The House Was Built in 1920. The Lead Paint Laws Changed Six Months Ago. Your Tenants Can Now Withhold Rent Into a Court Escrow Account, and Nobody Told You the Homestead Exemption Has a Filing Deadline.

You found a triple-decker in Providence. The numbers looked beautiful -- buy the building with 3.5% down, live in one unit, rent the other two for $1,400 each, and cut your effective housing cost to $1,070 a month. Your agent said "house hacking" was how half the landlords in the city got started. You ran the PITI against your income, got pre-approved, and made an offer.

Then Rhode Island happens. Your closing attorney calls and says, "This property was built before 1978. As of January 2024, the owner-occupant exemption for lead paint compliance has been eliminated. You are now required to obtain a Certificate of Lead Conformance for the entire building -- all three units -- before renting." You get quotes: $20,000 to repaint the exterior to inspection standards, $30,000 if you wrap it in vinyl siding, $5,000 per unit for interior remediation. Meanwhile, your lender calculates property taxes at Providence's non-owner-occupied rate of $29.20 per $1,000 -- not the $8.40 owner-occupied rate -- because nobody filed the homestead exemption for you, and your monthly payment just tripled what you modeled. Then your insurance agent asks whether you checked the FEMA flood map. The property sits in an AE zone along the Providence River. Annual flood insurance: $3,200. You budgeted zero.

Here's what no single free resource explains: Rhode Island layers mandatory attorney-driven closings where a licensed lawyer must handle your title search, deed drafting, and fund disbursement at $800 to $1,500 in non-negotiable fees, against the most aggressive lead paint enforcement regime in New England where the 2024 elimination of the owner-occupant exemption means buying a pre-1978 multi-family triggers mandatory lead certification with treble damages for violations and tenant escrow rights that can sever your rental income overnight, against a Providence split-rate property tax system where missing the March 15 homestead exemption deadline means paying $29.20 per $1,000 instead of $8.40 -- a $6,240 annual penalty on a $300,000 home, against FEMA Risk Rating 2.0 flood insurance premiums that affect not just waterfront properties but suburban neighborhoods in Warwick, Cranston, and East Providence where annual premiums in AE zones run $1,500 to $6,000, against RIHousing DPA programs offering $15,000 to $25,000 in assistance but requiring you to navigate overlapping credit score thresholds, geographic restrictions to specific census tracts, and stacking rules that most buyers never decode, against a municipal tax system where 39 towns set independent rates creating $3,000 to $7,000 annual differences between adjacent municipalities on the same assessed value, against nine-year revaluation cycles that trigger tax spikes of 50% to 100% with no warning. Each of these has cost real first-time buyers thousands of dollars because the information existed -- scattered across RIHousing program sheets, municipal tax assessor websites, the Attorney General's lead paint enforcement page, FEMA flood maps, and Reddit threads from buyers who discovered the homestead exemption deadline six months too late -- but nobody had assembled it into a single decision system calibrated to how Rhode Island actually works.

The Rhode Island First-Time Home Buyer Guide is an Ocean State Closing Blueprint -- not a generic overview of the home buying process, but a structured reference that maps every RI-specific legal mechanism, tax calculation, assistance program, environmental liability, and coastal risk factor into a process you work through before your earnest money is at risk. It replaces months of cross-referencing RIHousing income limit matrices, municipal tax rate tables, DOH lead paint registry requirements, FEMA flood zone maps, and forum posts with a single guide that tells you exactly what to verify, exactly what the numbers should look like, and exactly where deals go wrong in this state.

What's Inside the Ocean State Closing Blueprint

A comprehensive 14-chapter guide, a quick-start checklist, and 4 RI-specific worksheets -- covering every stage from pre-approval through post-closing, built specifically for the legal mechanisms, tax structures, assistance programs, environmental liabilities, and coastal risks that make Rhode Island a deceptively complex real estate market:

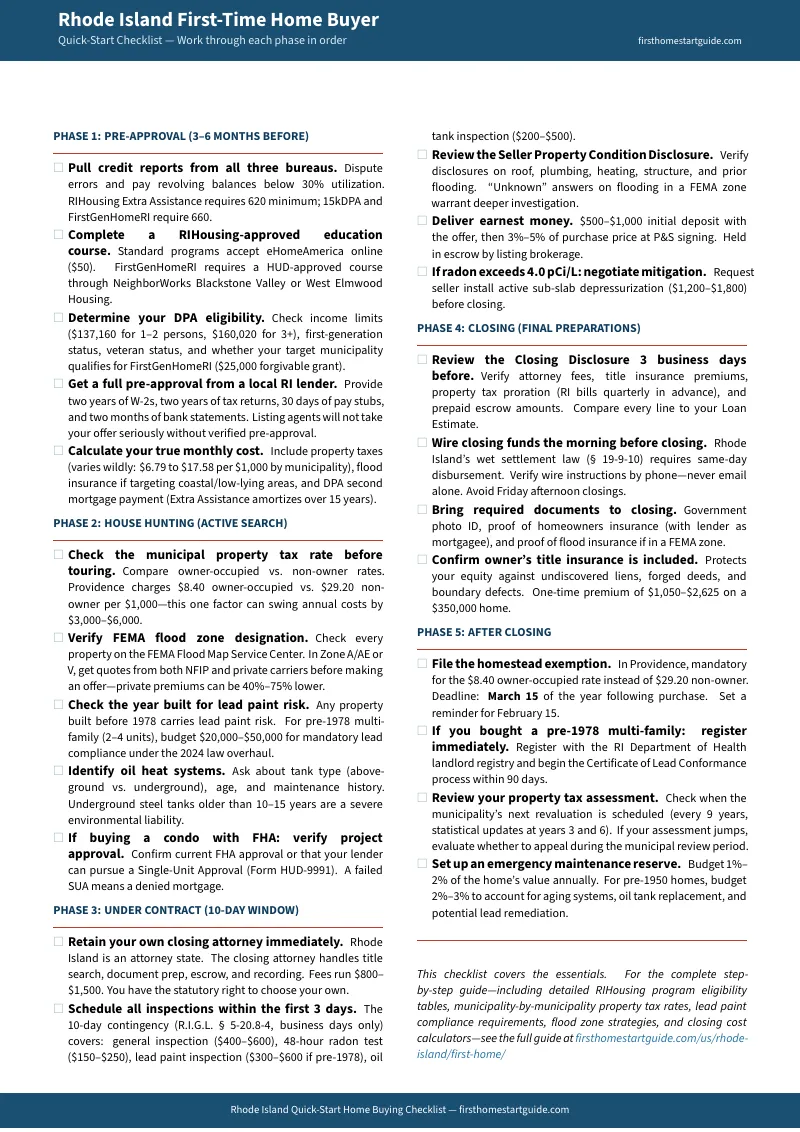

The Attorney-Driven Closing Process

Rhode Island law treats the examination of title and drafting of a deed as the practice of law. A licensed attorney -- not a title company or escrow agent -- must handle your closing. The guide explains exactly what the closing attorney does: 40-year title examination of municipal land evidence records, document preparation, IOLTA trust account escrow management, and same-day deed recording. It covers the wet settlement mandate under R.I.G.L. Section 19-9-10 requiring all loan proceeds to be fully disbursed on the day the mortgage is recorded, why Friday afternoon closings are dangerous and most experienced attorneys refuse them, the statutory right to choose your own attorney, typical fees ($800 to $1,500, up to $3,000 for complex historic or coastal properties), and the warranty deed vs. quitclaim deed distinction that determines whether you have legal recourse if a title defect surfaces years later.

Lead Paint Compliance Under the 2024 Law Overhaul

The single most consequential due diligence issue for Rhode Island buyers targeting multi-family homes. The guide covers the elimination of the owner-occupant exemption effective January 1, 2024, which means buying a pre-1978 triple-decker and renting out units now triggers mandatory Certificate of Lead Conformance requirements for the entire property. It explains the two-year CLC renewal cycle, the DOH public registry requirement effective September 2024, treble damages for violations plus mandatory attorney fee awards, the tenant escrow right that allows renters to redirect payments to a court-managed account if your CLC lapses, the expanded inspection window for properties built before 2011 covering lead water service lines, and the financial reality of compliance: $20,000 or more for exterior repainting, $30,000 minimum for vinyl siding, $5,000 per unit for interior remediation, and the difficulty of finding certified abatement contractors quoting reasonable rates. The guide also covers the FHA 203(k) renovation loan strategy for financing lead abatement into the mortgage instead of paying out of pocket.

RIHousing Down Payment Assistance Decision Framework

Rhode Island offers some of the most generous DPA programs in New England, but they layer on top of each other with different credit score thresholds, geographic restrictions, and repayment structures that are nearly impossible to compare without a structured breakdown. The guide maps every program: the Extra Assistance loan providing up to $20,000 (6% of purchase price) as a fully amortizing second mortgage at your first mortgage rate with a 620 minimum credit score, the 15kDPA offering $15,000 as a zero-interest deferred loan with no monthly payments but requiring 660 credit, the FirstGenHomeRI pilot providing $25,000 in forgivable grants after five years of owner-occupancy but restricted to specific census tracts in Central Falls, Pawtucket, Woonsocket, East Providence, and parts of Providence and Newport, and AnchorHome eliminating PMI entirely on an $80 million program for homes up to $525,000. It shows exactly which programs stack, which ones replace each other, and which credit score thresholds unlock the most lucrative combinations.

Property Tax Decoder

Rhode Island property taxes are administered by 39 independent municipalities with wildly divergent rates. The guide explains Providence's split-rate system -- $8.40 per $1,000 for owner-occupants versus $29.20 for non-owner-occupied properties -- and the March 15 homestead exemption filing deadline that nobody files for you. It provides a full municipal rate comparison table showing that the same $300,000 home costs $2,520 per year in property taxes in Providence (with exemption) versus $5,274 in North Providence -- a $2,754 annual difference between adjacent cities. It covers the mandatory nine-year revaluation cycles that trigger sudden tax spikes, the 2026 "Taylor Swift Tax" imposing a statewide surcharge on non-owner-occupied properties assessed above $1 million, and the quarterly advance billing structure that determines how much cash your lender will require in escrow at closing.

Flood Insurance and Coastal Buying

Rhode Island has over 400 miles of coastline, and flood zones extend surprisingly far inland through Narragansett Bay, tidal rivers, and coastal salt ponds. The guide covers FEMA flood zone designations with typical premium ranges ($300 to $900 for X zones, $1,500 to $6,000 for AE zones, $3,000 to $10,000 or more for V zones), Risk Rating 2.0's property-specific repricing with 18% annual increase caps that compound over years, and the private flood insurance market that can cut premiums by 50% to 75%. Real New England case studies show NFIP quotes of $4,200 replaced by private options at $1,050 -- a $3,150 annual savings. It explains Elevation Certificates, CRMC coastal jurisdiction and setback rules, seawall maintenance liability, and why suburban neighborhoods in Warwick and East Providence carry flood risk that feels impossible until you check the map.

Military Buyers at Naval Station Newport

A dedicated chapter for active-duty military and veterans stationed at Naval Station Newport and the Naval War College. It includes 2026 BAH rates by rank (E-5 through O-5) with approximate buying power calculations for VA 0% down loans, Newport's exceptionally low $8.69 per $1,000 property tax rate compared to neighboring Middletown ($11.47) and Portsmouth ($10.23), the VA Minimum Property Requirements that clash with Rhode Island's pre-1950 housing stock -- particularly the peeling paint flag that kills deals when sellers refuse to remediate -- strategies for VA buyers including the seller credit workaround and post-1978 targeting, and the PCS rental conversion strategy leveraging Newport's constant influx of Naval War College faculty and defense contractors.

The Five Micro-Markets

Despite functioning as one metro, Rhode Island segments into five distinct micro-markets with different price dynamics, tax burdens, and environmental risks. The guide profiles each: Providence Core and Urban Ring (house hacking territory with lead paint risk), Blackstone Valley (lowest price points with FirstGenHomeRI eligibility), East Bay (top schools in Barrington with steep taxes), Aquidneck Island (Newport's low mill rate and military buyer ecosystem), and South County (coastal lifestyle with the highest flood insurance exposure in the state). Each profile includes advantages, risks, and the specific DPA programs and tax structures that apply.

Closing Cost Breakdown

RI closing costs run 2% to 5% of the purchase price. The guide itemizes every buyer cost on a $350,000 purchase ($5,350 to $14,600): lender origination, closing attorney fees, title insurance (owner and lender policies), property inspections (general, lead, radon, oil tank), prepaid escrow deposits, and recording fees. It covers the Real Estate Conveyance Tax at $2.30 per $500 with the $800,000 surcharge, non-resident seller withholding requirements (6% individual, 9% corporate), and the two-stage earnest money structure ($500 to $1,000 initial deposit, 3% to 5% at Purchase and Sale signing).

Environmental Hazards Beyond Lead Paint

Radon testing ($150 to $250), oil tank inspection ($200 to $500), and septic system evaluation ($300 to $500). Rhode Island's reliance on heating oil means many properties have above-ground or underground storage tanks with a structural lifespan of only 10 to 15 years. A breached tank triggers strict liability for all soil remediation and groundwater cleanup -- costs that run into the tens of thousands and are not covered by standard homeowners insurance. The guide covers what to look for, what to negotiate, and when to walk away.

RI-Specific Worksheets

Four standalone worksheets you can print and use immediately:

- Budget Worksheet -- Goes beyond PITI to include property taxes calculated by municipality, flood insurance, mortgage insurance, DPA second mortgage payments, and the DTI calculation that accounts for Rhode Island's 5.99% state income tax rate reducing your effective qualifying income

- Closing Cost Estimator -- Fillable worksheet itemizing every RI-specific cost: attorney fees, title insurance, inspections (general, lead, radon, oil tank, septic), prepaid escrows, and recording fees

- Property Comparison Worksheet -- Side-by-side comparison for three properties covering municipality, tax rate, flood zone, lead paint risk, oil heat, septic status, homestead exemption availability, DPA eligibility, and net monthly housing cost

- DPA Program Eligibility Checker -- Assessment covering credit score, income, household size, first-time and first-generation status, target municipality, and geographic eligibility for every RIHousing program

Who This Guide Is For

This guide is for first-time home buyers in Rhode Island who:

- Are targeting a Providence triple-decker as a house-hacking strategy -- and need to understand why the 2024 lead paint law overhaul eliminated the owner-occupant exemption, how mandatory Certificate of Lead Conformance requirements add $20,000 to $50,000 above the purchase price, how tenant escrow rights can sever your rental income if your CLC lapses, and whether an FHA 203(k) renovation loan can finance the abatement into the mortgage

- Are buying anywhere in Providence and don't know about the homestead exemption -- and need to understand that missing the March 15 filing deadline means paying $29.20 per $1,000 instead of $8.40 on every dollar of assessed value, that nobody files this for you, and that the penalty is immediate and retroactive for the entire fiscal year

- Are stationed at Naval Station Newport or the Naval War College -- and need 2026 BAH buying power calculations by rank, Newport's $8.69 mill rate advantage over neighboring towns, VA Minimum Property Requirement workarounds for historic homes with peeling paint, and the PCS rental conversion strategy that turns your tour-length purchase into a positive-cash-flow rental when you receive new orders

- Are moving from Massachusetts and looking for relative affordability in Rhode Island -- and need to know that attorney-driven closings are non-negotiable and cost $800 to $1,500, that flood zones extend far beyond the waterfront into suburban neighborhoods you assumed were safe, and that each of Rhode Island's 39 municipalities sets its own tax rate with no statewide consistency

- Are a first-generation homebuyer in Central Falls, Pawtucket, or Woonsocket -- and want the $25,000 forgivable FirstGenHomeRI grant but need help confirming your target property falls within the eligible census tracts, meeting the 660 credit score threshold, and completing the HUD-approved counseling course that the standard eHomeAmerica online course does not satisfy

- Are looking at coastal properties in South County or along Narragansett Bay -- and need to understand FEMA's Risk Rating 2.0 repricing, the private flood insurance market that can cut premiums by 50% to 75%, Elevation Certificate strategy, and CRMC coastal jurisdiction rules that control what you can build, expand, or repair on your property

- Want every RI-specific legal mechanism, tax calculation, assistance program, environmental liability, and coastal risk factor in one reference -- instead of assembling it from RIHousing program sheets, municipal tax assessor offices, DOH lead paint registry guidance, FEMA flood maps, CRMC coastal regulations, and Reddit threads from buyers who learned the hard way

Why Not Free Tools and Forums?

Free information on buying a home in Rhode Island exists. Here's what it actually delivers:

- RIHousing's website publishes program guidelines, income limits, and participating lender lists. It doesn't explain the strategic difference between the Extra Assistance loan (monthly payments, 620 credit) and the 15kDPA (no payments, 660 credit), doesn't show which programs stack and which replace each other, and doesn't map the geographic boundaries that restrict FirstGenHomeRI to specific census tracts. You get program specifications without a decision framework for navigating them.

- Zillow and Realtor.com show estimated monthly payments using approximate tax figures. In a state where Providence charges owner-occupants $8.40 per $1,000 but penalizes non-filers at $29.20, and where adjacent municipalities can differ by $5,000 per year in property tax on the same home, those estimates can be off by $300 to $600 per month. No listing site warns you about the homestead exemption deadline, the lead paint law overhaul, or the escrow seed that can reach $5,000 in a high-tax municipality.

- Real estate brokerage blogs highlight Providence's walkable neighborhoods, Newport's charm, and South County's coastline. They don't explain that buying a pre-1978 triple-decker triggers tens of thousands in mandatory lead compliance costs, don't mention the tenant escrow rights that can freeze your rental income, and never discuss the private flood insurance market that can save buyers thousands per year. The content generates leads. It doesn't identify reasons to slow down.

- Reddit threads (r/RhodeIsland, r/providence) contain genuine buyer experiences -- homestead exemption horror stories, lead paint contractor nightmares, revaluation tax spikes, flood insurance sticker shock. But advice from 2022 doesn't reflect the 2024 lead paint law overhaul, current RIHousing income limits, or the 2026 "Taylor Swift Tax." One homeowner documented a $17,000 quote just to paint a stairwell. The frustration is real, but sorting current guidance from outdated venting takes longer than reading a guide that has already done it.

This guide fills the Rhode Island-specific gap -- the space between knowing how to buy a house in general and knowing how to buy one in a state where a licensed attorney must handle your closing, where buying a pre-1978 rental property triggers mandatory lead certification with treble damages for non-compliance, where a missed filing deadline can triple your property tax rate, where flood insurance in a suburban neighborhood can exceed your annual property tax bill, and where $25,000 in forgivable down payment assistance is available but restricted to specific census tracts that most buyers never check. It's the analysis that would take a Rhode Island real estate attorney, a RIHousing-approved lender, and a certified lead inspector to assemble -- structured as a reference you own permanently.

-- Less Than One Hour With a Rhode Island Closing Attorney

A Rhode Island closing attorney charges $800 to $1,500 for a standard transaction. Lead paint compliance on a triple-decker runs $20,000 to $50,000. Missing the homestead exemption in Providence costs $6,240 per year on a $300,000 home. Failing to check the FEMA flood map before making an offer can add $3,000 to $6,000 in annual insurance premiums you never budgeted. Not knowing the FirstGenHomeRI geographic restrictions means leaving $25,000 in forgivable grants on the table.

This guide doesn't replace your closing attorney or your lender. But it gives you the attorney-driven closing mechanics, lead paint compliance framework, DPA program analysis, property tax decoder, flood insurance strategy, and closing cost breakdown that ensure you identify every Rhode Island-specific risk before your earnest money is committed -- instead of discovering them during title search, on your first quarterly tax bill, or when a lead inspector quotes $30,000 to wrap your building in vinyl siding.

If it catches a single homestead exemption deadline, prevents a single lead paint compliance surprise, or helps you claim $25,000 in forgivable assistance you qualified for, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't sharpen your decision-making and protect your investment in the Ocean State's deceptively complex real estate market, you pay nothing.

Download the free Rhode Island Quick-Start Home Buying Checklist to see the action plan covering pre-approval, attorney selection, property search, closing preparation, and post-closing protection. When you're ready for the full closing mechanics, lead paint compliance framework, DPA decision system, property tax decoder, and flood insurance strategy, the complete guide is here.

The triple-decker looks like a wealth-building machine on a spreadsheet. This guide tells you whether Rhode Island's lead paint laws, property tax system, and flood maps agree.