The Yield Looks Great on Property.com.na. Namibian Law Will Decide Whether You Keep It.

You found a three-bedroom house in Pioneerspark listed at N$1.5 million with tenants paying N$9,000 a month. Or a student accommodation opportunity near UNAM where the university has 2,389 applicants competing for 1,150 campus beds and private rooms command N$3,000 per student. Or a sectional title apartment in Swakopmund where Airbnb data shows $9,860 in annual revenue at a 31% occupancy rate. The gross yield clears 7%. The numbers work.

Then reality shows up. The Pioneerspark tenant stops paying rent and you change the locks — only to receive a letter from their attorney citing Article 80 of the Namibian Constitution, informing you that self-help eviction is illegal and that only the Deputy Sheriff, executing a court order obtained through a process that takes 3 to 9 months, can legally remove an occupant. The Swakopmund apartment generates strong December revenue but sits empty from April to September, and your body corporate just imposed a special levy for sea-salt corrosion repairs you did not budget for. The student rooms near UNAM violate municipal density zoning and the city council revokes your occupancy certificate — zero rental income while you fight the administrative appeal.

Here is what no single resource explains: Namibia layers constitutional tenant protections (the Rents Ordinance of 1977 requires 3 months' notice where a Rent Board exists, Article 80 of the Constitution prohibits any eviction without a fair hearing, and the judicial process from breach notice through Deputy Sheriff execution takes 3 to 9 months), a tax system with powerful but misunderstood incentives (the 20% initial building allowance under Section 17(1)(f) can shield hundreds of thousands of dollars in rental income, but the October 2024 Transfer Duty Amendment closed the CC share-transfer loophole that sophisticated investors relied on for decades), Bank of Namibia financing regulations (100% LTV on second properties since October 2023, but a rigid 30% gross income affordability ceiling that banks enforce without exception), exchange control rules that can trap foreign capital indefinitely (the Bank of Namibia will block repatriation of sale proceeds if you cannot produce the original deal receipts proving legal capital introduction), and regional yield disparities so extreme that a Windhoek investment earning 5.5% and a Swakopmund short-term rental earning double-digit returns require completely different operational strategies. Every one of these has cost real investors real money — not because the information did not exist, but because it was scattered across FNB Namibia marketing booklets, WKH Law corporate blog posts, Bank of Namibia regulatory circulars, and Facebook group threads that may have been accurate before the October 2024 amendments.

The Namibia Investment Property Guide is a Namibian Investor Compliance and Yield System — not a motivational overview of Southern African real estate, but a structured due diligence framework that maps every Namibia-specific legal requirement, NamRA tax calculation, Bank of Namibia financing regulation, and regional yield profile into a process you work through before you sign the Offer to Purchase. It replaces months of cross-referencing conveyancer advice, NamRA interpretation notes, Bank of Namibia circulars, and Deeds Registry procedures with a single reference that tells you exactly what to verify, exactly how the numbers should work, and exactly where deals go wrong.

What's Inside the Namibian Investor Compliance and Yield System

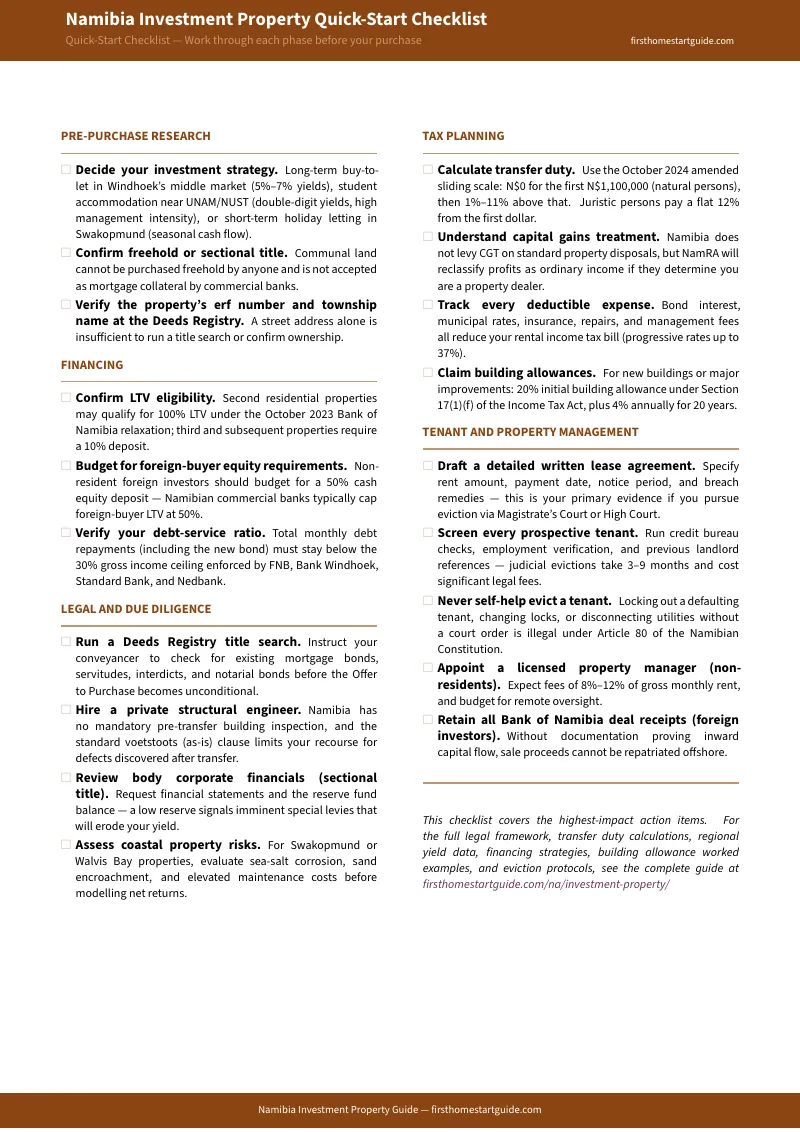

A 12-chapter guide, a standalone due diligence checklist, and 6 printable tools (transfer duty worksheet, building allowance calculator, eviction protocol card, regional yield reference, foreign investor capital flow checklist, and 20-year cash flow template) — covering every stage from financing through post-purchase operations, built specifically for the legal and tax framework that makes Namibia different from every other property market:

The Rents Ordinance Eviction Framework

The single most dangerous legal trap for Namibian landlords. Self-help eviction — changing locks, disconnecting utilities, seizing possessions — is illegal under Article 80 of the Namibian Constitution. Every eviction must follow a court process: proper written notice (3 months where a Rent Board exists, 30 days under common law), filing at the Magistrate's Court or High Court, proving both rightful ownership via title deed and unlawful possession via breach of contract, and execution by the Deputy Sheriff with police assistance if necessary. Contested evictions take 3 to 9 months. The guide maps the complete protocol so you budget legal risk into every deal from day one — not after your first non-paying tenant refuses to leave.

The 20% Building Allowance — The Full Calculation

Namibia's most powerful and most underutilized tax benefit. Section 17(1)(f) of the Income Tax Act allows a 20% initial deduction on the cost of erecting a building used for trade purposes, followed by 4% annually for 20 years. Build a purpose-built rental property costing N$2 million and you deduct N$400,000 from taxable income in year one, then N$80,000 per year for two decades. The guide includes the standalone building allowance calculator so you can model the exact tax impact on your specific project — because most investors do not know this provision exists, and those who do rarely calculate it correctly.

Transfer Duty After the October 2024 Amendments

The Transfer Duty Amendment Act No. 6 of 2024 closed the loophole that allowed investors to avoid transfer duties by purchasing shares in a Close Corporation or member's interest in a Trust that owned the property. The definition of "property" now explicitly includes shares or member's interests in entities owning residential property. If you are relying on pre-2024 tax advice that recommends CC structuring for residential acquisitions, your strategy is broken. The guide includes the complete post-amendment sliding scale for natural persons (exempt up to N$1,100,000, then 1% to 11%) and the flat 12% rate for juristic persons, plus the standalone transfer duty worksheet for calculating exact costs on any deal.

Bank of Namibia Financing and the 30% Ceiling

The October 2023 LTV relaxation eliminated the deposit requirement for second residential properties and reduced it to 10% for third and subsequent properties. This sounds like an open door — until the 30% gross income affordability ceiling shuts it. Banks will not approve a mortgage if your total monthly debt repayments exceed 30% of gross income. The guide covers extended-term strategies (up to 30 years through Bank Windhoek to reduce monthly instalments), the commercial finance option for tenanted buildings above N$1.5 million, and the non-resident reality: foreign buyers face a 50% maximum LTV and typically need to purchase with cash.

Exchange Control — Getting Capital In and Out

For South African, diaspora, and international investors, exchange control is the silent killer. The Bank of Namibia's Exchange Control Regulations of 1961 require all foreign funds to flow through an Authorized Dealer, with every deal receipt and bank endorsement retained permanently. Without proof that purchase funds were legally introduced into Namibia, the Bank of Namibia will block repatriation of sale proceeds — your capital is trapped. Rental income repatriation requires the lease agreement, a NamRA Good Standing Certificate, and an auditor's confirmation. The guide includes the standalone foreign investor capital flow checklist that documents every step from capital introduction through eventual repatriation.

Regional Market Analysis — Five Zones, Matched to Strategy

Windhoek middle market (5% to 7% gross yields, stable civil servant demand), Windhoek student accommodation near UNAM and NUST (double-digit yields, 36,000-bed shortfall, high management intensity), Swakopmund holiday rentals ($9,860 average annual Airbnb revenue, 31% occupancy, seasonal cash flow), Walvis Bay industrial corridor (port expansion, offshore energy, green hydrogen projects driving executive housing demand), and Luderitz speculative frontier (Hyphen Hydrogen Energy project, high upside contingent on mega-projects reaching financial close). Each zone analysed with yield data, tenant profiles, and risk factors. The standalone regional yield reference card gives you a printable comparison to take to your conveyancer.

NamRA Tax Architecture

Rental income taxed at progressive rates from 0% (first N$100,000 exempt) to 37% (above N$1,550,000). Corporate rates dropping from 31% to 28% over the next two fiscal years. No Capital Gains Tax on standard disposals — but NamRA will reclassify profits as ordinary income if they determine you are a property dealer. Withholding taxes for non-residents: 10% on interest (final, withheld by bank), 10% to 20% on dividends via the Non-Resident Shareholders Tax. The Double Taxation Agreement with South Africa may provide relief. Every deduction mapped: bond interest, municipal rates, insurance, management fees, repairs, body corporate levies.

The 20-Year Cash Flow Model

A worked example projecting gross rent, net operating income, tax liability, and property value over 20 years — using a N$1,500,000 Pioneerspark house as the baseline. Cumulative net rental income of approximately N$2,540,000 plus capital appreciation of N$2,480,000 with zero Capital Gains Tax on disposal. The standalone 20-year cash flow template lets you plug in your actual purchase price, rental income, and expense assumptions to model your specific deal.

Who This Guide Is For

This guide is for property investors targeting the Namibian market who:

- Are Namibian professionals earning N$20,000+ per month who want to deploy bonuses, maturing policies, or surplus income into rental property — and need to understand whether the deal actually works once you account for transfer duty, conveyancer fees, the 30% affordability ceiling, municipal rates, and the 3-to-9-month eviction timeline, not the gross yield projection from the estate agent

- Are South African investors seeking geographic diversification without currency risk through the NAD/ZAR 1:1 peg and zero Capital Gains Tax — and need to navigate cross-border financing restrictions, exchange control documentation, the Non-Resident Shareholders Tax, and remote property management before you commit capital across the border

- Are Namibian diaspora living in South Africa, the UK, or Germany who want a physical foothold in your home country — and need clarity on withholding taxes, non-resident LTV limitations, apostille requirements for offshore document signing, and the capital introduction trail that determines whether you can ever repatriate your money

- Are SME owners or business operators with excess retained earnings seeking to convert corporate profits into personal wealth through property — and need to understand that the October 2024 Transfer Duty Amendment closed the CC share-transfer loophole, that juristic persons pay a flat 12% transfer duty from the first dollar, and that the corporate tax rate reduction trajectory affects your entity structuring decision

- Are yield-seeking retirees with cash savings being eroded by 5.1% inflation who need inflation-linked monthly cash flow from a tangible asset — and want the eviction protocol, tenant vetting framework, and maintenance budgeting that addresses the operational risks that keep conservative investors on the sideline

Why Not Free Tools and Forums?

Free information on Namibian property investing exists across several sources. Here is what it actually delivers:

- FNB Namibia and Bank Windhoek property booklets explain the bond application process for their specific mortgage products. They do not explain how to calculate post-amendment transfer duty on the sliding scale, how the 20% building allowance under Section 17(1)(f) reduces your effective tax rate over 20 years, or how the 30% gross income ceiling interacts with extended-term loan structuring. You get a mortgage sales pitch without the tax and legal analysis that determines whether a specific deal works.

- Facebook groups ("Namibia Property Investment," "Windhoek Real Estate") are where someone says you can still avoid transfer duty through CC share transfers (you cannot since October 2024), someone else says you can change the locks on a non-paying tenant (you will face a court action under Article 80 of the Constitution), and a third person quotes South African PIE Act provisions that do not apply in Namibia (the Rents Ordinance of 1977 governs here, with entirely different notice periods and procedures). Genuine experience reports exist alongside advice that can trigger legal proceedings or tax penalties.

- South African investment property guides are the most dangerous shortcut. While the NAD/ZAR peg and shared banking heritage create a false sense of familiarity, the underlying legal frameworks are entirely distinct. South Africa's PIE Act eviction process, Section 13sex depreciation allowance, and ring-fencing rules under Section 20A do not exist in Namibian law. Applying South African tenant law to a Namibian eviction will result in procedural failure. The tax codes, transfer duty structures, and building allowances are not interchangeable.

- Law firm blog posts (WKH Law, Engling Stritter) occasionally publish accurate technical articles on niche topics — the 2024 Transfer Duty Amendment analysis, eviction protocol summaries. These are deeply siloed, written in dense legalese, and require you to piece together a complete investment strategy from dozens of separate corporate blogs. Consulting these firms directly for foundational education costs N$2,000 to N$4,000 per hour.

This guide fills the Namibia-specific gap — the space between knowing that property investing works in principle and knowing how to structure, evaluate, and operate a portfolio under the specific legal, tax, and regulatory framework that governs every dollar you invest in Namibian residential real estate. It is the analysis that would take a conveyancer, a NamRA tax specialist, and a property management professional to assemble — structured as a reference you own permanently.

— Less Than One Hour with a Conveyancer

A single transfer duty miscalculation after the October 2024 amendments can cost tens of thousands of Namibian dollars. A self-help eviction attempt on a non-paying tenant exposes you to a court action that takes 3 to 9 months and costs more in legal fees than the unpaid rent. An exchange control documentation gap means your sale proceeds are trapped in Namibia indefinitely. A student accommodation conversion that violates municipal zoning loses its occupancy certificate and generates zero income while you appeal. A Swakopmund holiday rental without a sea-salt corrosion maintenance budget erodes your yield within three years.

This guide does not replace your conveyancer or your NamRA tax advisor. But it gives you the eviction protocol, transfer duty worksheet, building allowance calculator, exchange control checklist, and regional yield analysis that ensure you identify every Namibia-specific risk before you sign the Offer to Purchase — instead of discovering them on your first tenant default, your first NamRA assessment, or your first attempt to repatriate capital.

If it catches a single transfer duty error, prevents a single illegal eviction attempt, or ensures your capital introduction documentation is complete before you need it, it pays for itself before you have finished reading it.

30-day money-back guarantee. If the guide does not sharpen your due diligence and protect your capital in Namibia's regulatory environment, you pay nothing.

Download the free Namibia Quick-Start Home Buying Checklist to see the due diligence framework covering pre-purchase research, financing, legal verification, tax planning, tenant management, and ongoing operations. When you are ready for the full eviction protocol, building allowance calculations, exchange control procedures, and 12-chapter investment system, the complete guide is here.

The yield looks good on the listing. This guide tells you whether Namibian law agrees.