You Can Afford the Mortgage Payment. It's the Transfer Duty Reforms, Conveyancing Tariffs, NHE Queue Realities, and PTO Land Traps That Nobody Assembled Into One Guide.

You found a three-bedroom freestanding house in Khomasdal for N$1.2 million. Or a sectional title townhouse in Kleine Kuppe where the monthly mortgage installment is less than your current rent. Or maybe you've been on the NHE waiting list since 2012 and you've just realized that with fewer than 700 houses built per year against 120,000 applicants ahead of you, the private market is your only realistic path to ownership.

Then Namibia's transaction layers arrive. The Khomasdal house has unapproved structures that the seller never regularized -- and retrospective building plans can take 3 to 6 months to approve, delaying your entire transfer. The Kleine Kuppe complex looks polished until you read the Body Corporate minutes and discover underfunded reserves, owner arrears, and a special levy pending. And that affordable plot on the outskirts of Windhoek? It's held under a Permission to Occupy certificate, not a freehold title deed -- meaning no bank in Namibia will give you a mortgage, and the PTO itself can be revoked by a traditional authority.

Here's the problem: Namibia combines a 300,000-unit housing backlog with a stagnant state developer that's built only 21,545 houses in 30 years, transfer duty legislation that was fundamentally reformed in October 2024, conveyancing fees locked to Law Society tariffs upheld by the Supreme Court, a dual land tenure system where some "properties" can't be mortgaged or even registered at the Deeds Registry, and a real estate information landscape dominated by South African content that references subsidy programs, tax brackets, and regulatory bodies that don't exist here. Each of these has cost real Namibian buyers real money because the information was scattered across bank brochures, conveyancer blogs, NHE application forms, and Reddit threads -- but nobody had mapped it into a single decision system built for Namibia's specific laws and costs.

The Namibia First-Time Home Buyer Guide is a Namibia Purchase Navigation System -- not a motivational overview about getting on the property ladder, but a structured decision framework that maps every transfer duty bracket, bank loan requirement, NHE eligibility threshold, conveyancing tariff, and land tenure risk into a process you work through before you sign anything. It replaces months of consuming South African advice that doesn't apply, waiting for NHE updates that never come, and guessing at transaction costs with a single reference that tells you exactly what to verify, exactly what the numbers should look like, and exactly where first-time buyers lose money in Namibia.

What's Inside the Namibia Purchase Navigation System

A 12-chapter guide, 5 standalone printable tools, and an 18-item Quick-Start Checklist -- covering every stage from credit repair through post-purchase essentials, built specifically for the regulatory complexity and information gaps that make buying in Namibia different from every other market:

October 2024 Transfer Duty Reform -- Fully Mapped

The Transfer Duty Amendment Act No. 6 of 2024 raised the tax-exempt threshold for natural persons to N$1,100,000 and introduced a new progressive sliding scale above that. It also closed the corporate shell loophole -- purchasing shares in a company or Close Corporation that owns residential property now triggers a flat 12% transfer duty on the full value. The guide walks through every bracket with worked examples at N$900,000, N$1.5 million, N$2.5 million, and N$5 million, so you know your exact transfer duty liability before making an offer. Most online calculators still reference the old thresholds.

Transaction Cost Breakdown -- Every Fee, Every Line Item

The purchase price is only the beginning. Conveyancing fees are fixed by the Law Society of Namibia's prescribed tariff schedule -- you cannot negotiate them. Bond registration costs follow a separate tariff. Then add 15% VAT on legal fees, N$345 per Deeds Registry fee (recently increased), FICA compliance charges, bank valuation fees, and municipal clearance costs. On a N$1.5 million property, these costs can add N$70,000+ in cash you need above your deposit. The guide calculates the total at multiple price points so you're not surprised at the conveyancer's office.

NHE vs Private Market -- Honest Assessment

The NHE has 120,000 applicants and builds fewer than 700 houses per year. The income cap is N$15,000 for individuals, N$30,000 for joint applications. If you qualify, register -- but the guide explains why the private market is your realistic primary strategy, covers the zero-deposit bank products that make it accessible (FNB EasyBond at 105% LTV, Nedbank at 108%), and models what the NHE pipeline actually looks like for someone joining the queue today. No false hope, no dismissal -- just the numbers.

The PTO and FLTS Land Tenure Trap

Not everything that looks like property ownership in Namibia actually is. Permission to Occupy certificates are personal user rights, not real rights -- they're not registered at the Deeds Registry, they can be revoked, and no commercial bank will accept them as mortgage collateral. The Flexible Land Tenure Act introduced Starter Title and Land Hold Title as upgradeable alternatives, but only Land Hold Title can be mortgaged because it requires a surveyed, demarcated plot. The guide explains the entire dual tenure system so you know exactly what legal right you're buying before you hand over money.

Bank Loan Requirements -- Document by Document

Banks cap your mortgage installment at 30% of gross monthly income. But approval depends on six months of clean bank statements with zero overdraft usage, a credit report from TransUnion Namibia with no unpaid accounts, and -- if you're self-employed -- two years of audited financial statements, cash flow forecasts, and a NamRA tax clearance certificate. The guide lists every document for both salaried and self-employed applicants at FNB, Bank Windhoek, Nedbank, and Standard Bank, and explains what specifically triggers a decline so you can fix it before you apply.

The South African Content Filter

Because Namibia's legal system shares roots with South Africa's, Namibian buyers constantly absorb South African property advice. Three mismatches cost the most: FLISP (a South African government deposit subsidy) does not exist in Namibia, SA transfer duty brackets don't match Namibian ones, and the NHBRC (South Africa's construction quality regulator) has no jurisdiction here. The guide is built entirely on Namibian legislation, Namibian bank products, and Namibian conveyancing practice -- every number, every threshold, every legal reference is verified against Namibian law.

Standalone Printable Tools Included

Beyond the 12-chapter guide, you get 5 standalone PDFs designed to print and bring to bank appointments, property viewings, and conveyancer meetings:

- October 2024 Transfer Duty Tables -- the complete post-reform bracket schedule with worked examples at three price points and a fillable calculator for your property

- Transaction Cost Worksheet -- calculate every N$ you need beyond the purchase price: duties, conveyancing fees, Deeds Registry costs, and municipal deposits

- Land Tenure Verification Card -- one-page reference comparing freehold, sectional title, PTO, and FLTS titles at a glance, with verification steps to confirm what you're buying

- Bank Loan Document Checklist -- every document required for salaried and self-employed mortgage applicants, organised by stage from pre-application through closing

- Body Corporate Audit Checklist -- how to review a sectional title complex's financial health, AGM minutes, management rules, and physical condition before signing

Who This Guide Is For

This guide is for first-time home buyers in Namibia who:

- Are paying N$8,000 to N$15,000+ in monthly rent and have realized they could be building equity for the same amount -- but don't know the actual total cash requirement to get into the private market beyond the deposit

- Have been on the NHE waiting list for years and need to understand whether the private market is now their better option, what zero-deposit bank products are available, and how to qualify

- Are civil servants eligible for the HOSSM housing subsidy or GIPF pension-backed loans but have never navigated the application process -- and don't realize these programs can unlock financing they thought was out of reach

- Need to know their exact transfer duty liability under the October 2024 reforms -- including whether buying through a company or CC still saves money (it doesn't -- the loophole is closed)

- Are considering sectional title townhouses and need to understand Body Corporate obligations, levy structures, exclusive use areas, and how to audit a complex's financial health before signing the Deed of Sale

- Are looking at property outside established suburbs and need to know the difference between freehold title, PTO certificates, Starter Title, and Land Hold Title -- and which ones banks will actually finance

- Are members of the Namibian diaspora buying from South Africa, the UK, or Germany, and need to understand the 50% foreign-deposit requirement, exchange control regulations, and the prohibition on purchasing agricultural commercial farmland

Why Not Free Tools and Bank Brochures?

Free information on buying property in Namibia exists. Here's what it actually delivers:

- Bank brochures and online calculators (FNB HomeOwners Book, Bank Windhoek home loan pages) explain their own products but don't guide you through independent valuations, negotiating agent commissions, or comparing loan offers across multiple banks. They're marketing tools designed to acquire your mortgage application -- not neutral buying guides.

- Estate agency blogs (Pam Golding Namibia, Integrated Properties, MyProperty Namibia) publish market reports and introductory articles. They're naturally aligned with seller-side interests and rarely cover hidden transaction costs, structural defect identification in Windhoek complexes, or the financial risks of specific Body Corporate arrangements.

- South African real estate content is consumed heavily by Namibian buyers because Namibia has no centralized first-time buyer resource. But FLISP subsidies don't exist here, SA transfer duty brackets don't match, and the NHBRC has no authority in Namibia. Applying South African advice to a Namibian purchase creates confusion on tax, subsidies, and quality certification at every step.

- Reddit (r/Namibia) and Facebook property groups contain genuine peer experiences -- Windhoek complex reviews, mortgage comparisons, NHE frustrations. But advice is mixed with outdated information, seller-disguised listings, and opinions based on South African norms. Extracting reliable, current Namibian-specific guidance requires cross-referencing against legislation and bank policies that most posters haven't read.

This guide fills the Namibia-specific gap -- the space between knowing you want to buy your first home and knowing exactly how to navigate a market where 300,000 families are waiting for houses that aren't being built, transfer duty law was rewritten six months ago, land tenure comes in forms that look like ownership but aren't, and the most accessible property advice is written for a country with different tax brackets, different subsidies, and different regulatory bodies. It's the analysis that would take a conveyancer, a mortgage specialist, and a land rights adviser to assemble -- structured as a permanent reference you own.

-- Less Than One Building Compliance Delay

A single unapproved structure that delays your transfer by three months while you keep paying rent. A transfer duty calculation based on pre-October 2024 thresholds that leaves you short at the conveyancer's office. A PTO certificate you thought was freehold title, locking you out of bank financing entirely. An NHE application you waited eight years on while zero-deposit private market products existed the whole time. A Body Corporate with underfunded reserves and a special levy you discover after you've signed the Deed of Sale.

This guide doesn't replace your conveyancer or your mortgage adviser. But it gives you the transfer duty calculation tables, bank document checklists, land tenure verification framework, NHE vs private market comparison, and Body Corporate audit checklist that ensure you identify every Namibia-specific cost and legal risk before you're financially committed -- instead of discovering them when your deposit is already on the line.

If it catches a single PTO before you pay for it, prevents a single transfer delay by flagging unapproved structures in your inspection, or saves you from budgeting with the wrong transfer duty brackets, it pays for itself before you've finished reading Chapter 6.

30-day money-back guarantee. If the guide doesn't sharpen your analysis and protect your deposit in Namibia's property market, you pay nothing.

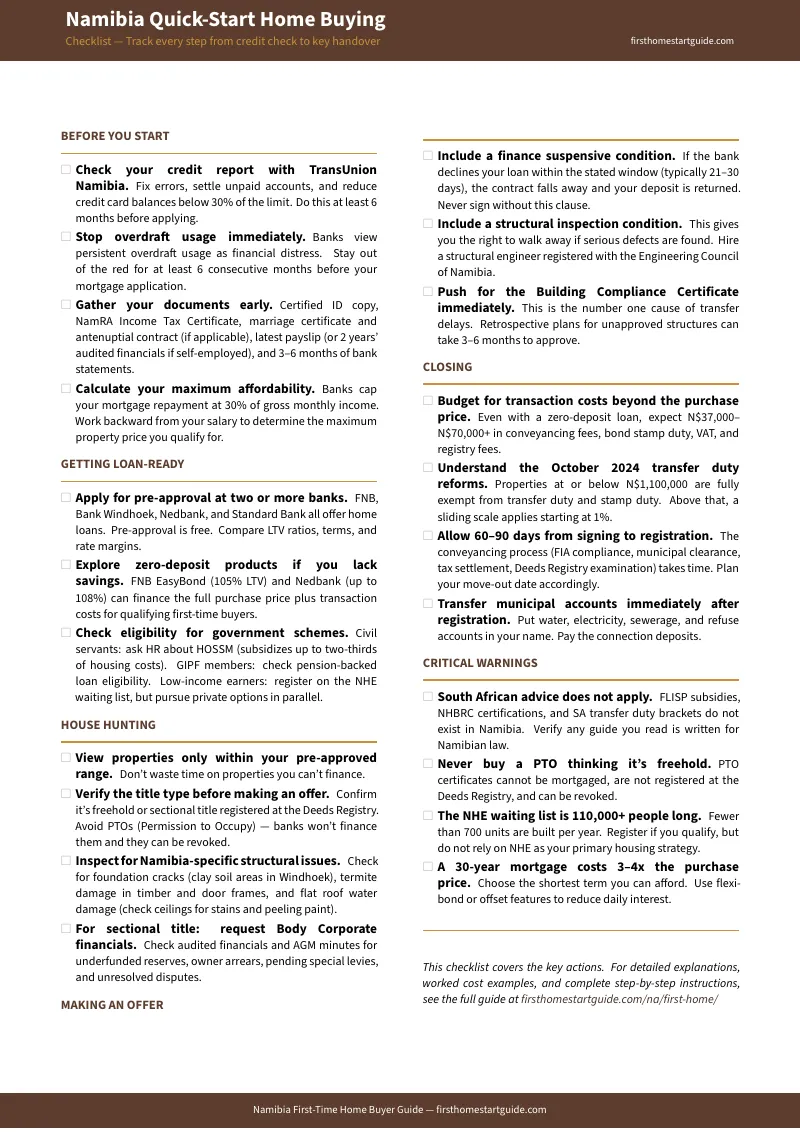

Download the free Namibia Quick-Start Home Buying Checklist to see the 18-item action plan covering credit preparation, document gathering, property inspection, offer protection, and closing costs. When you're ready for the full transfer duty tables, bank comparison framework, land tenure guide, and 12-chapter buying system, the complete guide is here.

The property looks right for your budget. This guide tells you whether Namibia's legal and financial system agrees.