You Found the House. But the THDA Assistance Isn't a Grant, the Sinkhole Insurance Won't Pay Unless the Government Condemns the Building, and the Title Insurance Custom Changes Depending on Which Side of the State You're On.

You found a three-bedroom in Murfreesboro projecting $2,200/month PITI. Or a starter home in Clarksville near Fort Campbell where your VA loan covers 100% of the purchase. Or a craftsman in East Knoxville where the listing agent says the foundation cracks are "normal settling" and the inspector didn't mention the word karst. You ran the numbers. You got pre-approved. You're ready to make an offer.

Then Tennessee happens. Your lender tells you the THDA Great Choice Plus down payment assistance is "basically free money" — but it's actually a $6,000 second mortgage at 0% interest that must be repaid in full if you sell, refinance, or transfer title before 30 years. Since the average first-time buyer moves within seven to ten years, that $6,000 comes out of your equity at closing. You buy in Knox County and your standard homeowners policy covers "Catastrophic Ground Collapse" — which sounds reassuring until you learn that Tennessee law requires four co-dependent criteria including a government condemnation order before the policy pays a single dollar. Your foundation sags, your walls crack, your floors slope — but because the home isn't condemned, your claim is denied. You close on a home in Johnson City and assume the seller paid for your owner's title insurance, the way it works in Nashville. But in East Tennessee, that custom is fully negotiable — and the seller's agent already told your agent that the buyer is covering title. That's $1,500 to $2,500 you didn't budget for.

Here's what no single free resource explains: Tennessee layers a state-funded down payment assistance program that is widely misunderstood as a grant against a property tax system using a unique 25% assessment ratio that makes county-to-county comparisons meaningless without conversion, against karst limestone geology covering 60% of East Tennessee that can destroy a foundation at remediation costs of $30,000 to $200,000, against an insurance framework where standard sinkhole coverage requires government condemnation to trigger, against closing customs that shift from attorney-directed to title-company-directed depending on which region you're buying in, against HOA fees in Nashville's suburban ring that reduce your purchasing power by $35,000 for every $200/month in dues, against a military buyer market in Clarksville where the VA "house hacking" exit strategy fails because monthly PITI exceeds local rents and 24-month equity is too thin to cover transaction costs. Each of these has cost real first-time buyers five figures because the information existed — scattered across THDA program sheets, county tax assessor websites, geological survey maps, insurance statute annotations, and Reddit threads from buyers who learned the hard way — but nobody had assembled it into a single decision system calibrated to how Tennessee actually works.

The Tennessee First-Time Home Buyer Guide is a Tennessee Risk Navigation System — not a motivational overview of the Volunteer State lifestyle, but a structured reference that maps every Tennessee-specific program, tax structure, geological hazard, insurance gap, and regional closing custom into a process you work through before your earnest money is at risk. It replaces months of cross-referencing THDA program matrices, county assessment ratios, karst zone maps, insurance policy exclusions, and forum posts with a single guide that tells you exactly what to verify, exactly what the numbers should look like, and exactly where deals go wrong in this state.

What's Inside the Tennessee Risk Navigation System

A comprehensive guide, a quick-start checklist, and 8 standalone printable tools (10 PDFs) — covering every stage from pre-approval through post-closing, built specifically for the programs, tax structures, geological risks, and regional customs that make Tennessee different from every other state:

THDA Down Payment Assistance Decision Framework

Tennessee's primary assistance program — the THDA Great Choice Home Loan with Great Choice Plus — is genuinely helpful but widely misunderstood. The guide breaks down the two DPA structures side by side: the $6,000 deferred option (0% interest, no monthly payments, forgiven at 30 years — but repaid in full if you sell, refinance, or transfer title before that) versus the amortizing option (up to $15,000 or 5% of purchase price, but fully repayable over 30 years at your mortgage rate, permanently increasing your monthly obligations and lowering your qualifying purchase price). It covers the income limits by county, the $400,000 purchase price cap, the mandatory homebuyer education course, the Homeownership for Heroes program (0.50% rate reduction for military, first responders, and K-12 teachers — with the first-time buyer restriction waived statewide), the Freddie Mac HFA Advantage Plus for conventional buyers, and the Mortgage Credit Certificate that gives you 20-30% of your annual mortgage interest back as a dollar-for-dollar federal tax credit. Plus the federal recapture tax — a levy most lenders forget to explain that can apply if you sell within nine years, make a profit, and your income exceeds federal limits.

Karst Geology and Sinkhole Risk Assessment

Approximately 60% of Knox County and much of the Valley and Ridge province of East Tennessee sits on karst topography — soluble limestone bedrock that dissolves over time, creating underground voids that cause the surface to collapse. The guide teaches you to identify the structural red flags (stair-step brick cracking, gaps between walls and ceilings, sloping floors, doors and windows that suddenly stick) and property-level warning signs (circular yard depressions, tilting fence posts, water pooling in unexpected areas, well water that turns cloudy after rain). It covers the cost of professional geotechnical evaluations ($2,500 to $4,500 for standard, $5,000 to $15,000 for GPR or ERI) and explains the critical difference between the two insurance frameworks: "Catastrophic Ground Collapse" (included in standard policies but requires four co-dependent criteria including government condemnation to pay) versus the "Sinkhole Loss Endorsement" (optional, must be requested separately, covers gradual foundation damage without condemnation). If you're buying in East or Middle Tennessee and you don't understand this distinction, you're carrying a risk you cannot recover from with your current insurance.

Tennessee Property Tax Mechanics

Tennessee's property tax system is unlike any other state. All residential property is assessed at 25% of its appraised market value — meaning a $350,000 home has an assessed value of $87,500. County tax rates are expressed per $100 of assessed value, so a rate of $2.29 per $100 assessed (Rutherford County) means $2,004/year — roughly $167/month. The guide includes county-by-county rate comparisons for the major markets, explains how reappraisal cycles work (every 4-6 years depending on county), and covers the equalization appeal process. It also clarifies that Tennessee has NO homestead property tax exemption for general homeowners — the "homestead exemption" protects equity from creditors in bankruptcy, not from taxes. Property tax relief programs exist only for seniors 65+, disabled homeowners, and disabled veterans.

Regional Closing Customs: Middle vs. East Tennessee

Tennessee is a "title state" where closings can be handled by either a title company or a licensed real estate attorney. But the customs governing who pays for what shift dramatically between regions. In Middle Tennessee (Nashville metro), sellers typically pay for the owner's title insurance policy. In East Tennessee (Knoxville, Chattanooga, the Tri-Cities), that custom is fluid and fully negotiable — and in competitive markets, buyers routinely absorb title insurance costs of $1,500 to $2,500 to make their offers more attractive. The guide covers the closing attorney vs. title company decision (comparable fees, but attorneys can provide legal advice and draft custom addenda — title agents cannot), the realty transfer tax ($0.37 per $100 of purchase price, typically paid by the buyer), the mortgage indebtedness tax ($0.115 per $100 of loan amount, first $2,000 exempt), and the county recording fees.

Nashville Metro Bidding War Playbook

Nashville's suburban ring — Rutherford, Wilson, Sumner, and outer Maury counties — is where most first-time buyers end up after being priced out of Davidson County proper. The guide covers how to obtain a fully underwritten pre-approval commitment (not just a standard pre-approval letter) to match cash-offer speed, how to structure escalation clauses with increment caps to stay competitive without overpaying, and how to shorten your inspection contingency for speed while keeping the right to walk away from major structural or geological issues. It includes a sub-market comparison table covering Nashville proper, Murfreesboro/Smyrna, Mt. Juliet/Lebanon, and Franklin/Brentwood — with estimated entry-level prices, typical property tax escrow, HOA ranges, and the specific pain point for each sub-market.

HOA Impact Analysis

In Nashville's newer suburban subdivisions, HOA membership is nearly universal. Lenders count HOA dues dollar-for-dollar against your debt-to-income ratio. A $200/month HOA reduces your purchasing power by approximately $35,000. The guide explains why a lower-priced home with high HOA fees can actually be harder to qualify for than a more expensive home without one, how to evaluate HOA reserve health (funding below 25% of anticipated capital expenditures signals special assessment risk of $5,000 to $15,000), and the specific fee ranges across property types — basic subdivision ($50-$150/month), master-planned community ($250-$400/month), and townhome/condo in Davidson County ($300-$500/month for exterior maintenance, roofing, and structural insurance).

Clarksville Military Buyer Analysis

Fort Campbell's 101st Airborne Division makes Clarksville one of the most military-dependent real estate markets in the country. The guide provides an honest financial analysis of the VA loan "house hacking" strategy that dominates military personal finance forums — and explains why it frequently fails. With 0% down in a high-rate environment, monthly PITI often exceeds local market rent. 10% property management fees, elevated tenant turnover, and transient wear-and-tear erase paper profits. And sellers who move after 24 months on PCS orders rarely have enough equity to cover the 5-6% transaction costs, forcing them to bring cash to the closing table. The guide includes the VA loan parameters, the Homeownership for Heroes 0.50% rate discount, and a realistic rent-vs-buy model for Clarksville's price point.

Memphis Market and Institutional Investor Landscape

Memphis is affordable on paper — entry-level homes in the $150,000 to $250,000 range — but first-time buyers face competition from institutional investors who purchased over 7,000 single-family homes in Shelby County in a recent two-year period. These all-cash, no-contingency offers lock FHA buyers out of the entry-level bracket. The guide covers the FHA financing strategy for Memphis (3.5% down, minimum property standards that disqualify older homes with safety issues), credit and DTI challenges specific to the Memphis market, and the older housing stock that often fails FHA appraisal requirements.

Rural Tennessee: USDA, Septic, Well Water, and Environmental Risks

Outside the major metros, USDA 100% financing makes homeownership accessible with zero down payment. But rural properties introduce due diligence requirements that urban buyers never encounter: septic system permit verification (a four-bedroom listing with a two-bedroom septic permit will fail under load), private well-water testing for bacterial and chemical contamination (especially in karst regions where surface runoff penetrates aquifers), fire department proximity and its impact on insurance premiums, and broadband availability for remote workers. The guide covers USDA eligibility zones, income limits, and property condition requirements alongside the rural-specific inspection protocol.

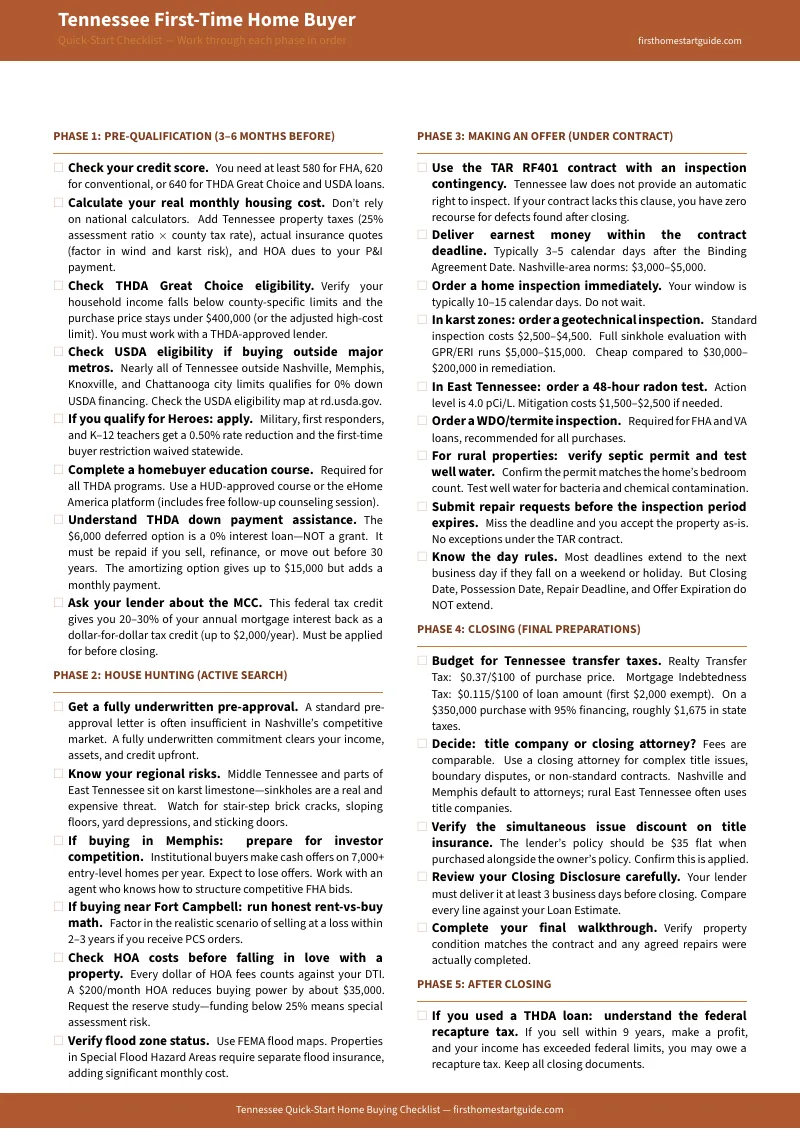

29-Item Quick-Start Checklist

A structured checklist covering five phases — pre-qualification, house hunting, making an offer, closing, and after closing — with the specific Tennessee deadlines, program requirements, and verification steps you need at each stage. Print it and check items off as you go.

8 Standalone Printable Tools

Print-ready reference cards and worksheets you can bring to lender meetings, property showings, inspections, and closing appointments:

- Closing Cost Calculator Worksheet — Line-by-line fillable worksheet covering Tennessee transfer taxes, title insurance, lender fees, prepaid items, inspections, THDA DPA credits, and seller concessions

- Inspection Checklist — Standard inspection items plus Tennessee-specific checks for karst/sinkhole indicators, radon, WDO/termite, septic, well water, and flood zones

- THDA Program Comparison Card — Side-by-side reference for the deferred vs. amortizing DPA options, Heroes program, Mortgage Credit Certificate, and eligibility requirements

- County Property Tax Reference Card — The 25% assessment ratio formula, worked example, county-by-county rate table for 10 major markets, and the homestead exemption misconception

- Nashville Sub-Market Comparison — Entry-level prices, property tax escrow, HOA ranges, and primary challenges across six Nashville metro sub-markets, plus bidding war quick reference

- Karst Risk Assessment Checklist — Structural red flags, yard indicators, geotechnical evaluation options, and a five-step action plan for evaluating sinkhole risk

- Sinkhole Insurance Verification Card — Side-by-side comparison of Catastrophic Ground Collapse (standard) vs. Sinkhole Loss Endorsement (optional), with action steps and TCA § 56-7-130 reference

- Regional Closing Customs Quick Reference — Title company vs. closing attorney comparison, Middle vs. East Tennessee title insurance customs, transfer tax rates, and recording fees

Who This Guide Is For

This guide is for first-time home buyers in Tennessee who:

- Are buying their first home anywhere in Tennessee and need to understand how THDA down payment assistance actually works — including the repayment conditions that program marketing materials tend to gloss over, the difference between the $6,000 deferred option and the $15,000 amortizing option, and whether the Mortgage Credit Certificate makes sense for their tax situation

- Are looking at properties in East or Middle Tennessee and need to understand karst geology — the structural red flags that indicate active sinkhole risk, the cost of professional geotechnical evaluation, and why standard homeowners insurance will deny your claim unless the government literally condemns your building

- Are buying in Nashville's competitive suburbs and need bidding war strategies — fully underwritten pre-approvals, escalation clauses, shortened inspection contingencies — that keep them competitive without taking on catastrophic risk

- Are relocating from another state and need a clear explanation of Tennessee's 25% assessment ratio, county-by-county property tax rates, the realty transfer tax, and the mortgage indebtedness tax — so their closing cost estimate reflects reality, not a national calculator's guess

- Are active-duty military or veterans buying near Fort Campbell and want an honest financial model for the Clarksville market — not the optimistic "house hack" narrative, but a realistic analysis of whether buying with 0% down makes sense when PCS orders could arrive in 24 months

- Want every Tennessee-specific program, tax, risk, and regional closing custom in one reference — instead of assembling it from THDA program sheets, county assessor websites, geological survey maps, Reddit threads, and agent blogs designed to generate leads, not explain risks

Why Not Free Tools and Forums?

Free information on buying a home in Tennessee exists. Here's what it actually delivers:

- THDA's website publishes program guidelines and income limit tables. It doesn't explain why the $6,000 deferred option is almost always repaid before forgiveness (because the average first-time buyer moves within seven to ten years), doesn't compare the deferred vs. amortizing options with specific DTI impact calculations, and doesn't cover the federal recapture tax that can apply if you sell within nine years. You get the program specs without the decision framework.

- Zillow and Realtor.com show estimated monthly payments using national-average tax rates. Tennessee's 25% assessment ratio and county-specific rates make those estimates unreliable. And no listing platform shows HOA dues, sinkhole risk zones, or the title insurance customs that vary by region. You get a number that looks affordable and may not be.

- Real estate agent blogs highlight no state income tax, affordable entry prices, and Nashville's growth story. They minimize HOA stacking in suburban subdivisions, gloss over the karst geology that underlies 60% of Knox County, and never explain why the insurance policy you think covers sinkholes actually requires a condemnation order to pay. The content is designed to generate leads, not to identify reasons to slow down.

- Reddit threads (r/Nashville, r/Knoxville, r/memphis, r/MilitaryFinance) contain genuine buyer experiences — people sharing bidding war fatigue, THDA confusion, and sinkhole horror stories. But advice from 2023 doesn't reflect current THDA income limits, updated USDA eligibility zones, or the latest county reappraisal cycles. Sorting current from outdated takes longer than reading a guide that has already done it.

This guide fills the Tennessee-specific gap — the space between knowing how to buy a house in general and knowing how to buy one in a state where down payment assistance is a repayable loan, where karst geology can destroy a foundation you never evaluated, where your sinkhole insurance requires a condemnation order before it pays, where property taxes use a 25% assessment ratio that makes county comparisons meaningless without conversion, and where the title insurance custom flips depending on whether you're buying in Nashville or Knoxville. It's the analysis that would take a Tennessee real estate attorney, a THDA-approved lender, and a licensed geotechnical engineer to assemble — structured as a reference you own permanently.

— Less Than One Geotechnical Inspection

A standard geotechnical evaluation in East Tennessee runs $2,500 to $4,500. A full sinkhole investigation with Ground Penetrating Radar costs $5,000 to $15,000. Foundation remediation — compaction grouting and underpinning — runs $30,000 to $200,000. Choosing the wrong THDA DPA option can mean repaying $6,000 out of your equity when you sell. Missing the inspection contingency deadline in the TAR contract means accepting the property as-is with zero recourse. A $200/month HOA you didn't factor into your DTI calculation means losing $35,000 in purchasing power.

This guide doesn't replace your real estate agent or your lender. But it gives you the THDA program analysis, karst geology assessment protocol, insurance coverage verification checklist, property tax calculations, regional closing custom breakdown, and bidding war strategy that ensure you identify every Tennessee-specific risk before your earnest money is committed — instead of discovering them on your first insurance claim denial, your first property tax reappraisal, or your first foundation repair quote.

If it catches a single THDA repayment surprise, prevents a single uninsured sinkhole loss, or saves you from absorbing title insurance costs you could have negotiated, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't sharpen your decision-making and protect your investment in Tennessee's unique real estate landscape, you pay nothing.

Download the free Tennessee Quick-Start Home Buying Checklist to see the 29-item action plan covering pre-qualification, house hunting, offer strategy, closing preparation, and post-closing protection. When you're ready for the full THDA decision framework, karst geology assessment guide, regional market profiles, military buyer analysis, and closing cost calculator, the complete guide is here.

The house looks perfect on Zillow. This guide tells you whether Tennessee agrees.