You Have Been Contributing to the NHT for Years. You Still Cannot Calculate What You Will Actually Pay to Buy Your First Home in Jamaica.

You have checked the NHT website. You know you qualify for a subsidized mortgage. You may have seen the Facebook post about a buyer who found a J$15 million house in Portmore, applied for the J$12 million special NHT allocation, and then discovered at closing that the surveyor's report, attorney fees, stamp duty, NLA registration, and valuation costs added over J$1 million in cash they did not have — money the NHT does not cover and nobody told them to budget for. Or the WhatsApp thread about someone who purchased land in St. Catherine with a Common Law Title, only to learn that commercial banks will not accept it as collateral, the NHT requires statutory declarations to prove the chain of ownership, and converting to a Registered Title is a multi-year process that costs more than their deposit.

The problem is not a lack of information. The NHT publishes loan limits. JN Bank and VMBS publish mortgage calculators. Attorneys write blog posts about conveyancing. But no single resource explains how the new EFMP programme replaced joint-venture financing and what that means for your mortgage structure, how the special J$12 million NHT allocation for homes priced under J$14 million lets single buyers in Spanish Town finance 85% of the purchase through subsidized debt, how public sector workers with 10 or more years of service can stack interest rate discounts to reach 0%, or why a property with a Common Law Title instead of a Registered Title can cost you your mortgage approval and expose you to ownership disputes you cannot resolve without years of legal proceedings.

The Jamaica First-Time Home Buyer Guide is a Jamaica NHT Mortgage Navigation System — a single, structured reference that maps every NHT benefit, deposit reduction, interest rate band, transaction cost, and title risk into a step-by-step process you work through before you sign an Agreement for Sale. It replaces weeks of cross-referencing the NHT portal, bank websites, attorney blogs, and forum posts with a reference that tells you exactly what you qualify for, exactly what the numbers should look like, and exactly where Jamaica-specific transactions fall apart.

What's Inside the Jamaica NHT Mortgage Navigation System

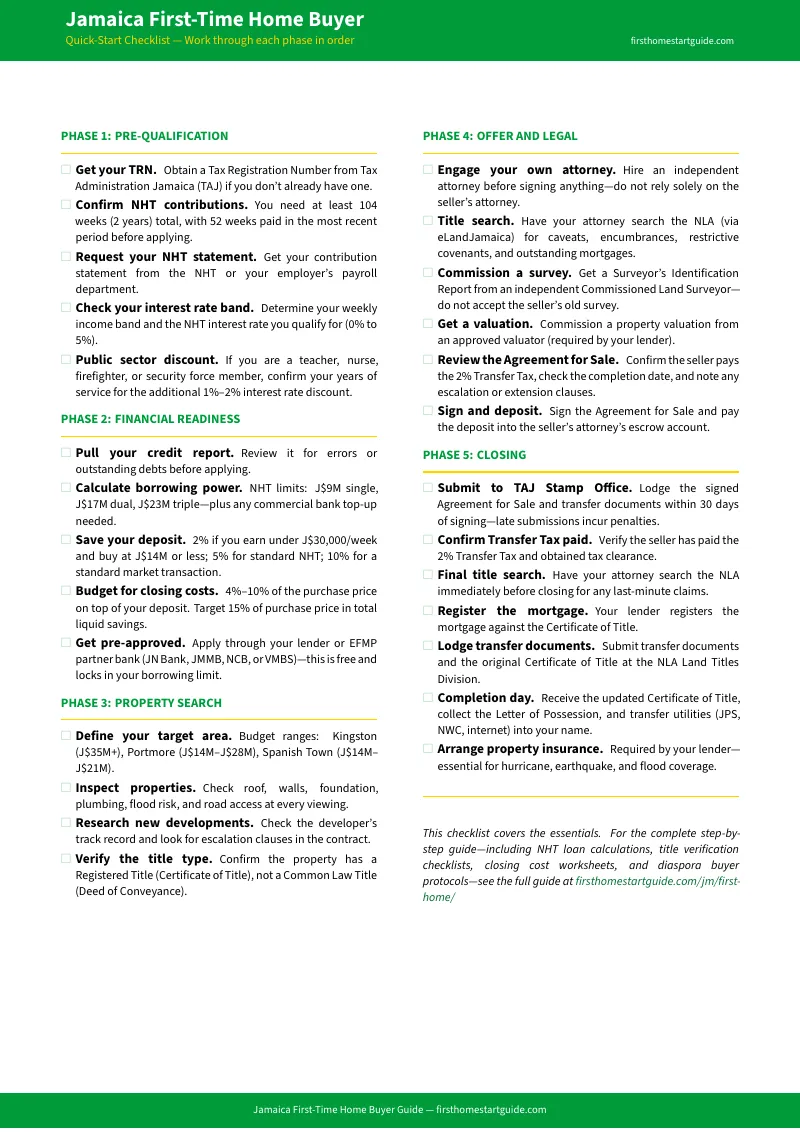

A comprehensive guide, a quick-start checklist, and 5 standalone printable worksheets (7 PDFs) — covering every stage from calculating your NHT borrowing power through to collecting your Certificate of Title, built specifically for the subsidies, risks, and legal frameworks that make buying in Jamaica different from anywhere else in the Caribbean:

NHT Loan Limits and the Special Low-Value Unit Allocation

Single buyers can borrow up to J$9 million through the standard NHT open market programme. But if you find a home priced at J$14 million or less, a special allocation lets you borrow up to J$12 million — J$3 million more than the standard limit. This allocation exists to prevent NHT subsidies from flowing to luxury developments and to channel single middle-income buyers into affordable housing. The guide maps every loan programme — Open Market, Build-On-Own-Land, House Lot, Homeowner's, and the SMART Energy Loan — with exact limits for single, dual, and triple co-applicants so you know your maximum borrowing power before you contact a lender.

Interest Rate Bands and Public Sector Discounts

NHT rates are not fixed — they are tied to your weekly income. If you earn minimum wage to J$30,000 per week, your rate is 0%. Up to J$42,000 per week, your rate is 2%. Compare that to commercial bank rates of 8.5% to 11%. On a J$9 million, 25-year loan, the spread between 0% NHT and 9% commercial rates means paying roughly J$12 million less over the life of the mortgage. For teachers, nurses, firefighters, and security force personnel, an additional 1% to 2% discount based on length of service can push your effective rate to zero. The guide includes the full rate table, public sector discount tiers, and worked calculations so you can see the exact monthly payment at your income level.

The EFMP — How Blended Mortgages Actually Work Now

If the property you want costs more than your NHT limit, you need a commercial bank loan to cover the gap. The External Financing Mortgage Programme replaced the older Joint Financing programme and changed the mechanics of how NHT and commercial funds are combined. The guide explains what changed, how to apply through the new structure, and how to calculate your blended monthly payment — the NHT portion at 0% to 5% and the commercial portion at 8.5% to 11% — so you know the true cost before you commit.

Registered Title vs. Common Law Title — The Risk That Can Cost You Your Home

Jamaica operates a Torrens-style registered title system. A Registered Title is a state-guaranteed Certificate of Title — indefeasible, with all encumbrances noted on the face of the document. A Common Law Title is a Deed of Conveyance prepared by an attorney for unregistered land. It provides no state guarantee. A single missing deed in the historical chain can invalidate the seller's right to sell. Transfers must be recorded at the Registrar General's Department in Spanish Town within two months or the transaction is legally void. Most commercial banks reject Common Law land as collateral. Converting to a Registered Title at the National Land Agency is a multi-year process requiring survey plans, statutory declarations, and substantial legal fees. The guide explains both title systems, the specific risks of Common Law Titles, and what your attorney must verify before you sign anything.

Transaction Costs — The Cash Nobody Tells You to Budget For

The purchase price is not what you pay. Total closing costs in Jamaica average 4% for cash transactions and can reach 10% when commercial mortgages are involved. The guide breaks down every cost element: the 2% Transfer Tax (paid by the seller, not you — a fact many buyers misunderstand), the flat J$5,000 stamp duty per document, the 0.5% NLA registration fee split 50:50, attorney fees at 2% to 3% plus 16.5% GCT, valuation reports, surveyor's identification reports, and lender processing fees. For a J$20 million home, the purchaser's total closing costs can exceed J$1 million in cash above the deposit. The guide includes a full cost schedule so you budget accurately from the start.

The Surveyor's Identification Report

Before any mortgage lender disburses funds, they require a Surveyor's Identification Report from a Commissioned Land Surveyor. This report verifies that the physical boundaries on the ground match the coordinates on the Registered Title, identifies any encroachments from neighbouring properties, and checks for restrictive covenant breaches. Costs are regulated: J$18,000 for quarter-acre properties, J$22,000 for properties under J$8 million, and 0.28% of the property value for higher-priced homes. The guide explains what this report covers, how much it costs at every price point, and why accepting the seller's old survey instead of commissioning your own is one of the most common — and most dangerous — shortcuts first-time buyers take.

Geographic Affordability — Kingston vs. Portmore vs. Spanish Town

Entry-level apartments in Kingston and St. Andrew start at J$35 million and climb past J$65 million. For a single buyer on a middle income, even the maximum NHT allocation of J$9 million leaves over J$26 million to finance through a commercial bank at rates close to 10%. The arithmetic is different in St. Catherine. In Greater Portmore, starter homes sit between J$14 million and J$28 million. In Spanish Town, gated scheme units start around J$14 million. The guide maps every major market — including Montego Bay for tourism workers and diaspora buyers — with entry-level prices, typical property types, and NHT financing feasibility for single buyers and joint applicants.

Joint Applications — Combining NHT Entitlements

Two NHT contributors applying together access up to J$17 million. Three kin-connected co-applicants access up to J$23 million. For a couple buying a J$20 million home in Portmore, the combined NHT limit covers 85% of the purchase price, leaving a manageable gap that can be financed commercially or covered from savings. The guide explains who qualifies as a co-applicant, how the interest rate is calculated using the weighted average of all co-applicants' incomes, and how to structure joint applications through EFMP partner banks.

Diaspora Buyer Guide

Jamaicans living in the United States, Canada, and the United Kingdom who want to purchase residential property in Jamaica face specific challenges: foreign income verification, remote documentation, power-of-attorney requirements, and the choice between JMD and foreign-currency mortgages. The guide covers the entire remote purchase process — from engaging a local attorney to managing the transaction from overseas — including the tax implications in your country of residence and the property tax obligations in Jamaica.

Government Housing Programmes

Beyond NHT loans, the Jamaican government operates additional housing access programmes: the Help-to-Own initiative for civil servants, JNHT developer schemes for affordable housing, and the under-35 quota that reserves 20% of NHT scheme units for younger contributors. The guide covers all active programmes, eligibility criteria, and application processes.

After You Buy — Post-Purchase Obligations

Owning a home in Jamaica comes with ongoing obligations: property tax filings with TAJ, property insurance (required by your lender and essential for hurricane, earthquake, and flood coverage), utility transfers, NHT repayment structure, and the first-year maintenance items that protect your investment. The guide covers the full post-purchase timeline so you are not caught by surprise after you receive the keys.

Standalone Printable Worksheets

In addition to the guide and checklist, you get 5 standalone worksheets designed to be printed and used during your home buying process:

- NHT Rate Card — A one-page reference showing every NHT loan programme limit, interest rate band, deposit requirement, and public sector discount. Print it and bring it to your bank appointment.

- Closing Cost Worksheet — A fillable worksheet where you enter your purchase price and calculate every Jamaica-specific transaction cost line by line, so you know exactly how much cash you need above the deposit.

- Mortgage Comparison Worksheet — Compare NHT-only, EFMP blended, and commercial-only financing side by side. Fill in your income band, calculate monthly payments for each option, and see the total cost difference over 25 years.

- Title Verification Checklist — A checklist to bring to property viewings and attorney meetings. Verify title type, check for Common Law red flags, confirm surveyor's report items, and track critical deadlines.

- Key Contacts & Institutions — A fridge-sheet reference card with every institution you will need (NHT, NLA, TAJ, EFMP partner banks), the documents required for your application, and the critical deadlines you cannot miss.

Who This Guide Is For

- NHT contributors earning J$30,000 to J$100,000 per week who have been paying into the Trust for years but cannot work out how their contributions translate into borrowing power, what interest rate band they fall into, or whether they qualify for the special J$12 million low-value unit allocation

- Couples and co-applicants planning to combine their NHT entitlements to buy a home in Portmore or Spanish Town and wanting to understand how blended mortgages work under the new EFMP programme

- Teachers, nurses, firefighters, and police officers who qualify for the public sector interest rate discount but do not know how to stack it with their income-based rate to minimise their monthly payment

- Single buyers targeting homes under J$14 million who need to understand the special NHT allocation and the 2% deposit reduction for lower earners

- Anyone looking at a property with a Common Law Title who needs to understand the financing restrictions, the Spanish Town recording deadline, and the conversion process before signing anything

- Diaspora Jamaicans in the US, Canada, or UK planning to buy property in Jamaica for retirement, investment, or family support and needing to navigate remote transactions, foreign-currency mortgages, and cross-border tax implications

Why Not Free Resources?

Free information on buying a home in Jamaica exists across a handful of government and bank websites. Here is what it actually delivers:

- The NHT website publishes loan limits, interest rate bands, and eligibility rules. It does not explain how the special J$12 million low-value unit allocation interacts with the 2% deposit reduction for lower earners, or how the EFMP programme structures blended mortgages. You get the statutory rules without the practical calculations that show what you will actually pay each month.

- JN Bank and VMBS publish mortgage calculators and basic buyer guides. They are designed to sell their own loan products. They do not provide unbiased comparisons of NHT-only financing versus blended EFMP financing, and they do not cover Common Law Title risks because it is not in their commercial interest to warn you away from a property they could finance.

- Attorney firm blogs publish technically accurate articles on conveyancing. They are sparse, written in legal jargon, and updated infrequently. They rarely address practical budgeting questions like how much cash you need above the deposit, or whether the 2% Transfer Tax is your responsibility or the seller's.

- Facebook and WhatsApp groups contain real buyer experiences mixed with outdated information. A 2024 thread about NHT loan limits does not reflect the June 2025 increases. Advice about the old Joint Financing programme does not apply to the new EFMP. Sorting current from outdated takes longer than reading a guide that has already done it.

This guide fills the Jamaica-specific gap — the space between knowing you want to buy a first home and knowing how to navigate a country where NHT benefits are generous but poorly explained, title risk can void a transaction, transaction costs catch buyers at closing, and the new EFMP programme changed how blended mortgages work.

— Less Than a Single Valuation Report

A property valuation in Jamaica costs J$50,000 to J$60,000 for homes under J$5 million, and scales up from there. Attorney fees for conveyancing run 2% to 3% of the purchase price plus 16.5% GCT. Losing the special J$12 million NHT allocation because you purchased a home priced at J$14.1 million instead of J$13.9 million costs you J$3 million in subsidized borrowing. Buying a property with a Common Law Title that your commercial bank will not accept as collateral can derail your entire purchase. A property with undisclosed boundary encroachments can trap you in a legal dispute that costs more than the surveyor's report that would have caught it.

This guide does not replace your attorney. But it gives you the NHT benefit calculations, EFMP blended mortgage structure, title risk assessment framework, transaction cost breakdown, and geographic affordability analysis that ensure you identify every Jamaica-specific risk and claim every available benefit before you sign an Agreement for Sale — not when the attorney's bill arrives, the bank rejects your title, or the NHT denies your allocation.

If it saves you from a single title risk, a single missed NHT allocation, or a single closing cost you did not budget for, it pays for itself before you finish reading it.

30-day money-back guarantee. If the guide does not sharpen your due diligence and protect your deposit in Jamaica's property market, you pay nothing.

Download the free Jamaica Quick-Start Home Buying Checklist to see the step-by-step framework covering pre-qualification, financial readiness, property search, offer and legal, and closing. When you are ready for the full NHT benefit calculations, title risk framework, transaction cost breakdown, and EFMP mortgage guide, the complete guide is here.

Your NHT contributions are your entitlement. This guide makes sure you claim every dollar of it.