You Can Afford the Flat. It's the Stamp Duty, MIP Premiums, Management Fees, and PSPA Penalties That Nobody Explained Clearly.

You found a two-bedroom in Tseung Kwan O at HKD 13,900 per square foot. Or a 400-square-foot unit in Tuen Mun with a walkable MTR connection and a monthly mortgage that's less than your current rent. Or maybe you've just received your HOS White Form ballot number and need to decide whether to wait for a subsidised flat or take the private market route while prices are still 25% below their 2021 peak.

Then Hong Kong's regulatory layers arrive. The Tseung Kwan O listing quotes Gross Floor Area, not Saleable Area — meaning the unit is 20% smaller than the headline number suggests. The Tuen Mun flat's management fees are HKD 6.50 per square foot because the estate has an Olympic-sized pool and three clubhouses that you'll use twice a year. And you just discovered that signing the Provisional Sale and Purchase Agreement in the secondary market is immediately legally binding — there is no cooling-off period, and backing out means forfeiting your deposit, paying double the deposit if the seller claims, and covering both agents' 1% commissions.

Here's the problem: Hong Kong combines the world's least affordable property market with a leasehold land system where every flat sits on a government lease, a stamp duty regime that changed three times in two years, a subsidised housing ballot where demand exceeds supply by 43x, MIP mortgage insurance rules that determine whether you need 10% or 30% down, Deed of Mutual Covenant clauses that can double your monthly carrying costs, and contract law that treats first-hand and second-hand purchases under entirely different legal frameworks — with different cooling-off rights, different forfeiture penalties, and different solicitor obligations. Each of these has blindsided real first-time buyers because the information existed — scattered across HKMA circulars in Chinese, LIHKG forum threads, Housing Authority PDFs, and bank mortgage brochures — but nobody had assembled it into a single system in English.

The Hong Kong First-Time Home Buyer Guide is a Hong Kong Purchase Navigation System — not a motivational overview of getting on the property ladder, but a structured decision framework that maps every stamp duty threshold, MIP eligibility rule, HOS ballot mechanic, contract obligation, and hidden cost into a process you work through before you sign anything. It replaces months of cross-referencing government portals, mortgage broker websites, and forum advice with a single reference that tells you exactly what to verify, exactly what the numbers should look like, and exactly where first-time buyers lose money in this market.

What's Inside the Hong Kong Purchase Navigation System

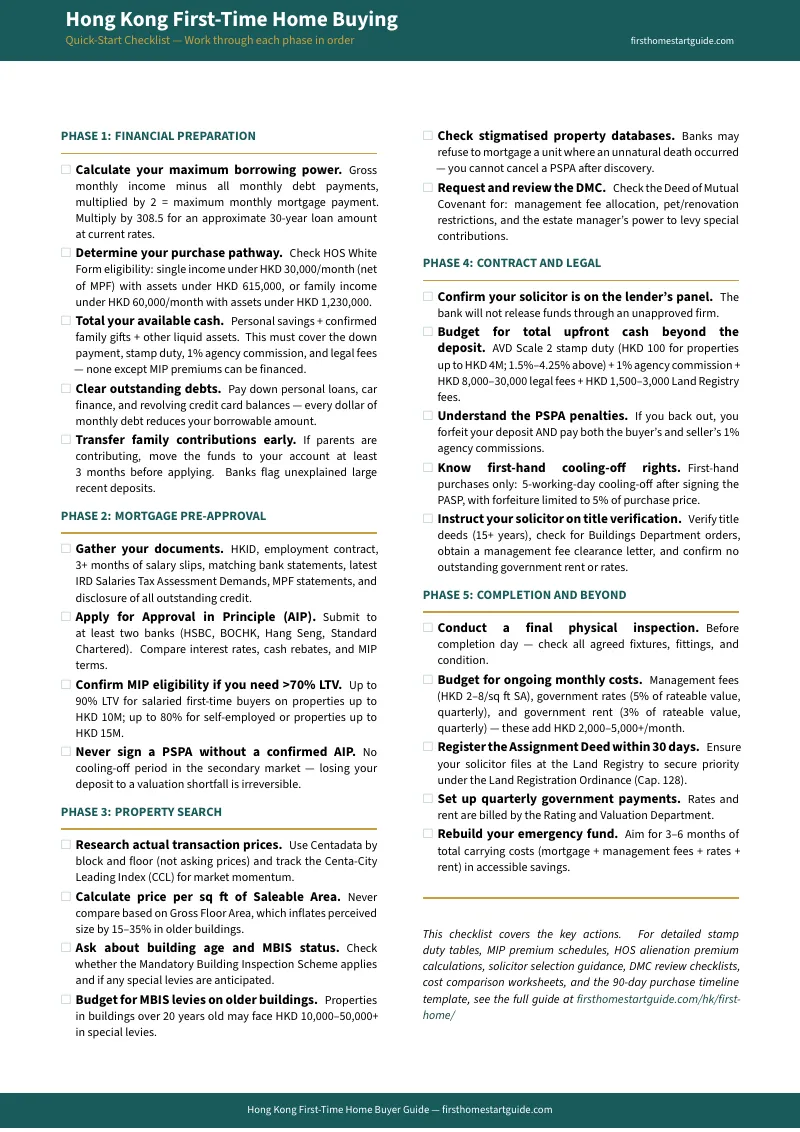

A 14-chapter guide, a standalone 20-item Quick-Start Checklist, and six standalone printable tools — covering every stage from financial readiness through completion day, built specifically for the cost traps and regulatory complexity that make buying in Hong Kong different from every other property market:

Subsidised vs Private Market Decision Framework

The most consequential decision you'll make — and the one with the least clear guidance. HOS flats sell at a 30% discount but lock you in through the alienation premium: if your flat appreciates from HKD 3 million to HKD 5 million, you owe the Housing Authority 30% of the new market value (HKD 1.5 million) just to sell on the open market. Private market flats cost more upfront but have no resale restrictions. The guide models both pathways side by side — long-term cost of ownership, resale flexibility, financing terms, and lifestyle trade-offs — so you can make this decision with actual numbers instead of guesswork.

HOS, WSM, and GSH Ballot System Decoded

The 2025/2026 ballot rules changed significantly: the Green Form to White Form quota shifted from 40:60 to 50:50, the WSM quota expanded to 7,000 with 2,000 reserved for under-40 applicants, and young families now receive an extra ballot number. The guide covers every eligibility threshold — the HKD 30,000 single-income limit, the HKD 1,230,000 family asset cap (net of MPF contributions), the Youth Scheme mechanics, and the failed-application buffer that gives you an extra ballot if you missed out in the last two exercises. If you're weighing whether to apply, you need to understand these numbers before the application window closes.

AVD Scale 2 Stamp Duty Calculation

Since the abolition of all "spicy measures" in February 2024, every residential buyer pays progressive Ad Valorem Stamp Duty under Scale 2. Properties up to HKD 4 million now attract a flat HKD 100 duty. But the progressive rates above that threshold — 1.5% to 4.25% — contain marginal relief bands with specific calculation formulas that most online calculators get wrong. The guide walks through the complete scale with worked examples at every price bracket, so you know your exact stamp duty liability before making an offer.

MIP Mortgage Insurance — How to Buy With 10% Down

The standard HKMA LTV cap is 70%, meaning you need a 30% down payment. But the Mortgage Insurance Programme lets salaried first-time buyers borrow up to 90% on properties up to HKD 10 million — if you meet the strict eligibility rules. The guide covers every MIP tier: the 80% vs 90% LTV thresholds, the HKD 9 million and HKD 12 million loan caps, the debt-servicing ratio ceiling, single vs annual premium structures (including the 15% refund if you cancel within three years), and the August 2024 rental waiver that lets you rent out your MIP property under specific conditions. The stress test was suspended in February 2024 — the guide explains what that means for your approval and why it could come back.

PSPA Contract Risks and the Cooling-Off Trap

In the secondary market, signing the Provisional Sale and Purchase Agreement is legally binding with no cooling-off period. If you change your mind, you forfeit your 3-5% deposit, owe double the deposit if the seller claims damages, and are liable for both agents' 1% commissions — potentially six figures in losses. First-hand purchases under the Residential Properties (First-hand Sales) Ordinance give you five working days to withdraw with only 5% forfeiture. The guide explains both frameworks in detail, including how to structure your PSPA terms, why your bank valuation must be confirmed before signing, and the exact sequence of deposits from PSPA through formal Agreement to completion.

The 2047 Leasehold Question — Fully Resolved

New Territories land leases expiring on 30 June 2047 used to create genuine mortgage anxiety — banks were reluctant to issue 30-year loans extending past that date. The Extension of Government Leases Ordinance (Cap. 657), passed in June 2024, automatically extends expiring general-purpose leases for 50 years with no additional land premium, maintaining only the standard 3% annual rent. The guide explains exactly what Cap. 657 covers, which lease types qualify, and why this legislative fix means the 2047 question is no longer a factor in your purchase decision.

DMC, Management Fees, and True Carrying Costs

Your monthly cost of ownership is not your mortgage payment. Management fees range from HKD 2 to HKD 8 per square foot of Saleable Area depending on estate age and facilities. Government rates add 5% of your rateable value quarterly. Government rent adds another 3%. On a typical starter flat, these add HKD 2,000 to HKD 5,000+ per month on top of your mortgage. The guide includes a Total Purchase Cost Calculator worksheet and explains how to read the DMC to identify management fee allocation formulas, pet and renovation restrictions, and the estate manager's power to levy special contributions — before you're contractually committed.

Who This Guide Is For

This guide is for first-time home buyers in Hong Kong who:

- Are deciding between the HOS ballot and the private market and need to compare both paths on actual numbers — not general advice — including how the alienation premium formula could cost you HKD 1 million+ when you eventually want to sell

- Need to understand exactly how much cash they need beyond the down payment — AVD stamp duty, 1% agency commission, legal fees, Land Registry charges, and MIP premiums — because the deposit is only the beginning

- Are about to sign a Provisional Sale and Purchase Agreement and need to understand why this is the single highest-risk moment in the entire transaction, what terms to negotiate, and why confirming your bank's valuation and your solicitor's panel status must happen before your pen touches paper

- Want 90% LTV through the Mortgage Insurance Programme but are confused by the eligibility tiers, loan caps, premium structures, and the difference between properties under and over HKD 10 million

- Are comparing listings that quote Gross Floor Area against listings that quote Saleable Area and need to understand efficiency ratios, how building age affects the gap, and how to calculate the true price per square foot across different estates

- Are concerned about the 2047 land lease expiry and need a clear explanation of Cap. 657 and why it resolves the issue — or are looking at a property with a lease type that might not qualify

- Want every Hong Kong-specific regulation, cost calculation, and due diligence step in one English-language reference — instead of assembling it from HKMA circulars, Housing Authority PDFs, forum threads, and mortgage broker websites that may reflect pre-2024 rules

Why Not Free Tools and Forums?

Free information on Hong Kong property buying exists across dozens of sources. Here's what it actually delivers:

- LIHKG and Discuss.com.hk forums contain genuinely useful experience reports from local buyers — overwhelmingly in Chinese, mixed with outdated advice about stamp duties that were abolished in 2024, MIP rules that changed in August 2024, and HOS ballot mechanics that were restructured for 2025/2026. Sorting current from outdated across a dozen threads requires fluent Cantonese reading comprehension and hours of cross-referencing against government circulars.

- HKMA and Housing Authority portals publish the official rules on LTV limits, HOS eligibility, and stamp duty rates. They don't explain how to compare an HOS flat against a private flat over a 15-year holding period, don't model the alienation premium impact on your actual resale proceeds, and don't walk you through the deposit-to-completion timeline with specific deadlines. You get the regulation without the decision framework.

- Mortgage broker comparison sites (mReferral, Starprop) compare bank interest rates and cash rebates. They don't explain why your solicitor must be on your mortgage lender's approved panel, why failing to check this before signing the PSPA can delay or kill your transaction, or how to read the DMC to identify management fee liabilities that won't show up in any mortgage calculation.

- Expat property guides provide general overviews aimed at high-net-worth luxury buyers. They rarely cover mass-market first-time buyer concerns — HOS subsidised housing, MIP high-ratio mortgages, NT district comparisons, efficiency ratios in older secondary estates, or the specific financial impact of management fees on a HKD 5-8 million starter flat.

This guide fills the English-language gap — the space between knowing you want to buy your first flat in Hong Kong and knowing exactly how to navigate a market where stamp duty rules changed twice, mortgage insurance eligibility varies by property value and employment type, contract law treats first-hand and second-hand purchases as entirely different legal transactions, and the subsidised housing system involves ballot mechanics and alienation premium calculations that most buyers only discover after they've committed. It's the analysis that would take a conveyancing solicitor, a mortgage specialist, and an HOS consultant to assemble — structured as a reference you own permanently.

— Less Than One Agency Commission Calculation Error

A single MIP eligibility miscalculation that leaves you scrambling for an extra 10-20% down payment within 14 days of signing the PSPA. A stamp duty estimate that's off by HKD 50,000 because you used the wrong AVD band. A PSPA you signed without confirming your bank's valuation, leaving you legally committed to a purchase you can't finance — with your deposit, double damages, and two agents' commissions on the line. An HOS alienation premium you didn't model, locking you into subsidised secondary market resale for a decade longer than planned.

This guide doesn't replace your conveyancing solicitor or your mortgage specialist. But it gives you the stamp duty calculation framework, MIP eligibility map, PSPA risk checklist, HOS comparison model, and district-by-district market analysis that ensure you identify every Hong Kong-specific cost and contractual risk before you're legally committed — instead of discovering them when the deposit is already non-refundable.

If it catches a single MIP tier mistake, prevents a single PSPA without confirmed bank valuation, or saves you from underestimating your carrying costs by HKD 3,000/month, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't sharpen your analysis and protect your deposit in Hong Kong's property market, you pay nothing.

Download the free Hong Kong Quick-Start Home Buying Checklist to see the 20-item action plan covering financial preparation, mortgage pre-approval, property search, contract execution, and completion. When you're ready for the full stamp duty tables, MIP premium schedules, HOS comparison worksheets, and 14-chapter buying guide, the complete guide is here.

The flat looks right for your budget. This guide tells you whether Hong Kong's regulatory system agrees.