The Spreadsheet Says Cash Flow. Rhode Island's Lead Paint Registry, Flood Premiums, and 20-Day Deposit Rule Say Otherwise.

You found a $550,000 triple-decker in Providence generating $6,800/month across three units. Or a coastal duplex in Narragansett with a $9.50 mill rate that looks absurdly low compared to neighboring Connecticut. Or a single-family near Brown University where per-bedroom leasing could push gross yield past 8%. The cap rate clears. The DSCR works. You're ready to wire earnest money.

Then Rhode Island shows up. The triple-decker was built in 1912, which means every unit needs a Certificate of Lead Conformance renewed every two years — and the state's rental registry auto-cross-references your CLC status. One lapsed certificate and you can't file evictions (since October 2024), you're accumulating $125/unit/month in fines, and your tenant can escrow rent with the court. The Narragansett coastal deal has a FEMA Zone VE designation you didn't check — flood insurance under Risk Rating 2.0 comes back at $22,000/year, consuming 31% of gross rent before taxes or debt service. The Brown University rental violates Providence's 3-unrelated-person occupancy limit, and the city enforces it. The tenant who moved out last week? You have 20 days — not the 30 or 60 days you're used to — to return the security deposit, or you owe double the amount plus their attorney's fees.

Here's the problem: Rhode Island combines mandatory recurring lead paint inspections with an enforcement regime that blocks evictions for non-compliance, a flood insurance landscape where two adjacent properties can have premiums differing by $15,000/year, university housing zoning that caps occupancy at 3 unrelated persons in Providence, a conveyance tax that increased 63% in October 2025, a new "Taylor Swift Tax" on vacant luxury properties effective July 2026, a 20-day security deposit deadline with double-damages penalties, and a judicial foreclosure process that takes 12-18 months — all in a state small enough that every deal falls under the same regulatory apparatus. Each of these has destroyed real investors' returns because the information existed in scattered municipal codes, dormant forum threads, and FEMA portals — but nobody had organized it into a system that tells you what to check before you're contractually committed.

The Rhode Island Investment Property Guide is a Regulatory Moat Investor System — not a motivational overview of real estate investing, but a structured compliance and due diligence framework that maps every Rhode Island-specific tax trap, lead paint requirement, flood insurance variable, zoning restriction, and landlord-tenant deadline into a process you work through before you sign a purchase agreement. It replaces months of cross-referencing the rental registry, FEMA flood maps, municipal zoning codes, and legislative updates with a single reference that tells you exactly what to verify, exactly what the numbers should look like, and exactly where deals die in this state. The name captures the core thesis: Rhode Island's regulatory density isn't a barrier — it's a moat that protects investors who understand it from competition that doesn't.

What's Inside the Regulatory Moat Investor System

A 15-chapter guide, a 20-item due diligence checklist, and 8 standalone printable tools — covering every stage from market selection through exit planning, built specifically for the financial traps and regulatory complexity that make Rhode Island unlike any other state:

Lead Paint Compliance System (CLC + Rental Registry)

The single most dangerous compliance area in Rhode Island real estate investing. Unlike most states where lead paint disclosure is a one-time checkbox at closing, Rhode Island requires active, recurring compliance for every pre-1978 rental unit. You must obtain a Certificate of Lead Conformance every two years or at each tenant turnover — whichever comes first — through an EPA-certified lead inspector. The 2024/2025 rental registry update auto-cross-references CLC status against health department records, so the state knows immediately when your certificate lapses. As of October 2024, a landlord without a valid CLC cannot file evictions — your problem tenant stays, and you accumulate $125/unit/month in fines while they do. Failed inspections trigger EPA RRP-compliant remediation costing $5,000-$15,000 per unit, performed only by certified Lead Renovation Firms. A first-time EPA violation carries fines up to $37,500 per day. The guide walks through the complete CLC inspection cycle, remediation budgeting, insurance coverage requirements, and how to verify compliance status before you close on any pre-1978 property — which is virtually every triple-decker in the state.

Triple-Decker Acquisition and Financing Strategy

Rhode Island's signature asset class is permanently supply-constrained. Modern zoning prohibits new three-unit construction, demolition is rare, and every surviving triple-decker was built between 1880 and 1930. Because they're classified as residential (not commercial), owner-occupant investors can acquire them with FHA financing at 3.5% down or Fannie Mae conventional at 5% down — putting a $550,000 building within reach for $19,250-$27,500 plus closing costs. The guide covers the full acquisition mechanics: how to evaluate century-old building systems, budget for deferred maintenance on knob-and-tube wiring and cast-iron plumbing, structure your owner-occupied unit selection to maximize rental income from the other two floors, and navigate the operational reality of becoming a three-unit landlord in a building older than most investors' grandparents. It also explains why this closed asset class creates a structural advantage — new supply literally cannot enter the market to compress your rents.

Flood Insurance and Coastal Deal Underwriting

Rhode Island has 400 miles of coastline, and FEMA's Risk Rating 2.0 methodology has made flood insurance the single largest variable in coastal deal economics. Under the old zone-based pricing, you could estimate premiums from neighbors' policies. Under Risk Rating 2.0, two adjacent properties in the same flood zone can have premiums differing by $15,000/year based on foundation type, first-floor elevation relative to Base Flood Elevation, and distance to the flooding source. A Zone VE property can face premiums of $20,000-$34,000/year — on a $4,000/month gross rent property, that's $1,250/month consumed by flood insurance alone before taxes, maintenance, or debt service. The guide covers elevation certificates (the single most important document in any coastal acquisition), Community Rating System discounts (Narragansett and Westerly's Class 8 rating yields 10% off NFIP premiums), private flood alternatives through surplus lines carriers, and the South County tax rate illusion — where low mill rates mask total carrying costs once flood premiums are modeled in.

University Housing Zoning and the Orange Sticker Ordinance

Renting near Brown, RISD, Providence College, or URI sounds like guaranteed occupancy. It is — until you hit the zoning wall. Providence caps unrelated occupants at 3 per dwelling unit, full stop. Narragansett recently expanded to 5 (one per legal bedroom), but attached a penalty structure that makes landlords personally liable for tenant behavior: the "Orange Sticker" ordinance fines landlords $500 for the first noise or disturbance offense, and on the second offense, revokes the property's rental registration for one full year. Your income goes to zero because of your tenant's house party. The guide covers occupancy verification procedures, lease structuring to shift liability, academic calendar timing (June 1 vs. September 1 lease starts), per-bedroom pricing strategies, and how to run a compliant university rental operation without triggering the enforcement mechanisms that have shut down other landlords' properties.

Newport Historic District Commission (HDC) Navigation

Approximately 40% of Newport's geographic area falls under Historic District Commission jurisdiction. Any exterior alteration visible from a public right-of-way — windows, siding, roofing, even paint color — requires a Certificate of Appropriateness before you can pull a building permit. Custom historically accurate materials (wood windows instead of vinyl, specific mortar compositions, approved composite siding profiles) add months and tens of thousands to renovation timelines. Short-term rentals are banned in Newport's residential zones unless owner-occupied. The guide covers the HDC application process, the Certificate of Appropriateness timeline, material specification requirements, the military housing opportunity (Naval Station Newport BAH rates create a rent floor), and how patient capital can exploit the regulatory complexity that scares off undercapitalized competitors.

Taxation: Conveyance Tax, Taylor Swift Tax, and Split Mill Rates

Rhode Island's tax landscape shifted dramatically in 2025-2026. The real estate conveyance tax increased 63% in October 2025 — from $2.30 to $3.75 per $500 of consideration — with a Tier 2 surcharge kicking in above $824,000 (2026 threshold). A $750,000 sale now incurs $5,625 in conveyance tax alone. The new "Taylor Swift Tax" (effective July 2026) levies $2.50 per $500 of assessed value above $1 million on non-owner-occupied residential properties left vacant more than 183 days per year. Municipal mill rates split between owner-occupied and investor-owned: in Providence, absentee investors pay $14.60 per $1,000 while owner-occupants pay $8.40. The guide models every tax scenario — including 1031 exchange eligibility, Rhode Island's 5.99% capital gains rate, LLC annual costs ($50 report + $400 minimum corporate tax), and how the split mill rate affects house-hack-to-full-investor transitions.

Landlord-Tenant Law and the 20-Day Security Deposit Rule

Rhode Island gives landlords 20 days to return security deposits after tenant departure — not the 30 or 60 days most states allow. Miss this deadline and the penalty is double the amount wrongfully withheld plus the tenant's attorney fees. The eviction process requires strict procedural compliance: notice periods, court filings, and specific grounds. Constructive eviction claims (where a tenant alleges uninhabitable conditions and withholds rent legally) add another dimension most out-of-state investors don't anticipate. The guide covers the complete eviction timeline, notice requirements, security deposit calculation and return procedures, self-help eviction prohibitions, and the specific documentation practices that prevent a $2,400 security deposit from becoming a $7,200 legal liability.

Foreclosure, Distressed Acquisitions, and the Porch Swing Doctrine

Rhode Island uses judicial foreclosure exclusively — meaning every foreclosure goes through the courts, typically taking 12-18 months from default to sale. Mandatory mediation adds time but creates acquisition opportunities: distressed owners often prefer negotiated sales to contested proceedings. The Porch Swing doctrine (a Rhode Island-specific legal principle) provides that a foreclosure purchaser who takes possession and makes improvements in good faith receives enhanced legal protections — effectively de-risking distressed debt acquisition for investors who understand the framework. The guide covers auction procedures, title defect risks, post-foreclosure possession timelines, and how patient capital can exploit the judicial process that impatient investors avoid.

8 Standalone Printable Tools

Beyond the guide and checklist, your download includes 8 standalone worksheets and reference cards you can print individually and use during property evaluations, closings, and ongoing operations: a fillable Due Diligence Worksheet expanding the guide's go/no-go checklist into a multi-page form with fields for every property-specific variable; a Lead Paint Compliance Reference Card with the complete CLC inspection cycle, cost ranges, and penalty schedule; a Flood Insurance Analysis Worksheet with FEMA zone premium tables, Risk Rating 2.0 variables, and a fillable DSCR impact calculator; a Tax Quick Reference covering municipal split rates, conveyance tax tiers, and the Taylor Swift Tax threshold; a Landlord-Tenant Quick Reference with the 20-day deposit deadline, eviction timeline, and notice requirements; a Closing Cost Estimator with fillable fields for every acquisition cost; an Investor Archetype Selection Guide matching your capital and strategy to the right chapters; and an Exit Cost Calculator with conveyance tax tables and a fillable exit model.

Who This Guide Is For

This guide is for real estate investors targeting Rhode Island markets who:

- Are analyzing a Rhode Island property and need to verify whether the deal actually works once you account for lead paint compliance costs, actual flood insurance premiums under Risk Rating 2.0, split mill rates for investors, and the 63% conveyance tax increase — not the generic underwriting assumptions that work in states without recurring CLC requirements

- Are under contract on a pre-1978 triple-decker and need to understand the CLC inspection cycle, remediation costs if units fail, rental registry cross-referencing, and why a lapsed certificate now blocks eviction filings — before discovering it on your first tenant dispute

- Plan to invest in South County coastal properties and need to model flood insurance under Risk Rating 2.0, verify whether the municipality's CRS rating provides a premium discount, and determine if the "Taylor Swift Tax" applies to your property's vacancy pattern

- Are targeting university-area rentals near Brown, RISD, or URI and need to verify occupancy limits, understand the Orange Sticker ordinance's landlord penalty structure, and structure leases that comply with municipal zoning without leaving rent on the table

- Are considering Newport properties and need to determine whether the parcel falls under HDC jurisdiction, what a Certificate of Appropriateness requires, why STRs are banned in residential zones, and how military BAH rates create a guaranteed rent floor

- Want every Rhode Island-specific regulation, tax calculation, and due diligence requirement in one reference — instead of assembling it from the rental registry, FEMA flood maps, municipal zoning codes, and forum threads written by investors who already made the mistakes you're trying to avoid

Why Not Free Tools and Forums?

Free information on Rhode Island real estate investing exists across a handful of sources. Here's what it actually delivers:

- BiggerPockets forums have almost no dedicated Rhode Island content. When the state is discussed, it is overwhelmingly by investors who have already purchased a property and are panicking about lead paint fines, flood insurance quotes that came back three times higher than expected, or the rental registry notification they just received. There is no organized, current Rhode Island investing resource on the platform — just scattered emergency posts from people learning expensive lessons in real time.

- Rhode Island's Rental Registry tells you whether a property is currently registered and whether the CLC is on file. It doesn't explain the 2-year renewal cycle, the $5,000-$15,000 remediation cost if a unit fails, the October 2024 eviction-blocking rule for non-compliant properties, or how to budget CLC compliance into your acquisition underwriting. You get a green or red indicator without the operational framework to act on it.

- FEMA's flood map viewer shows you the zone designation. It doesn't calculate your actual premium under Risk Rating 2.0 (which depends on property-specific elevation, foundation type, and distance to flooding source), doesn't explain CRS discounts, doesn't compare NFIP vs. private carrier options, and doesn't model the premium's impact on your DSCR. You get a zone letter without the financial analysis that determines whether the deal survives.

- Rhode Island REIA meetings provide networking and anecdotal experience from local investors. They don't provide structured due diligence frameworks, tax modeling across the 2025-2026 legislative changes, or systematic compliance procedures you can apply to every deal. The value is real but episodic — you get one investor's experience with one property, not a complete system.

- National investing courses ($997 to $5,000+) teach cap rate, DSCR, and 1031 mechanics that apply everywhere. They don't mention Rhode Island's recurring CLC requirement, the rental registry cross-reference, Risk Rating 2.0's property-specific flood premiums, Providence's 3-person occupancy limit, the Orange Sticker ordinance, Newport's HDC process, the 20-day security deposit deadline, the Taylor Swift Tax, or the Porch Swing doctrine. Applying national frameworks to Rhode Island's regulatory density is how investors discover five-figure compliance costs on their first deal.

This guide fills the Rhode Island-specific gap — the space between knowing how to analyze a rental property in general and knowing how to underwrite one in a state where recurring lead paint inspections, property-specific flood premiums, university occupancy caps, historic district commissions, split investor mill rates, a 20-day deposit deadline, and a 63% conveyance tax increase can each independently turn a profitable deal into a losing one. It's the analysis that would take a Rhode Island real estate attorney, a lead paint compliance consultant, a FEMA flood specialist, and a local tax advisor to assemble — structured as a reference you own permanently.

— Less Than One Lapsed CLC Fine

A single lapsed Certificate of Lead Conformance costs $125/unit/month in rental registry fines — and blocks you from filing evictions until compliance is restored. One unmodeled flood insurance premium of $15,000/year reduces your monthly NOI by $1,250 and can sink your DSCR below the lender's threshold. A security deposit returned on day 21 instead of day 20 triggers double damages plus the tenant's attorney fees. A conveyance tax you modeled at the old $2.30 rate instead of the new $3.75 rate understates your exit costs by 63%.

This guide doesn't replace your Rhode Island closing attorney or your CPA. But it gives you the lead paint compliance framework, flood insurance modeling methodology, university zoning map, tax calculation system, and landlord-tenant deadline calendar that ensure you identify every Rhode Island-specific risk before you're contractually committed — instead of discovering them on your first rental registry notification, your first flood insurance bill, or your first security deposit lawsuit.

If it catches a single lead paint compliance gap, prevents a single flood insurance miscalculation, or saves you from a security deposit penalty, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't sharpen your underwriting and protect your capital in Rhode Island's regulatory environment, you pay nothing.

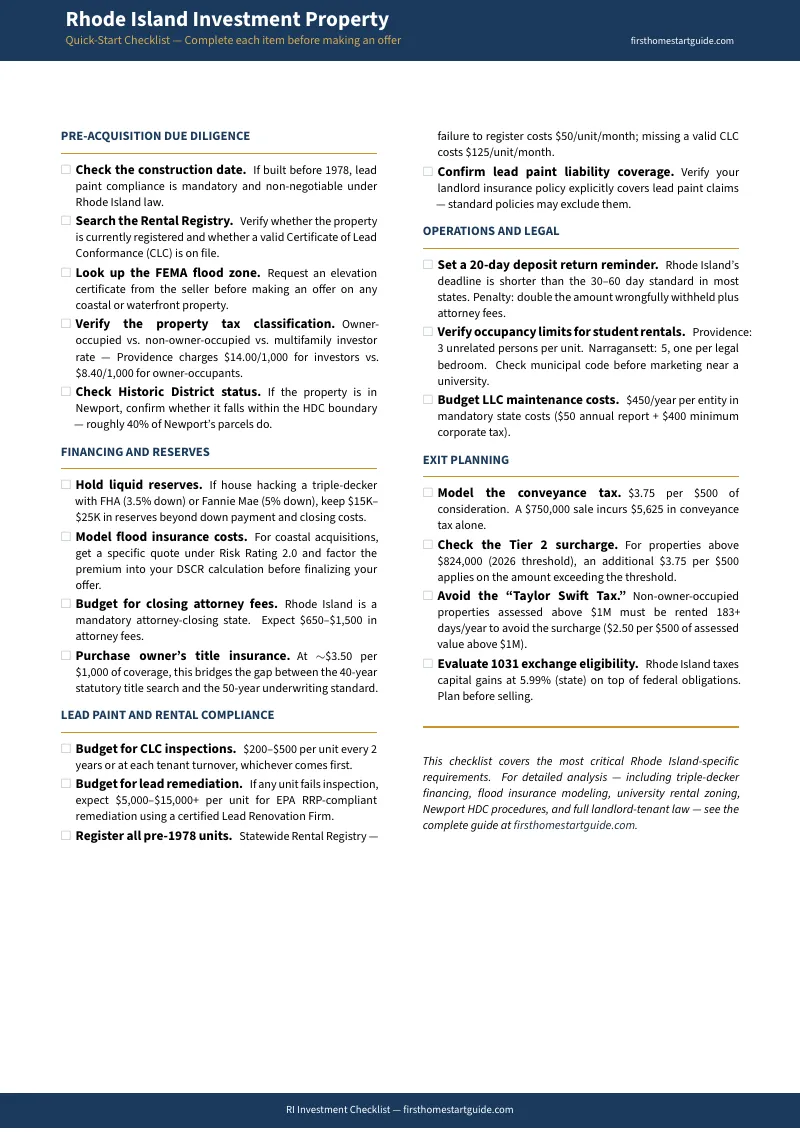

Download the free Rhode Island Quick-Start Checklist to see the 20-item due diligence framework covering pre-acquisition research, financing reserves, lead paint and rental compliance, operations and legal requirements, and exit planning. When you're ready for the full 15-chapter guide, 8 standalone printable tools, and the complete lead paint compliance system, flood insurance analysis, university zoning guide, and tax modeling, the complete toolkit is here.

The deal looks good on the spreadsheet. This guide tells you whether Rhode Island agrees.