investing books and courses teach cap rate, DSCR, and 1031 mechanics that apply everywhere. They don't mention Oklahoma's percentage-based wind/hail deductibles, the expansive clay soil shrink-swell cycle, the dominant mineral estate doctrine, the criminal penalties for security deposit commingling, the property tax assessment reset upon transfer, or the five-year capital gains exemption. Applying national frameworks to Oklahoma-specific problems is how investors lose five figures on their first deal.

- DoD BAH lookup tools show you the monthly allowance by pay grade and location. They don't reverse-engineer the BAH ceiling into a maximum acquisition price, don't map target ranks to optimal sub-markets within the OKC metro, don't explain why an E-5 maps to Midwest City but an officer maps to Edmond, and don't account for the strategic difference between Tinker's diversified metro play and Lawton's pure cash-flow position with base realignment risk. You get the stipend amount without the investment framework.

This guide fills the Oklahoma-specific gap — the space between knowing how to analyze a rental property in general and knowing how to underwrite one in a state where $4,200 insurance premiums, expansive clay foundations, severed mineral rights, criminal penalties for deposit commingling, assessment resets upon transfer, and five-year capital gains exemptions can each independently determine whether a deal creates wealth or destroys it. It's the analysis that would take an Oklahoma real estate attorney, an insurance broker, a structural engineer, and a mineral rights specialist to assemble — structured as a reference you own permanently.

— Less Than One Insurance Surprise

A single insurance premium modeled at the national average instead of Oklahoma's actual $2,430-$6,000 range destroys your entire cash flow projection on day one. A foundation repair quote accepted from a commissioned salesman instead of verified by an independent structural engineer at $310-$780 can cost you $10,000 or more in unnecessary underpinning. A security deposit commingled with operating funds — even accidentally — is a criminal offense carrying up to six months in county jail and a fine of twice the amount. A property tax bill modeled from the seller's historically capped assessment instead of your actual acquisition price understates your holding costs from the first year of ownership. A mineral lease you didn't discover in the abstract can result in drilling equipment arriving on your residential lot with a $25,000 bond and a court-appointed appraiser.

This guide doesn't replace your Oklahoma real estate attorney, your insurance broker, or your structural engineer. But it gives you the insurance underwriting framework, foundation assessment protocol, mineral rights due diligence checklist, landlord-tenant compliance system, property tax calculation methodology, and military housing economics analysis that ensure you identify every Oklahoma-specific risk before you're contractually committed — instead of discovering them on your first insurance renewal, your first hailstorm deductible, your first foundation inspection, or your first security deposit dispute.

If it catches a single insurance underwriting error, prevents a single security deposit compliance violation, or saves you from accepting a single unnecessary foundation repair quote, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't sharpen your underwriting and protect your capital in Oklahoma's operating environment, you pay nothing.

Download the free Oklahoma Quick-Start Home Buying Checklist to see the due diligence framework covering insurance verification, foundation assessment, mineral rights review, security deposit compliance, and property tax modeling. When you're ready for the full insurance underwriting system, foundation maintenance protocols, military BAH tables, landlord-tenant compliance navigator, and 20-chapter investment guide, the complete guide is here.

The deal looks good on the spreadsheet. This guide tells you whether Oklahoma agrees.