Your Loan Estimate Showed $13,734 in Transfer Tax. Your Agent Said That's Normal for Philadelphia.

You found a $300,000 rowhouse in Fishtown. Your lender sent the Loan Estimate, and there it was: $13,734 in realty transfer tax. You called your agent, and she told you that's the standard Philadelphia rate — 4.578% of the purchase price split between you and the seller. Your share: $6,867 in pure cash, on top of your down payment, lender fees, title insurance, and escrow deposits. Nobody mentioned this number during the pre-approval conversation. Nobody mentioned it during the house hunt. The first time you saw it was on the document that also told you the closing date was 28 days away.

Or maybe you're buying in Pittsburgh, where the transfer tax is even worse: 5% total — a 1% state tax, a 3% city tax, and a 1% school district tax. On that same $300,000 home, you owe $7,500 at closing. But your cousin bought a place across the street in Mount Lebanon last year and only paid 2%. The difference? A municipal boundary line running down the middle of the road that nobody pointed out until the title search.

Or maybe it's not the closing costs. Maybe it's what comes after. You bought a renovated home in Allegheny County and budgeted your mortgage payment using the seller's property tax bill — $2,400 a year based on a decades-old assessment. Three months after closing, the school district filed an appeal. Your new assessment was calculated at your purchase price times the 52.7% Common Level Ratio, and your annual tax bill jumped to over $8,000. Your lender adjusted your escrow, and your monthly payment climbed $470. Nobody told you school districts in Allegheny County routinely appeal new purchases. Nobody told you the seller's tax bill was based on a "base year" assessment from a different era. You planned your budget around a number that was never going to survive your closing date.

The problem is not that Pennsylvania is expensive. The problem is that Pennsylvania layers a transfer tax system where rates swing from 2% to 5% depending on which side of a municipal boundary you buy on, imposes a 3.74% wage tax on every dollar earned inside Philadelphia, runs a property assessment system in Allegheny County where school districts routinely appeal new buyers to inflate their tax base, sits atop abandoned coal mines in 43 of 67 counties where standard homeowners insurance explicitly excludes collapse damage, registers radon levels among the three highest in the nation across a geological formation running beneath the southeast, and offers PHFA assistance programs worth up to $6,000 at 0% interest or 5% of your purchase price forgivable over ten years — and no single resource maps all of these into a decision framework you can work through before you sign.

The Pennsylvania First-Time Home Buyer Guide is a Keystone Closing Cost Defense System — a structured walkthrough of every Pennsylvania-specific transfer tax calculation, environmental liability, assessment trap, and assistance program that determines whether your purchase protects you or bankrupts you. It replaces months of cross-referencing PHFA program portals, county assessment databases, DEP mine subsidence maps, radon zone reports, and r/philadelphia threads with a single reference that tells you exactly what to verify, exactly when your cash-to-close is at risk, and exactly where Pennsylvania transactions destroy first-time buyers who assumed national advice applied to the Keystone State.

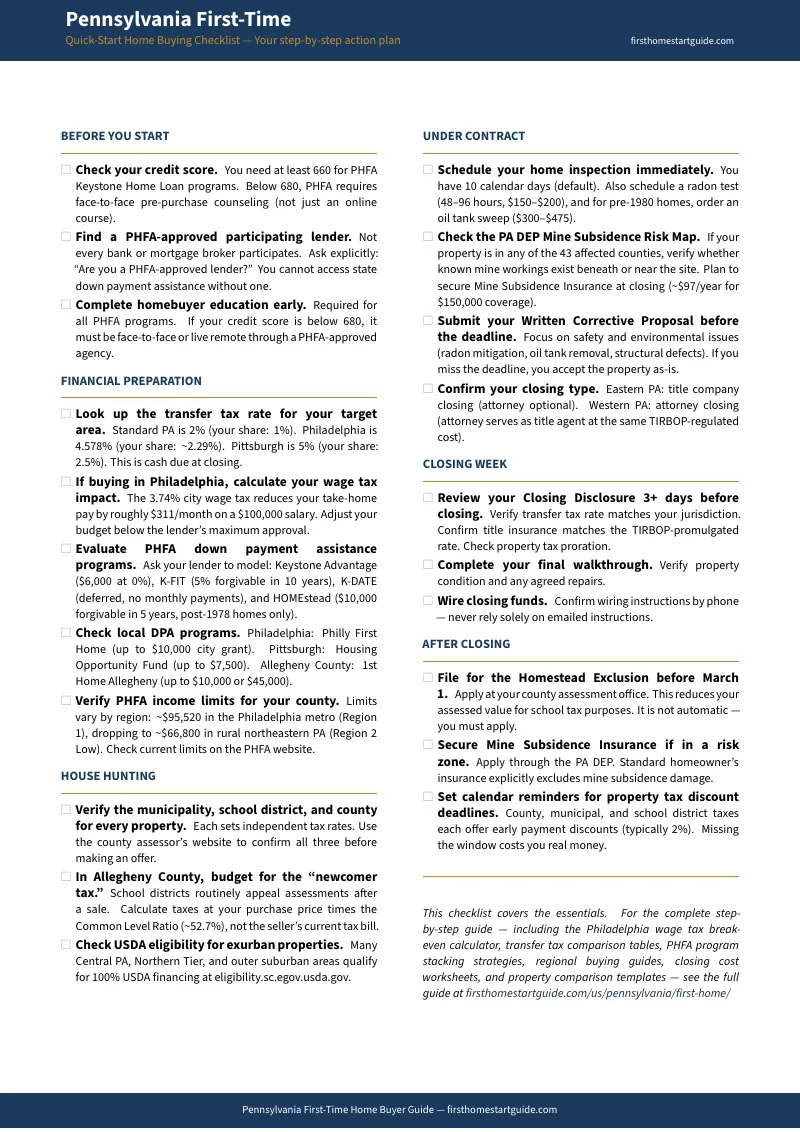

What's Inside the Keystone Closing Cost Defense System

A comprehensive guide, a quick-start checklist, and 8 standalone worksheets and reference cards — 10 printable PDFs covering every stage from pre-approval through post-purchase setup, built specifically for the tax structures, environmental hazards, and assistance programs that make Pennsylvania unlike any other state:

Transfer Tax Calculator and Municipal Boundary Guide

Pennsylvania's transfer tax is not one rate. The state charges 1%, then your municipality and school district add their own — creating a patchwork where Philadelphia charges 4.578% total, Pittsburgh charges 5%, and most other jurisdictions charge 2%. The difference between buying on one block versus the next can cost you thousands. The guide breaks down how the two-part system works (state versus local), which municipalities levy the highest rates, how the customary 50/50 buyer-seller split works and when you can negotiate it differently, and how to calculate your exact cash-to-close transfer tax obligation before you submit an offer. In Philadelphia, this section alone shows you why the $6,867 on your Loan Estimate is real, unavoidable, and must be in your bank account — not financed — on closing day. Failure to pay within 30 days of closing triggers penalties up to 50% of the unpaid tax.

Philadelphia Wage Tax Affordability Worksheet

When you move inside Philadelphia city limits, you lose 3.74% of your gross income to the city wage tax before your mortgage payment, property tax, insurance, or any other expense. On a $100,000 household income, that is $3,740 per year — $311 per month — that disappears from your take-home pay. No national mortgage calculator includes this. No generic affordability guide accounts for it. The worksheet models your true Philadelphia affordability by layering the wage tax into your debt-to-income calculation, showing you exactly how much less house you can afford inside the city versus the collar counties. For non-residents working in Philadelphia who live in the suburbs, the guide covers the 3.43% commuter withholding and shows how to calculate whether the property tax savings of suburban living offset the wage tax you still owe.

PHFA Program Navigator: Keystone Advantage and K-FIT

The Pennsylvania Housing Finance Agency offers two programs that can fundamentally change your closing economics — but navigating the PHFA website is a bureaucratic maze with no decision framework. The Keystone Advantage Assistance Loan provides up to 4% of the purchase price or $6,000 (whichever is less) at 0% interest, amortized over 10 years. The K-FIT program provides up to 5% of the purchase price with no dollar cap, and the entire loan is forgiven if you stay in the home for 10 years — effectively a pure grant. But K-FIT requires a minimum 660 credit score and caps liquid assets at $50,000 after deducting closing funds. The guide lays out the income limits by region (they vary dramatically — $95,520 in the Philadelphia suburbs versus $66,800 in Lackawanna County), the exact eligibility criteria for each program, and how to sequence your application so your lender submits to PHFA correctly the first time.

Allegheny County Reassessment Defense

If you are buying in Allegheny County — Pittsburgh, its boroughs, or the surrounding townships — you need to understand the "newcomer tax" before you budget your monthly payment. Allegheny County uses a base-year assessment system that pegs property values to historic levels. When you buy a home for significantly more than its assessed value, the school district files an annual appeal to reassess the property at your purchase price multiplied by the Common Level Ratio (currently 52.7%). A home assessed at $120,000 that you purchase for $400,000 can be reassessed to $210,800 — nearly doubling your property tax overnight. The guide explains how the CLR calculation works, which school districts appeal most aggressively, how to project your post-appeal tax bill before making an offer, and how to file a counter-appeal if the reassessment exceeds fair market value.

Radon Testing Protocol for High-Risk Counties

Pennsylvania ranks in the top three states nationally for dangerous radon levels, with approximately 40% of homes testing above the EPA action limit. The geological cause is the Reading Prong — a band of uranium-rich metamorphic rock running beneath Northampton, Lehigh, Berks, Bucks, and Montgomery counties, placing radioactive gas within feet of residential basement slabs. While Pennsylvania law does not mandate radon testing, the Seller Disclosure Act requires disclosure of known elevated results, and any competent buyer should treat testing as non-negotiable. The guide covers how to conduct a 48-to-96-hour continuous monitor test during your inspection period, how to interpret results against the 4.0 pCi/L EPA action limit, how to use the Written Corrective Proposal to demand remediation, and what an Active Soil Depressurization system costs ($843 to $1,500 installed by a DEP-certified mitigator). Skipping this test to win a bidding war means breathing a Class A carcinogen every day you own the home.

Coal Mine Subsidence and Underground Oil Tank Assessment

Over one million Pennsylvania homes sit atop abandoned underground coal mines spanning 43 of 67 counties. When century-old mine supports collapse, the surface above fails — and standard homeowners insurance explicitly excludes earth movement damage. A sudden subsidence event can cause hundreds of thousands of dollars in structural damage or total property loss. The guide shows you how to check the PA DEP Mine Subsidence Risk Map for your property, how to secure the state's heavily subsidized Mine Subsidence Insurance ($97 per year for $150,000 in coverage), and how to make MSI part of your closing checklist. The guide also covers underground heating oil tanks — buried steel tanks that corrode and leak, triggering soil remediation costs of $15,000 to $60,000. You'll learn when to order a tank sweep ($300 to $475), how to negotiate removal before closing ($2,000 to $4,000), and the limits of the DEP's Underground Storage Tank Indemnification Fund ($4,000 maximum reimbursement after a $1,000 deductible).

Regional Closing Guides

Five distinct Pennsylvania markets with current pricing, tax structures, and financing strategies: Philadelphia (4.578% transfer tax, wage tax modeling, PHFA Region 1 income limits), Philadelphia Collar Counties (Delaware, Montgomery, Bucks, Chester — suburban property tax millage rates, commuter wage tax, school district comparisons), Pittsburgh and Allegheny County (5% transfer tax, reassessment defense, CLR projections), Central Pennsylvania (Lancaster, York, Harrisburg — PHFA access, rural development loans, older housing stock), and University and Military Markets (State College's 4% transfer tax, VA loan layering with PHFA, Carlisle Barracks area).

Closing Cost Worksheet and Transaction Timeline

A fillable worksheet covering every Pennsylvania-specific closing cost line item: state and local transfer tax (calculated for your municipality), title insurance, recording fees, lender fees, homeowners insurance, escrow deposits, and PHFA program integration. Plus a complete transaction timeline from pre-approval through deed recording — inspection contingency windows, radon testing scheduling, oil tank sweep timing, PHFA underwriting submission, and closing day procedures.

Who This Guide Is For

- Philadelphia renters buying their first rowhouse who need to calculate the real cost of homeownership inside city limits — transfer tax at 4.578%, wage tax at 3.74%, and property tax — before they discover at closing that the $300,000 home requires $6,867 in transfer tax cash they did not budget for

- Suburban buyers in the collar counties (Delaware, Montgomery, Bucks, Chester) who assume escaping Philadelphia's wage tax means lower costs, only to find property tax bills of $8,000 to $12,000 annually on a moderately priced home — and who need to model the real break-even between city wage tax and suburban property tax

- Pittsburgh and Allegheny County buyers who are budgeting their mortgage payment using the seller's historic property tax bill and do not know that the school district will appeal their assessment within months of closing, potentially adding $3,000 to $5,000 to their annual tax burden

- PHFA-eligible buyers across the state who know down payment assistance exists but cannot navigate the program maze — Keystone Advantage versus K-FIT, income limits that vary by region, credit score minimums, asset caps — and need a single reference that tells them exactly which program fits their situation

- Out-of-state relocators who have bought homes in other states and assume 2% to 3% closing costs are normal, do not know that Pennsylvania splits transfer tax between buyer and seller, and have never budgeted for radon remediation, coal mine subsidence insurance, or underground oil tank removal

- Buyers in coal country and the Reading Prong who need to understand the environmental liabilities hiding beneath their prospective home — radon gas, abandoned mine shafts, buried heating oil tanks — and the specific inspections, insurance policies, and remediation costs that protect them from catastrophic loss

Why Not Free Tools and Forums?

Free information on buying a home in Pennsylvania exists. Here is what it actually delivers:

- Zillow and NerdWallet closing cost calculators use national averages and tell you to budget 2% to 3% for closing costs. In Philadelphia, the transfer tax alone is 4.578% of the purchase price. In Pittsburgh, it is 5%. These calculators do not include the municipal boundary variations, do not split the buyer's share from the seller's share, and do not warn you that this cash cannot be financed — it must be in your account on closing day. Following their advice means showing up to closing $5,000 to $10,000 short.

- The PHFA website gives you program descriptions, income limit tables by region, and approved lender lists scattered across dozens of PDF documents and web pages. It does not tell you whether Keystone Advantage or K-FIT is the better option for your income and credit profile, does not explain the asset cap that disqualifies buyers with more than $50,000 in liquid assets, and does not show you how to coordinate PHFA underwriting with your lender's timeline. You get eligibility data without a decision framework.

- Reddit threads (r/philadelphia, r/Pittsburgh, r/FirstTimeHomeBuyer) contain genuine transfer tax horror stories and wage tax warnings, but mixed with advice from buyers who confuse state tax with local tax, do not understand the 50/50 split convention, and recommend skipping radon testing because "every house in PA has radon." Sorting current law from outdated anecdote takes longer than reading a guide that already did it.

- Local real estate agent blogs write about "5 things to know about buying in Philadelphia" or "Pittsburgh home buying tips" designed to capture lead-generation inquiries. They do not cover the Allegheny County reassessment appeal process, do not explain mine subsidence insurance, do not detail the DEP oil tank remediation fund, and do not provide fillable worksheets for calculating your municipality-specific closing costs. You get marketing content, not analytical tools.

This guide fills the Pennsylvania-specific gap — the space between knowing how to buy a home in general and knowing how to buy one in a state where transfer tax rates swing from 2% to 5% depending on your street address, a 3.74% wage tax restructures your entire affordability calculation, school districts appeal new buyers to inflate property assessments, and environmental hazards beneath the surface require inspections and insurance that no national guide mentions. It is the analysis that would take a real estate attorney, a PHFA-approved lender, a DEP-certified radon mitigator, and a structural engineer to assemble — structured as a reference you own permanently.

— Less Than One Hour of Attorney Time

A real estate attorney in Pennsylvania charges $1,500 to $3,000 for a residential closing. A radon mitigation system you did not know you needed costs $843 to $1,500. An underground oil tank remediation you did not catch before closing costs $15,000 to $60,000. An Allegheny County reassessment you did not anticipate adds $3,000 to $5,000 to your annual property tax. Not knowing about K-FIT means missing up to 5% of your purchase price in forgivable assistance. Budgeting with national closing cost averages in Philadelphia means arriving at closing $5,000 to $10,000 short on cash.

This guide does not replace your real estate attorney, your lender, or your home inspector. But it gives you the transfer tax calculations, environmental checklists, assessment defense strategies, and program navigation that ensure you identify every Pennsylvania-specific risk and opportunity before your deposit is at stake — instead of discovering them on the Loan Estimate, at the inspection, or on your first reassessed property tax bill.

If it catches a single transfer tax miscalculation before you sign, prevents a single reassessment surprise in Allegheny County, connects you with PHFA assistance worth $6,000 to 5% of your purchase price, or reminds you to check the mine subsidence risk map before you close in coal country, it pays for itself before you have finished reading it.

30-day money-back guarantee. If the guide does not sharpen your Pennsylvania home buying analysis and protect your closing, you pay nothing.

Download the free Pennsylvania Quick-Start Home Buying Checklist to see the step-by-step framework covering financial preparation, transfer tax calculation, program eligibility, environmental due diligence, offer and close, and post-purchase essentials. When you are ready for the full transfer tax calculator, wage tax worksheet, PHFA comparison card, radon testing protocol, mine subsidence checklist, closing cost worksheet, and the complete guide with regional market analysis, the full 10-PDF toolkit is here.

Pennsylvania rewards buyers who understand the tax system underneath the listing price. This guide makes sure you do.