The Spreadsheet Says Cash Flow. The 45-Day Clock Says Otherwise.

You found a duplex in Norfolk throwing off 7% gross yield against an E-6's $2,559 BAH ceiling. Or a townhome in Virginia Beach where the comps support a healthy DSCR at 1.25. Or a student rental near VCU where per-bedroom leasing pencils to $32,000 in gross annual rent on a $275,000 acquisition. The numbers work. The cap rate is solid. You're ready to wire earnest money.

Then you run the real numbers. The Norfolk duplex sits in an independent city where the property tax rate is $1.25 per $100 of assessed value — not the $0.83 you modeled from Henrico County data two miles away. On a $400,000 property, that's $4,800 in annual taxes instead of $3,320. Your property management company just triggered the Virginia Residential Landlord and Tenant Act because you hired a "managing agent" — even though you only own one property — and now you're subject to the 45-day security deposit return deadline, mandatory mold remediation disclosures, and tenant rights statements in six languages you didn't know existed. The Virginia Beach townhome sits in a flood zone where your Risk Rating 2.0 premium came back at $6,200 per year, not the $1,400 you estimated from legacy flood zone maps. At that insurance cost, your 1.25 DSCR just collapsed to 0.91 — and the lender won't close.

Here's what no single resource explains: Virginia layers an independent city tax system that creates 30% to 40% property tax cliffs across invisible municipal boundaries, a landlord-tenant act that automatically applies to any investor using a property manager regardless of portfolio size, a 45-day security deposit return deadline that imposes double-damages liability for administrative failures, FEMA Risk Rating 2.0 flood insurance premiums that can reach $8,000 per year in Hampton Roads once subsidized rates fully adjust, a military housing economy where BAH ceilings cap rents at government-set thresholds by rank, and an eviction notice period expanding from 5 days to 14 days effective July 2026 — into a regulatory environment that punishes investors who apply national assumptions to Virginia-specific problems. Every one of these has cost real investors five to six figures because the information existed — scattered across Virginia Tax's local rate tables, VRLTA code sections, FEMA actuarial data, DoD BAH lookup tools, and BiggerPockets threads from 2022 — but nobody had assembled it into a single underwriting system.

The Virginia Investment Property Guide is a Virginia Investor Compliance Navigator — not a motivational overview of real estate investing, but a structured due diligence framework that maps every Virginia-specific financial trap, regulatory restriction, and environmental risk into a process you work through before you wire earnest money. It replaces months of cross-referencing independent city tax rates, VRLTA code sections, FEMA Risk Rating 2.0 actuarial data, DoD BAH tables, and Virginia Beach STR permit requirements with a single reference that tells you exactly what to verify, exactly what the numbers should look like, and exactly where deals go wrong.

What's Inside the Virginia Investor Compliance Navigator

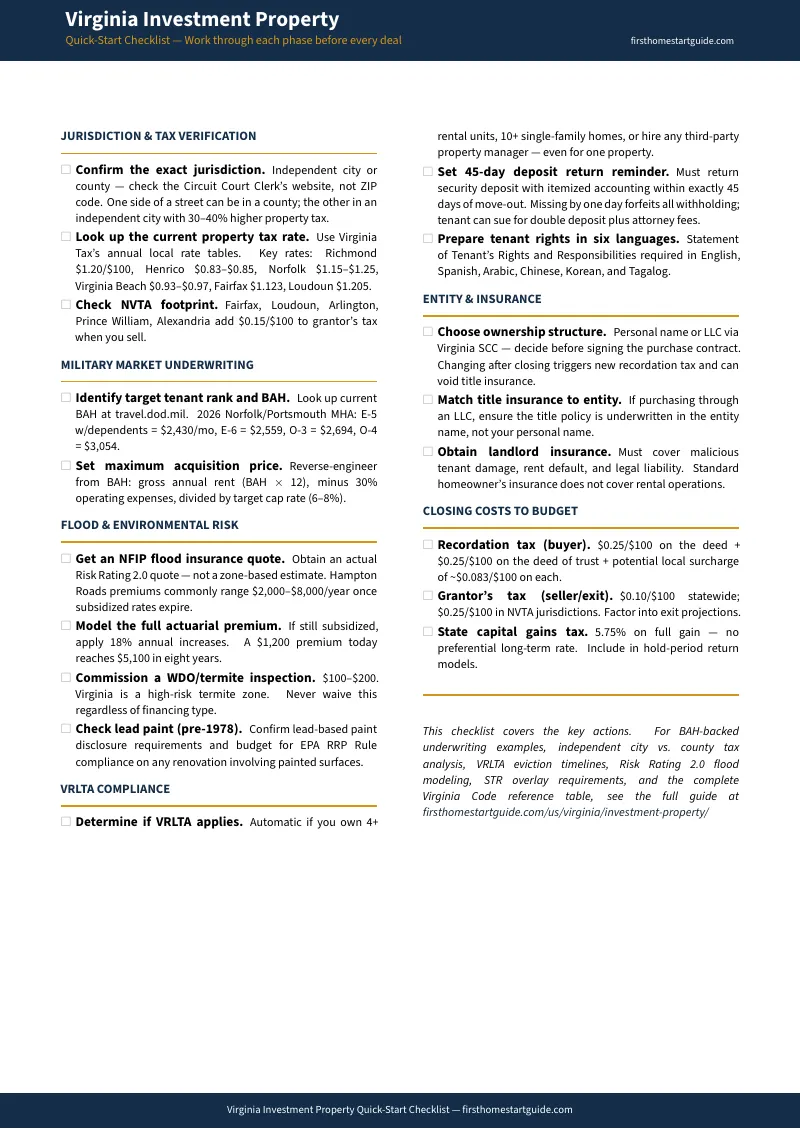

An 11-chapter guide with appendices, a quick-start checklist, and 5 standalone printable worksheets and reference cards — covering every stage from regional market selection through exit strategies, built specifically for the financial traps and regulatory complexity that make Virginia different from every other state:

Military Housing Economics and BAH Underwriting

Hampton Roads is the largest military housing market on the East Coast, and BAH — the tax-free monthly stipend from the Department of Defense — is the number that dictates your rental ceiling, not Zillow comps. The guide provides 2026 BAH rates for every relevant pay grade in the Norfolk/Portsmouth Military Housing Area, from E-1 at $2,229/month (with dependents) through O-5 at $3,318. It walks through the reverse-engineering process: pick your target rank, set gross rent at the BAH ceiling, deduct 30% operating expenses, divide by your target cap rate, and you get your maximum acquisition price. An E-5 with dependents maps to a $280,000 to $330,000 property in Norfolk or Newport News. An O-4 maps to $380,000 to $480,000 in Virginia Beach or Chesapeake's Harbour View. The guide also covers the "house hack to PCS conversion" pipeline that makes military buyers your primary acquisition competitors, and the mid-term rental strategy targeting traveling healthcare professionals and TDY personnel that circumvents the BAH ceiling by generating 30% to 50% higher gross monthly yields on furnished units near Naval Medical Center Portsmouth.

The VRLTA Minefield

Virginia is often described as "landlord-friendly" on national forums. That description conceals procedural tripwires that consistently trap out-of-state investors. The guide covers the full scope of the Virginia Residential Landlord and Tenant Act — including the "managing agent" paradox that automatically subjects any investor using a third-party property manager to the VRLTA, regardless of portfolio size. It maps the 45-day security deposit return deadline under Virginia Code section 55.1-1226, the itemized deduction requirements with $125 receipt thresholds, the double-damages liability for willful violations, and the mandatory tenant rights disclosures now required in English, Spanish, Arabic, Chinese, Korean, and Tagalog as of July 2025. It covers the complete eviction process — from the current 5-day pay-or-quit notice through redemption tender, judgment of possession, and the sheriff's 72-hour writ execution — plus the critical July 2026 change extending the nonpayment notice period from 5 days to 14 days. On a property with $2,500 monthly rent, a missed 45-day deadline on a maximum-allowable deposit can escalate into $10,000 to $15,000 in legal liability. The guide ensures you never discover this statute in a courtroom.

Independent City vs. County Property Tax Arbitrage

Virginia's constitutional structure makes its cities politically and fiscally independent from surrounding counties — a structural anomaly that creates sharp, localized property tax cliffs invisible to investors using aggregated MSA-level data. The guide maps the exact tax rates across every major investment jurisdiction: City of Richmond at $1.20 per $100 versus Henrico County at $0.83, City of Norfolk at $1.15 to $1.25 versus Virginia Beach at $0.93, City of Alexandria at $1.135 versus Fairfax County at $1.123, Goochland County at $0.53. On a $400,000 property, the annual tax difference between Richmond City and Henrico County is $1,480 — which translates to a $24,667 loss in implied asset valuation at a 6% cap rate. The guide shows you how to verify exact municipal boundaries before making an offer, and where the yield arbitrage opportunities sit across each metro area.

Flood Insurance and Environmental Risk (Hampton Roads)

Coastal Virginia represents one of the most acute intersections of environmental risk and real estate financial engineering in the country. FEMA's Risk Rating 2.0 abandoned the legacy flood zone maps that investors still rely on and replaced them with individualized actuarial pricing based on precise distance to water, flood frequency, elevation, foundation type, and structural replacement cost. More than one in five NFIP claims in South Hampton Roads occur outside designated high-risk flood zones. Under the new system, premiums in Norfolk and Virginia Beach range from $2,000 to $8,000 per year once fully adjusted — and existing restrictions limit annual increases to 18%, meaning investors are acquiring properties on a "glide path" to their true actuarial cost that hasn't arrived yet. Hampton Roads is also experiencing the highest rate of relative sea level rise on the East Coast. The guide models how an escalating flood premium curve destroys the DSCR calculation over a 10-to-30-year holding period, and identifies which sub-markets within Hampton Roads carry the least environmental exposure.

Short-Term Rental Regulations

Virginia Beach's STR regulatory framework is among the most restrictive in the country, and out-of-state investors routinely discover this after closing. The guide covers the annual zoning permit ($500 fee), structural safety inspections, million-dollar liability insurance mandates, and the off-street parking requirement of one full-size space per bedroom that eliminates most older oceanfront condominiums. It maps the two zones where STRs are permitted — the Oceanfront Resort District (Conditional Use Permits, renewed every five years) and the Sandbridge Special Service District — and explains why establishing an STR outside these zones requires petitioning 75% of neighboring property owners to create a new Overlay District. The "Home Share" exemption, transient occupancy tax obligations, and Shenandoah Valley vacation rental regulations are also covered. If your Virginia Beach investment thesis depends on STR income, this chapter tells you whether the property qualifies before you submit an offer.

Four-Zone Market Analysis

Virginia operates as four quasi-independent investment zones, each with distinct demand drivers, risk profiles, and optimal strategies. The guide dissects each one: Northern Virginia (NOVA) — the federal contractor and data center equity play where cap rates compress to 4% to 5% but vacancy is near-zero, with the commuter belt strategy pushing to Prince William, Stafford, and Spotsylvania counties for moderate cash flow. Richmond Metro — genuine cash-flow market at $385,000 median with 5% to 7% cap rates, anchored by VCU's 2,300-bed housing deficit and the city/county tax arbitrage. Hampton Roads — the BAH-driven military market with 6% to 8% cap rates but flood insurance and environmental risk as the primary yield killer. Shenandoah Valley and secondary markets — Charlottesville's UVA niche, Roanoke and Lynchburg's affordable entry points, and the vacation rental corridor along the Blue Ridge Parkway.

Financing, Entity Structuring, and Exit Strategies

Conventional, DSCR, VA loan (house hack pathway), and hard money financing compared by down payment, rate, qualification method, and Virginia-specific considerations. DSCR loan mechanics are covered in detail — the guide shows how Virginia's localized risks (flood insurance premiums, independent city tax rates) directly impact the DSCR calculation and can push a property from loan-eligible to loan-denied between the initial underwriting and the closing table. Entity structuring via Virginia LLC formation, registered agent requirements, and multi-property asset protection. Exit strategies including 1031 exchanges (Virginia fully conforms to federal rules with no state-specific surprises), seller financing under the Executory Contracts Act, and the non-judicial foreclosure timeline that gives investors rapid resolution through the deed of trust system.

Who This Guide Is For

This guide is for real estate investors targeting Virginia markets who:

- Are underwriting a Hampton Roads property and need to reverse-engineer the acquisition against actual BAH ceilings by rank — not Zillow rent estimates that ignore the military housing economy's artificial ceiling on what tenants will pay

- Are hiring a property manager for a Virginia rental and don't realize that a single managing agent triggers the full VRLTA — including the 45-day security deposit return deadline, mandatory six-language tenant disclosures, and double-damages liability for administrative violations — even if you only own one property

- Are analyzing a Virginia Beach or Norfolk property and need an actual Risk Rating 2.0 flood insurance projection — not a legacy zone-based estimate — to determine whether the deal survives the DSCR calculation at the true actuarial premium

- Are comparing properties across Virginia jurisdictions and need the exact property tax rate for each independent city and county to avoid the $1,000-to-$2,000 annual NOI error that comes from using aggregated MSA-level data

- Plan to operate short-term rentals in Virginia Beach and need to verify before closing whether the property qualifies under the Oceanfront Resort District CUP, the Sandbridge Special Service District, or the Home Share exemption — and what happens if it doesn't

- Are targeting VCU student housing in Richmond and want to understand the per-bedroom leasing economics, the 2,300-bed housing deficit, and the city-versus-county tax decision that determines whether the deal cash-flows

- Are an out-of-state investor evaluating Virginia for the first time and want every state-specific regulation, tax calculation, and due diligence requirement in one reference — instead of assembling it from Virginia Tax rate tables, VRLTA code sections, FEMA actuarial data, and Reddit threads that may have been accurate two legislative sessions ago

Why Not Free Tools and Forums?

Free information on Virginia real estate investing exists across dozens of sources. Here's what it actually delivers:

- BiggerPockets forums are where someone in a 2022 thread says Virginia is "landlord-friendly," someone in 2024 mentions the VRLTA expansions, and nobody has posted about the July 2026 extension of the pay-or-quit notice from 5 days to 14 days. Hampton Roads threads discuss BAH-based investing in general terms but don't provide the rank-by-rank underwriting tables, don't model the mid-term rental premium over long-term BAH-capped rents, and don't warn that Risk Rating 2.0 has obsoleted the flood zone maps everyone still references. You'll find genuinely useful experience reports mixed with advice predating the latest VRLTA amendments, the 14-day notice change, and FEMA's actuarial repricing. Sorting current from outdated takes longer than reading a guide that has already done it.

- Virginia Tax's local rate tables give you the property tax rate for every jurisdiction in the state. They don't explain Virginia's independent city system, don't map which side of a street sits in a county versus an independent city, don't calculate the NOI impact of selecting the wrong jurisdiction, and don't connect the tax rate to your cap rate and DSCR calculation. You get the rate without the investment analysis that determines whether the deal works at that rate.

- National investing books and courses teach cap rate, DSCR, and 1031 mechanics that apply everywhere. They don't mention the managing agent paradox that triggers the VRLTA, the 45-day security deposit deadline with double-damages liability, BAH-capped rent ceilings in military markets, Risk Rating 2.0 premium projections in Hampton Roads, the Virginia Beach STR overlay district system, or independent city tax cliffs. Applying national frameworks to Virginia-specific problems is how investors lose five figures on their first deal.

- DoD BAH lookup tools show you the monthly allowance by pay grade and location. They don't reverse-engineer the BAH ceiling into a maximum acquisition price, don't map target ranks to optimal acquisition zones within Hampton Roads, don't explain why an E-5 maps to Norfolk but an O-4 maps to Virginia Beach, and don't account for how the mid-term rental strategy circumvents the BAH ceiling entirely. You get the stipend amount without the investment framework that converts it into underwriting parameters.

This guide fills the Virginia-specific gap — the space between knowing how to analyze a rental property in general and knowing how to underwrite one in a state where BAH-capped military rents, the VRLTA's managing agent trigger, independent city tax cliffs, Risk Rating 2.0 flood premiums, and Virginia Beach's STR overlay districts can each independently turn a profitable deal into a losing one. It's the analysis that would take a Virginia real estate attorney, a flood insurance specialist, and a military housing consultant to assemble — structured as a reference you own permanently.

— Less Than One Security Deposit Mistake

A single missed 45-day security deposit deadline on a $2,500/month property exposes you to double damages plus attorney fees — $10,000 to $15,000 in legal liability from one administrative error. A property tax rate modeled at Henrico County's $0.83 instead of Richmond City's $1.20 understates your annual holding costs by $1,480 on a $400,000 property. A flood insurance premium that comes back at $6,200 instead of the $1,400 you estimated from legacy zone maps kills your DSCR loan eligibility at the closing table. An eviction timeline that takes an additional nine days after the July 2026 notice extension adds hundreds in carrying costs per nonpayment event. A Virginia Beach STR that can't meet the one-parking-space-per-bedroom requirement generates zero revenue from a strategy you already capitalized.

This guide doesn't replace your real estate attorney or your settlement agent. But it gives you the BAH underwriting tables, VRLTA compliance framework, independent city tax analysis, flood insurance projection model, and STR regulatory map that ensure you identify every Virginia-specific risk before you're contractually committed — instead of discovering them on your first security deposit dispute, your first flood insurance renewal, or your first General District Court eviction filing.

If it catches a single tax jurisdiction error you didn't model, prevents a single VRLTA compliance violation, or saves you from underestimating a single flood insurance premium, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't sharpen your underwriting and protect your capital in Virginia's regulatory environment, you pay nothing.

Download the free Virginia Quick-Start Checklist to see the due diligence framework covering jurisdiction verification, BAH underwriting, flood risk assessment, VRLTA compliance, and closing preparation. When you're ready for the full military housing economics analysis, VRLTA compliance navigator, independent city tax maps, flood insurance projections, and 11-chapter investment system, the complete guide is here.

The deal looks good on the spreadsheet. This guide tells you whether Virginia agrees.