You Earn Enough to Buy a Home in Ireland. The System Just Won't Let You Prove It.

You've done everything right. Degree, stable job, disciplined savings while paying rent that could cover a mortgage twice over. You ran the numbers: combined income times four, minus deposit, and the result puts you €40,000 short of a starter home in your own city.

So you start researching. Citizens Information explains Help to Buy in language that reads like legislation. Bank of Ireland's calculator conveniently forgets to mention what happens when you combine HTB with the First Home Scheme and your FHS cap drops from 30% to 20%. Reddit says one couple got their LTI exception approved in a week; another couple with the same income was told they needed to be Sale Agreed first — on a property they couldn't afford under standard rules. A mortgage broker wants €500 before they'll even explain the difference between the Local Authority Home Loan and a standard commercial mortgage.

Here's what no single resource explains: Ireland has four government housing schemes, each with different eligibility rules, price caps, and compatibility restrictions — and choosing the wrong combination can cost you tens of thousands of euros in missed support or lock you into service charges that compound for decades. Help to Buy gives you up to €30,000 toward your deposit, but only for new builds. The First Home Scheme covers up to 30% of the purchase price, but drops to 20% if you also use HTB — and it charges rising service fees from year six onward. The Local Authority Home Loan offers state-backed mortgages with updated 2026 price caps, but it's incompatible with the First Home Scheme entirely. And the Affordable Purchase Scheme provides council-built homes at a discount, but has means-testing rules that exclude you if your combined purchasing power exceeds 95% of market value.

The Ireland First-Time Home Buyer Guide is a Property Purchase Command Centre. Not a summary of what each scheme offers — a structured decision system that maps every scheme combination, calculates your true borrowing capacity under Central Bank rules, and walks you through the entire process from mortgage approval through key handover. It replaces months of contradictory forum threads, biased bank advice, and dense government pages with a process you can work through chapter by chapter.

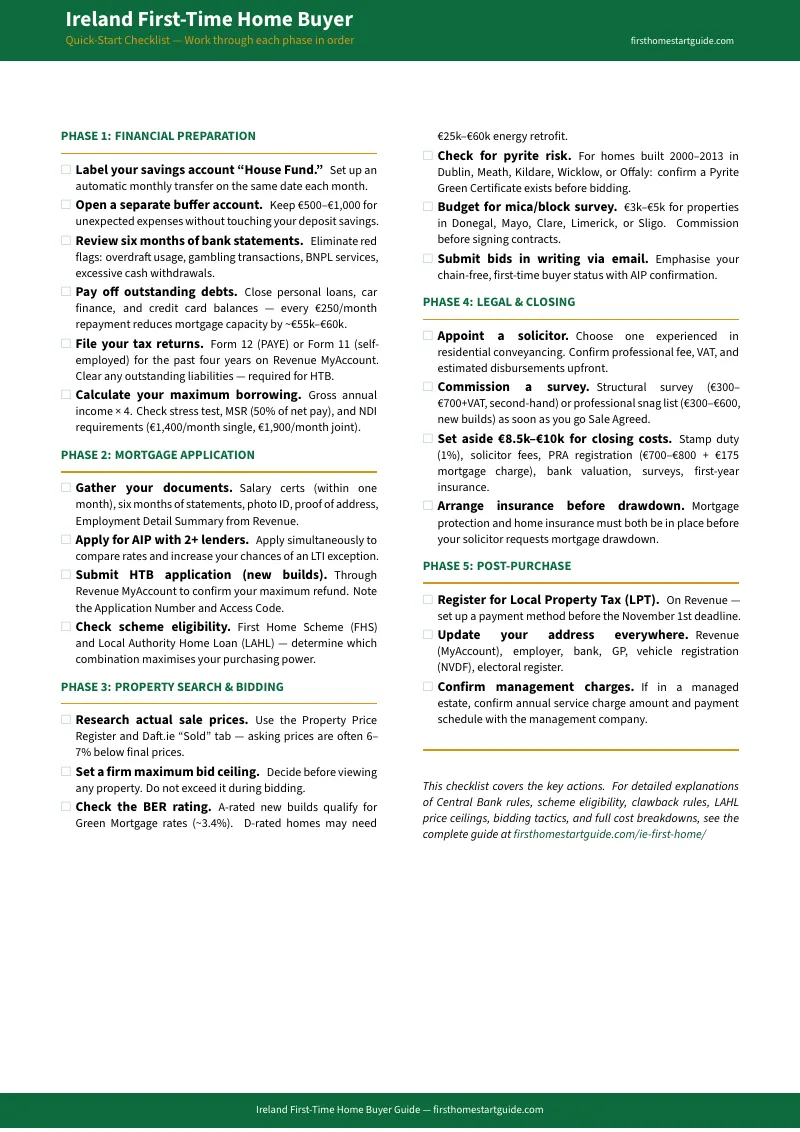

What's Inside the Property Purchase Command Centre

The complete guide plus two standalone printable worksheets — covering every stage from scheme eligibility through conveyancing completion, plus fillable tools you print, fill in, bring to mortgage appointments, and share with your solicitor:

The Four-Scheme Decision Engine

A side-by-side breakdown of Help to Buy, First Home Scheme, Local Authority Home Loan, and Affordable Purchase Scheme — with the compatibility rules that determine which combinations actually work together. The guide explains exactly why FHS and LAHL are incompatible, how stacking HTB with FHS reduces your equity support, and how to calculate which pathway yields the highest total support for your specific income and property target. This single analysis replaces hours of cross-referencing Citizens Information pages that never mention each other.

Central Bank Borrowing Capacity Worksheets

Your maximum mortgage under the 4.0x LTI rule, your deposit requirement under the 90% LTV rule, and what happens when you stress-test your repayments at 2% above your fixed rate. The worksheets calculate your Mortgage Servicing Ratio (under 50% of net pay) and Net Disposable Income (€1,400 single, €1,900 joint) so you know exactly where you stand before you sit in front of a lender. If you need an LTI exception to borrow at 4.5x, the guide explains the 15% quota system, why most lenders require you to be Sale Agreed before granting one, and how to prepare your bank statements for the six-month financial review.

Help to Buy Claim Walkthrough

The HTB refund can return up to €30,000 in Income Tax and DIRT paid over the previous four years — but only if you meet every eligibility condition. The guide walks through the Revenue MyAccount application step by step: how to verify your tax contributions, how to calculate your maximum refund, why you need a mortgage of at least 70% LTV, and the five-year primary residence requirement that triggers pro-rata clawback if you move out early. If you're choosing between a new build and a second-hand home, this chapter quantifies exactly what the HTB is worth to your total budget.

First Home Scheme Long-Term Cost Analysis

The FHS is interest-free for five years. Then the service charges begin: 1.75% annually in years 6 through 15, rising to 2.15% in years 16 through 29, and 2.85% from year 30 onward. These charges are calculated on the original cash amount, but the equity buyout is based on current market value. The guide models these costs over 10, 15, and 25 years so you can see exactly what the "free" equity support actually costs — and when buying it out makes financial sense versus letting it run.

The Full Cost of Buying — Beyond the Deposit

Stamp duty at 1% of purchase price. Solicitor fees from €1,500 plus disbursements. Land Registry fees of €400 to €800. Mortgage registration at €175. Structural survey at €300 to €700 plus VAT. Snag list for new builds at €300 to €600. Bank valuation at €150 to €300 plus VAT. The guide tallies every cost into a single total-cost worksheet so there are no surprises at the contract stage — because discovering a €3,000 shortfall after you've gone Sale Agreed is how purchases collapse.

Bidding Strategy and Estate Agent Tactics

Properties in popular areas regularly sell for 10% to 30% above asking price because estate agents deliberately under-quote to trigger bidding wars. The guide covers how to check real sale prices on the Property Price Register and Daft.ie, how to set a hard maximum before you start bidding, when to use deadline pressure on an offer, and how to leverage your first-time buyer status (no property chain) as a competitive advantage. Including what "Sale Agreed" actually means legally — and why it offers you zero protection until contracts are signed.

Mica, Pyrite, and Structural Risk Assessment

If you're buying a second-hand home in Donegal, Mayo, Clare, Sligo, Dublin, Meath, Kildare, or Offaly, you need to know about defective concrete blocks before you sign anything. Mica causes concrete to crumble; pyrite causes floors to heave. The guide covers the affected counties, the visual warning signs you can check during viewings (stair-step cracks, uneven floors, raised driveways), and the Enhanced Defective Concrete Blocks Grant Scheme that covers up to €462,000 in remediation. This chapter alone could save you from buying a home that becomes unmortgageable and uninsurable.

The Conveyancing Timeline — Solicitor to Keys

From booking deposit through contract signing to completion — mapped out over the typical 42 to 56 day timeline. The guide explains what your solicitor handles, what you need to provide, when funds are drawn down, and the critical milestones where delays commonly occur. Including the snag list process for new builds and the planning search that reveals if there's a motorway planned through your back garden.

Who This Guide Is For

This guide is for first-time home buyers in Ireland who:

- Are earning a solid dual income but find that 4.0x LTI limits their borrowing capacity below metropolitan starter home prices — and need to understand whether an LTI exception, a state scheme, or a combination of both closes the gap

- Qualify for Help to Buy but aren't sure whether a new build or second-hand home makes more financial sense once you factor in HTB, FHS eligibility, snag lists, and customization costs

- Have been told to "check Citizens Information" and found 14 separate pages, none of which explain how the four schemes interact with each other or with Central Bank lending rules

- Lost a bid and realized they went in without checking the Property Price Register, without understanding under-quoting, and without a hard maximum — and refuse to make that mistake again

- Are buying in a county with mica or pyrite risk and need to know exactly what to look for during viewings and what the remediation grant covers before they commit

- Want every cost laid out in one worksheet — deposit, stamp duty, solicitor, survey, registration, valuation — so the contract stage holds zero financial surprises

Why Not Free Resources?

Free information on buying your first home in Ireland is everywhere. Here's what it actually delivers:

- Citizens Information covers each scheme accurately and in detail. Across 14 separate pages, none of which reference each other. You get the rules for Help to Buy. You get the rules for the First Home Scheme. You never get a single page that explains they reduce each other's benefit when combined, or that FHS and LAHL are mutually exclusive. The information is correct. The connections between programs — the part that actually determines your optimal strategy — are missing entirely.

- Bank mortgage calculators (AIB, BOI, PTSB) give you a borrowing estimate in seconds. Based on their own products, at their own rates, without mentioning the competing lender down the road that's 0.3% cheaper. They'll never tell you that the Local Authority Home Loan at 4.00% fixed for 30 years might beat every commercial rate on the market for buyers under the income cap.

- Reddit threads (r/irishpersonalfinance, r/MortgageAdviceIreland) are where someone says their AIP took two weeks and someone with an identical profile says theirs took three months. You'll find genuinely helpful personal experience mixed with advice that was accurate in 2024, before the LAHL price caps were updated and the single income limit rose to €80,000. Sorting current from outdated takes longer than reading a guide that's already done it.

- Mortgage brokers offer expert guidance — for €500 to €1,500 in advisory fees, with no obligation to discuss government schemes that compete with the commercial products they earn commission on. Good brokers exist. But their incentive structure doesn't include telling you about the LAHL.

This guide fills the integration gap — the space between knowing each scheme exists and understanding which combination of schemes, lending rules, and cost structures produces the strongest possible financial position for your specific situation. It's the analysis a truly independent advisor would give you, laid out as a structured workbook you own permanently.

— Less Than One Hour of a Mortgage Broker's Time

A single mortgage broker consultation starts at €250. A conveyancing solicitor charges €1,500 minimum. Stamp duty on a €350,000 home is €3,500. The structural survey your solicitor will insist on runs €500 to €900.

This guide doesn't replace your solicitor or your mortgage application. But it gives you the scheme comparison logic, borrowing capacity worksheets, cost breakdowns, and bidding strategies that ensure you walk into every appointment, viewing, and negotiation knowing exactly where you stand — instead of learning expensive lessons in real time.

If it prevents a single overbid, identifies a single missed scheme benefit, or catches a single hidden cost before contract stage, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't make your home buying process clearer and your financial position stronger, you pay nothing.

Download the free Quick-Start Checklist to see the step-by-step action plan covering scheme eligibility, borrowing capacity, and cost planning. When you're ready for the full scheme decision engine, Central Bank worksheets, bidding strategies, and conveyancing timeline, the complete guide is here.

You've saved the deposit. Now build the strategy that gets you the keys.