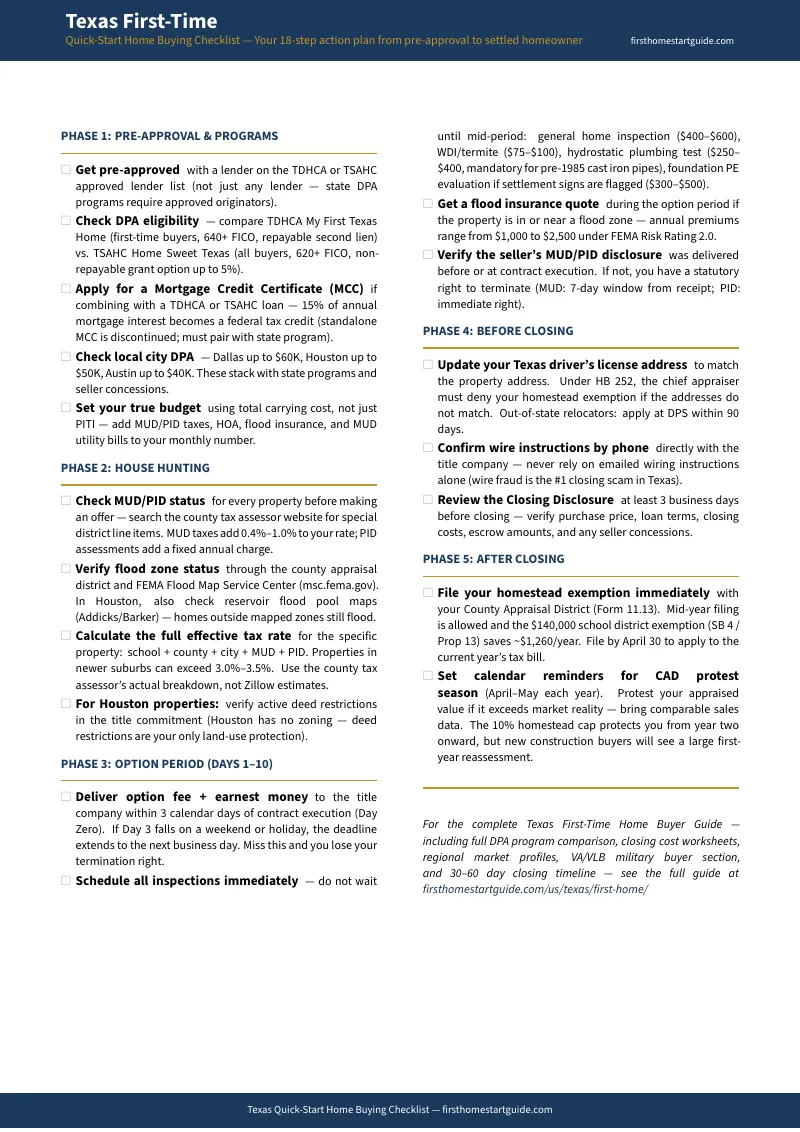

You Found the House. But the Option Fee Is Due in 72 Hours, the MUD Tax Rate Isn't on Zillow, and Your Homestead Exemption Will Be Denied If Your Driver's License Doesn't Match.

You found a three-bedroom in Katy projecting $1,950/month PITI. Or a new build in McKinney where the builder quoted you $2,100 with "low taxes." Or a townhouse in Pflugerville where the listing says "no HOA" and the commute to downtown Austin clocks 28 minutes on Google Maps at 2 PM on a Tuesday. You ran the numbers. You got pre-approved. You're ready to make an offer.

Then Texas happens. Your agent sends the TREC One to Four Family contract and you have 72 hours from execution to deliver the option fee and earnest money to the title company --- or you lose your unrestricted right to terminate. You close on the new build in McKinney and your first-year escrow payment is based on vacant land value --- then the County Appraisal District reassesses at full improved value and your monthly payment jumps $450. You file your homestead exemption and the chief appraiser denies it because the address on your Texas driver's license doesn't match the property --- you didn't know about House Bill 252's matching mandate, and now you've lost $1,260 in school district tax savings. The property in Katy sits inside a Municipal Utility District with a tax rate of 0.85% layered on top of school, county, and city taxes, plus a separate monthly MUD water bill. Your $1,950 estimate is actually $2,400.

Here's what no single free resource explains: Texas layers a uniquely structured option period with strict 72-hour delivery deadlines and a non-refundable option fee (meaning your termination right depends on getting funds to the title company before Day 3, not Day 4), against a property tax system that has no state income tax but effective rates of 1.6% to 3.5% depending on special district overlays, against a homestead exemption worth $140,000 off your school district assessment that requires your driver's license address to match exactly or the application is denied by statute, against two separate state DPA agencies (TDHCA and TSAHC) that each offer different assistance structures --- repayable second liens, forgivable second liens, and outright grants --- with different eligibility rules and different MCC compatibility, against foundation and plumbing risks driven by expansive clay soils that can cost $15,000 to $35,000 to repair if you skip the right inspections during the option period. Each of these has cost real first-time buyers five figures because the information existed --- scattered across TREC forms, CAD websites, TDHCA program matrices, Reddit threads, and real estate agent blogs designed to close deals, not explain risks --- but nobody had assembled it into a single decision system calibrated to how Texas actually works.

The Texas First-Time Home Buyer Guide is a Texas Transaction Control System --- not a motivational overview of the Lone Star lifestyle, but a structured reference that maps every Texas-specific deadline, tax trap, assistance program, and inspection requirement into a process you work through before your option period expires and your earnest money is at risk. It replaces months of cross-referencing TREC contract paragraphs, CAD protest procedures, TDHCA vs. TSAHC program matrices, MUD boundary lookups, and forum posts with a single guide that tells you exactly what to verify, exactly what the numbers should look like, and exactly where deals go wrong in this state.

What's Inside the Texas Transaction Control System

A comprehensive guide, a quick-start checklist, and 8 standalone printable tools (10 PDFs) --- covering every stage from pre-approval through post-closing tax filing, built specifically for the transaction mechanics, tax structures, and assistance programs that make Texas different from every other state:

The TREC Contract and Option Period Blueprint

Texas is a title company state where agents use TREC promulgated forms --- not attorney-drafted contracts. The option period gives you an unrestricted right to terminate for any reason, but only if the option fee reaches the title company within three calendar days of execution. The guide walks through Day Zero counting (the effective date is Day Zero, not Day One), the weekend and holiday extension rule, how combined option fee and earnest money payments are allocated under Paragraph 5A (option fee applied first, shortfall hits earnest money), the consequences of late delivery under Paragraph 5D (you lose the termination right permanently), and the title commitment review window under Paragraphs 6B and 6D. If you're buying in Texas for the first time --- especially from out of state --- this chapter alone prevents the single most common contractual mistake buyers make: missing the option fee delivery deadline and being locked into a binding contract with no exit.

Property Tax Mechanics and the New Construction Escrow Trap

Texas has no state income tax, but effective property tax rates of 1.6% to 2.5% in established neighborhoods --- and 3.0% to 3.5% in newer suburbs with MUD and PID overlays. The guide breaks down how County Appraisal Districts assess value annually based on January 1 condition, why new construction buyers see escrow shortages of $300 to $600 per month when the CAD reassesses from vacant land to fully improved value, how to calculate the full effective tax rate for any property using the county tax assessor's actual breakdown instead of Zillow estimates, the annual protest process (file by May 15 or 30 days after notice, whichever is later), and why Texas's lack of a state transfer tax saves several thousand dollars at closing compared to New York, Connecticut, or Pennsylvania. If you're relocating from California, the comparison to Proposition 13's locked-in assessments versus Texas's annual market-value reassessments is here.

The $140,000 Homestead Exemption and the Driver's License Trap

The Residence Homestead Exemption is the most valuable tax tool available to Texas homeowners. Through Proposition 4 (2023) and Senate Bill 4 / Proposition 13 (2025), the mandatory school district exemption has grown from $40,000 to $140,000 --- saving approximately $1,260 per year on a $350,000 home. Seniors and disabled homeowners get an additional $10,000, for a combined $150,000 exemption with a permanent tax freeze. The guide details how to file Form 11.13, the mid-year filing rule that lets you claim the exemption in the same year you buy (without waiting until the following January), the 10% annual appraisal cap that starts protecting you in year two, and the HB 252 matching mandate that requires your Texas driver's license address to match the property address exactly --- if it doesn't, the chief appraiser must deny your application by law. Out-of-state relocators must apply for a Texas license in person at DPS within 90 days.

TDHCA vs. TSAHC: Down Payment Assistance Decision Framework

Texas runs two separate state agencies that fund down payment assistance, and choosing the wrong one can cost you thousands. TDHCA's My First Texas Home requires first-time buyer status and pairs with a Mortgage Credit Certificate (MCC) that converts 15% of your annual mortgage interest into a federal tax credit --- effectively lowering your debt-to-income ratio and helping you qualify for a larger purchase price. TDHCA's My Choice Texas Home drops the first-time requirement but cannot pair with an MCC. TSAHC's Home Sweet Texas and Homes for Texas Heroes programs offer a non-repayable grant of up to 5% of the loan amount or a deferred forgivable second lien --- forgiven after 36 months with no refinancing. The guide maps every program's credit score requirements (620 for government loans, 640 for conventional HFA), income limits, purchase price caps, and the specific scenarios where each program wins: TSAHC grants for buyers who want zero repayment obligation, TDHCA forgivable liens for buyers who plan to stay 3+ years, and the TDHCA + MCC combo for buyers who need the DTI boost to qualify. Plus city-level DPA programs that stack on top: Dallas up to $60K, Houston up to $50K, Austin up to $40K.

MUD and PID Special District Tax Playbook

Municipal Utility Districts and Public Improvement Districts are the hidden carrying cost that blindsides first-time Texas buyers --- especially in DFW's outer-ring suburbs and Houston's master-planned communities. MUDs fund water, wastewater, and drainage infrastructure through an ad valorem property tax that adds 0.4% to 1.0% to your rate, plus a separate monthly utility bill. PIDs fund neighborhood enhancements through a fixed annual assessment that can be prepaid in full to permanently remove the lien. The guide explains how MUD tax rates start high and decline as development matures (more homes sharing the bond debt), the critical difference between MUD taxes (permanent, no prepayment) and PID assessments (prepayable, dissolved when bonds retire), the statutory disclosure requirements sellers must meet (failure triggers a 7-day MUD termination right or an immediate PID termination right), and how to look up any property's special district status using the county tax assessor's actual line items.

Foundation, Plumbing, and Structural Inspection Protocol

Large regions of Texas --- particularly DFW and Houston --- sit on expansive clay soils that swell when wet and shrink during drought. This continuous cycle cracks slab-on-grade foundations, shears under-slab sewer pipes, and creates differential settlement that warps door frames and separates brick veneer. The guide covers when to hire a licensed Professional Engineer for a Level B foundation evaluation (not a foundation repair company, which has a conflict of interest to recommend expensive pier installations), how a hydrostatic plumbing test works (inflatable test plug, fill to lowest fixture level, monitor for 15-20 minutes), why pre-1985 homes with cast iron sewer pipes have near-certain failure rates under hydrostatic testing, and the typical cost range for under-slab sewer replacement ($15,000 to $35,000). General home inspectors spot warning signs, but they are not licensed engineers --- this chapter tells you exactly when to escalate.

Flood Zones, Deed Restrictions, and Houston's No-Zoning Reality

Houston is the largest US city with no zoning laws. Land-use protection comes from private deed restrictions, not city ordinances --- and if those restrictions have expired or were never recorded, a commercial development can appear next to your home. The guide covers how to verify active deed restrictions in the title commitment during the option period, the post-Hurricane Harvey disclosure requirements under Senate Bill 339 (sellers must disclose 100-year floodplain, 500-year floodplain, reservoir flood pool, and prior flood damage), why homes outside mapped flood zones still flooded during Harvey due to reservoir overflows, and how to read FEMA flood maps alongside historical satellite data and elevation certificates. Flood insurance under FEMA Risk Rating 2.0 runs $1,000 to $2,500 annually.

VA and Military Buyer Section

San Antonio (Joint Base San Antonio) and El Paso (Fort Bliss) are two of the largest military real estate markets in Texas. The guide covers the Texas Veterans Land Board (VLB) Veterans Housing Assistance Program --- competitive fixed-rate loans up to the conforming limit with little to no down payment, a 0.5% interest rate discount for veterans with a 50%+ VA disability rating, and the 3-year primary residency requirement. For El Paso buyers, the guide includes the Texas vs. New Mexico cross-border comparison: El Paso County's property tax rate of 2.5% to 3.0% versus southern New Mexico's 0.7%, and the break-even calculation showing when the New Mexico income tax is offset by property tax savings over a 4-year stationing window.

Regional Market Profiles: DFW, Houston, Austin, San Antonio, El Paso

Every metro has different pain points. DFW: HOA + MUD double squeeze in master-planned communities, severe foundation and plumbing risks from North Texas clay soils. Houston: MUD/PID tax stacking in Katy, Cypress, and Sugar Land, no zoning, catastrophic flood risk, effective rates approaching 3.0% to 3.5%. Austin: tech-industry pricing pushing first-time buyers to Pflugerville, Kyle, and Cedar Park, California transplants surprised by annual reassessments. San Antonio: military-heavy market with VLB programs, affordable entry prices. El Paso: most affordable major metro for VA buyers, cross-border New Mexico strategy. Each profile covers the specific financial traps and inspection priorities for that region.

30-60 Day Closing Timeline and Carrying Cost Worksheet

A day-by-day timeline from accepted offer through county recording, with specific Texas deadlines mapped (option fee delivery by Day 3, inspection scheduling in Days 1-3, title commitment review window, survey ordering, HOA document delivery, closing disclosure review 3 days before closing). Plus a carrying cost worksheet that models every line item: PITI, MUD tax, PID assessment, HOA dues, MUD utility bill, flood insurance, and maintenance reserves --- so your monthly budget reflects what you'll actually pay, not what the listing agent quoted.

8 Standalone Printable Tools

Every tool is a separate PDF you can print and use independently --- at your lender's office, during the option period, or pinned to your wall during closing:

- Carrying Cost Worksheet --- fill in the numbers for any property: PITI, MUD tax, PID assessment, HOA, flood insurance, utilities, and maintenance. Includes two worked examples (Houston MUD suburb and San Antonio VA) plus closing cost estimates at three price points.

- DPA Decision Framework --- side-by-side comparison of TDHCA My First Texas Home, My Choice, TSAHC Home Sweet Texas, and Homes for Texas Heroes. Credit scores, income limits, MCC compatibility, and local municipal programs (Dallas $60K, Houston $50K, Austin $40K). Bring this to your lender meeting.

- Closing Timeline --- 30-to-45-day reference card with every phase from pre-approval through post-closing, with fillable fields for your own dates and contacts.

- Foundation & Inspection Checklist --- option period due diligence covering general inspection, PE foundation evaluation, hydrostatic plumbing test, WDI/termite, HVAC, and roof. Cost ranges and escalation triggers for each.

- MUD & PID Lookup Checklist --- step-by-step verification of special district status, with separate checklists for MUD and PID properties and a comparison table showing the key structural differences.

- Homestead Exemption Filing Guide --- 5-step filing process for the $140,000 school district exemption, including the HB 252 driver's license matching requirement, mid-year filing rules, and the 10% appraisal cap.

- Regional Market Quick Reference --- one-page fridge sheet with metro-by-metro pain points for DFW, Houston, Austin, San Antonio, and El Paso. Entry corridors, price ranges, and the specific traps to watch for in each market.

- Key Contacts & Resources --- every agency, appraisal district, and government website you need during the Texas home buying process, plus fillable fields for your own team contacts.

Who This Guide Is For

This guide is for first-time home buyers in Texas who:

- Are buying their first home anywhere in Texas and need to understand how the TREC option period works, what the 72-hour delivery deadline means for their earnest money, and how to use the termination right strategically during inspections --- before the option period expires and they're locked in

- Are relocating from another state --- especially California, New York, or Illinois --- and need a clear comparison of how Texas property taxes, annual reassessments, escrow mechanics, and the absence of a state transfer tax differ from what they're used to

- Want to claim every dollar of down payment assistance available and need to understand which program (TDHCA My First Texas Home, TDHCA My Choice, TSAHC grant, TSAHC forgivable lien) fits their credit score, income level, and buyer status --- and whether an MCC combination makes sense for their tax situation

- Are looking at properties in MUD or PID districts and need to calculate the true carrying cost --- not the estimate on Zillow --- including the special district tax overlay, the separate MUD utility bill, and the HOA fees that often stack on top in master-planned communities

- Are active-duty military, veterans, or military spouses buying near JBSA or Fort Bliss and want to understand the VLB housing program, the VA disability rate discount, BAH coverage at current entry prices, and the Texas vs. New Mexico cross-border tax strategy

- Want every Texas-specific deadline, tax calculation, inspection requirement, and assistance program in one reference --- instead of assembling it from TREC contract paragraphs, CAD websites, TDHCA program matrices, TSAHC eligibility charts, and Reddit threads that may predate the $140,000 homestead exemption or the latest MCC program changes

Why Not Free Tools and Forums?

Free information on buying a home in Texas exists. Here's what it actually delivers:

- TDHCA and TSAHC websites publish program charts and eligibility tables. They don't explain how to choose between a TDHCA repayable second lien and a TSAHC non-repayable grant when your credit score qualifies for both, don't show how an MCC combination changes your qualifying DTI, and don't cover city-level DPA programs that stack on top. You get the program specs without the decision framework that tells you which program to apply for.

- Zillow and Realtor.com show estimated monthly payments and "tax information" that omits MUD and PID line items, doesn't account for new construction escrow shortages, and reports historical tax bills that reflect the prior owner's homestead-capped valuation --- not the reassessed value you'll pay as a new buyer. You get a number that looks affordable and isn't.

- Real estate agent blogs and builder content highlight affordable entry prices, master-planned amenities, and "no state income tax." They minimize MUD tax stacking, gloss over the option fee delivery deadline, and never explain that foundation repair companies have a conflict of interest to recommend expensive pier installations instead of independent PE evaluations. The content is designed to generate leads, not to identify reasons to slow down.

- Reddit threads (r/FirstTimeHomeBuyer, r/Houston, r/Dallas, r/Austin) contain genuinely useful buyer experience reports --- people sharing escrow sticker shock, MUD tax surprises, and homestead exemption filing mistakes. But advice from 2023 doesn't reflect the $140,000 exemption, the latest TSAHC income limits, or the current MCC program structure. Sorting current from outdated takes longer than reading a guide that has already done it.

This guide fills the Texas-specific gap --- the space between knowing how to buy a house in general and knowing how to buy one in a state where the option period has a 72-hour delivery deadline, where property taxes run 1.6% to 3.5% depending on special district overlays, where a $140,000 homestead exemption requires your driver's license to match, where two state agencies offer four different DPA structures with different eligibility rules, and where expansive clay soils can destroy a foundation and sewer system you never inspected. It's the analysis that would take a Texas real estate attorney, a TDHCA-approved lender, and a licensed Professional Engineer to assemble --- structured as a reference you own permanently.

--- Less Than One Home Inspection

A single general home inspection in Texas runs $400 to $600. A hydrostatic plumbing test adds $250 to $400. A PE foundation evaluation adds $300 to $500. Missing the option fee delivery deadline can cost you your entire earnest money deposit. Filing your homestead exemption with a mismatched driver's license address costs you $1,260 per year in school district savings. Choosing the wrong DPA program can mean repaying assistance you could have received as a non-repayable grant.

This guide doesn't replace your real estate agent or your lender. But it gives you the option period timeline, property tax model, homestead filing checklist, DPA decision framework, special district lookup protocol, and inspection escalation criteria that ensure you identify every Texas-specific risk before your option period expires --- instead of discovering them on your first escrow shortage notice, your first CAD protest deadline, or your first foundation repair quote.

If it catches a single MUD tax miscalculation, prevents a single homestead exemption denial, or saves you from choosing a repayable lien over a forgivable grant, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't sharpen your decision-making and protect your earnest money in Texas's unique transaction system, you pay nothing.

Download the free Texas Quick-Start Home Buying Checklist to see the 18-step action plan covering pre-approval, house hunting, option period inspections, pre-closing preparation, and post-closing tax filing. When you're ready for the full DPA decision framework, carrying cost worksheet, regional market profiles, VA/VLB military buyer section, and closing timeline, the complete guide is here.

The house looks perfect on Zillow. This guide tells you whether Texas agrees.