You've Saved the Deposit. The Rules Just Changed on How Much You Can Actually Borrow.

You spent three years contributing to KiwiSaver, watched your balance pass the 5% deposit threshold, and started looking at listings with real intent. Then the First Home Grant was terminated. Then the First Home Partner scheme closed. Then the Reserve Bank imposed a debt-to-income limit of 6 — and suddenly your deposit is irrelevant because your income caps out your borrowing power $150,000 below the median Auckland home.

So you start researching. Kāinga Ora's website explains the First Home Loan criteria in language written for policy analysts. Sorted.org.nz has a mortgage calculator that doesn't account for DTI restrictions. ANZ's first-home guide conveniently omits that their lending criteria differ from Kiwibank's by tens of thousands of dollars. Reddit says one couple got their KiwiSaver withdrawal processed in two weeks; another says their provider took four weeks and they nearly defaulted on settlement. A mortgage broker wants $800 before they'll explain the difference between a First Home Loan and a standard low-deposit mortgage.

Here's what no single resource explains: New Zealand has a KiwiSaver withdrawal process with a 15-business-day minimum timeline and a mandatory $1,000 lockout, a leaky building crisis that has made an entire generation of housing stock unmortgageable, four different title structures with hidden legal liabilities, and a DTI regime that has shifted the constraint from deposit size to income level — and getting any one of these wrong can cost you tens of thousands or collapse your purchase entirely.

The New Zealand First-Time Home Buyer Guide is a Property Defence System. Not a summary of government programs — a structured decision framework that calculates your true borrowing capacity under DTI limits, maps the KiwiSaver withdrawal timeline against your settlement obligations, identifies the physical red flags of leaky buildings, and walks you through every stage from pre-approval through to key handover. It replaces months of contradictory forum threads, biased bank guides, and outdated government pages with a process you can work through chapter by chapter.

What's Inside the Property Defence System

A complete guide, seven standalone printable worksheets, and a quick-start checklist — covering every stage from DTI calculation through settlement. Print the worksheets and bring them to mortgage appointments, open homes, and settlement day:

The DTI Borrowing Capacity Engine

Your maximum mortgage under the Reserve Bank's 6x DTI rule, calculated with every debt category that banks actually count — including credit card limits you aren't using, student loans, and car finance. The guide includes a worked example showing exactly how a couple on $135,000 combined income reaches their ceiling, plus the two critical exemptions that bypass DTI entirely: new builds and the Kāinga Ora First Home Loan. If you have unused credit cards open, this chapter alone changes your borrowing power by tens of thousands.

KiwiSaver Withdrawal Mechanics

The exact process for withdrawing your KiwiSaver balance as a first-home deposit — the $1,000 mandatory remaining balance, the Australian super transfer lockout, the certified ID and solicitor's letter of undertaking, and the 15-business-day minimum processing timeline that catches buyers who agree to short settlement periods. The guide maps the withdrawal timeline against your offer conditions so you never find yourself legally bound to settle with your funds stuck in transit.

First Home Loan Decision Framework

With the First Home Grant terminated and the First Home Partner scheme closed, the Kāinga Ora First Home Loan is the last remaining government deposit support. The guide breaks down the income caps ($95,000 individual, $150,000 couple), the 1.2% Lender's Mortgage Insurance premium, the strict genuine-cash deposit requirement, and the mathematical paradox where qualifying for the loan's income cap still leaves you short of habitable property in Auckland under DTI limits. Including the participating lenders list and what makes each one calculate DTI differently.

Leaky Building Red Flag Identification

The most expensive mistake a first-time buyer can make in New Zealand is purchasing a monolithic-clad property from the 1990–2005 building era. Auckland reclads currently cost $330,000 to $500,000. Banks refuse to lend against identified high-risk builds. The guide covers the visual red flags — no eaves, flat roofs, internal gutters, smooth plaster cladding over untreated timber — the cladding failure rates by type (monolithic stucco: 95%), and why community forums unanimously warn against buying cheap leaky apartments even with cash.

Title Structure Decoder

New Zealand uses four title types, each with distinct legal risks. Fee simple is safest but most expensive. Cross-lease titles require that the registered flats plan matches the actual building footprint — defective cross-leases are common and costly. Unit titles carry mandatory body corporate disclosures under the Unit Titles Act, with pre-contract and pre-settlement statements most buyers don't know to request. Leasehold titles look artificially cheap but expose you to devastating ground rent increases on renewal. The guide explains each structure's lending implications, hidden liabilities, and what your solicitor should check before you commit.

Auction Survival and Due Diligence Cost Management

Buying at auction in New Zealand means all bids are unconditional — every dollar spent on LIM reports ($300–$400), building inspections ($400–$700), registered valuations ($700–$1,200), and solicitor reviews is sunk before you even raise your hand. Three unsuccessful auctions can burn through $5,000 in non-refundable costs. The guide covers defensive bidding strategies, when to let a property pass in to negotiate privately, how to use irregular bid increments to disrupt competitors, and the critical difference between auction, tender, deadline sale, and negotiation methods.

Insurance, Natural Hazards, and Climate Risk

No insurance means no mortgage means no settlement. The guide covers NHCover building and land coverage, the climate red-lining that is making properties in flood-prone and liquefaction-prone areas uninsurable, and the specific council hazard overlays you need to check before making an offer. Including the Christchurch Technical Categories that still affect lending and insurance for properties on the former red zone fringe.

Regional Market Intelligence

Auckland, Wellington, Christchurch, and regional centres each present different price-to-income realities, physical risks, and opportunities. The guide provides median prices, key risk factors, and strategic considerations for each — including Wellington's liquefaction risk on the valley floor, Christchurch's post-earthquake TC categories, and regional centres where your borrowing power stretches furthest.

Who This Guide Is For

This guide is for first-time home buyers in New Zealand who:

- Have a KiwiSaver balance approaching the 5% deposit threshold but don't understand the withdrawal mechanics — the $1,000 lockout, the 15-business-day timeline, the Australian super transfer restriction — and can't afford to get the timing wrong against their settlement date

- Earn a solid dual income but find that DTI limits cap their borrowing below the median home price in their city — and need to understand whether a First Home Loan, a new build exemption, or clearing existing debt changes the equation

- Have been told to "check the Kāinga Ora website" and found eligibility criteria written for policy analysts that don't explain how the income caps interact with DTI limits, or what happens when you stack First Home Loan LMI costs on top of a 5% deposit

- Are viewing properties built between 1990 and 2005 and need to know exactly which cladding types, roof profiles, and ground clearances signal a leaky building that will cost more to fix than the property is worth

- Lost a bid at auction after spending $2,000 on due diligence and refuse to enter another auction without a clear defensive strategy, a hard maximum, and a method for managing the sunk cost exposure

- Are returning from overseas with savings but face lending barriers — employment contract requirements, currency buffer demands, and non-bank LVR restrictions — that standard guides don't cover

Why Not Free Resources?

Free information on buying your first home in New Zealand is everywhere. Here's what it actually delivers:

- Kāinga Ora and HUD maintain the most accurate information on First Home Loan criteria and property title structures. Presented in dense, bureaucratic language that covers every eligibility condition without once explaining how those conditions interact with DTI limits, KiwiSaver timing, or auction mechanics. You get the rules for the First Home Loan. You get the income caps. You never get a single page explaining the mathematical paradox where qualifying for the income cap still leaves you short of habitable property in major cities.

- Sorted.org.nz has excellent mortgage calculators and KiwiSaver tools — including ESCT tax calculations most buyers wouldn't think to check. But the calculators operate in an academic vacuum. They'll tell you your maximum mortgage. They won't tell you what happens when the withdrawal takes 20 business days and your settlement is in 15, or that the property you can afford on paper has monolithic cladding that makes it unmortgageable.

- Bank guides (ANZ, ASB, Kiwibank, Westpac) are polished, visually appealing, and designed to originate mortgages. They minimise the sunk cost reality of auction due diligence, obscure the differences between their own lending criteria and competitors, and never mention that a different bank might lend you $30,000 more for the same income because they calculate DTI differently.

- Mortgage brokers (Squirrel, Mortgage Lab) produce excellent scenario-based content that explains how lending works in practice. Then the article ends with a consultation booking form. They'll explain alt-doc loans for the self-employed brilliantly. They won't explain why the leaky apartment you found at a price you can finally afford is a financial trap that no broker commission can justify recommending.

This guide fills the integration gap — the space between knowing each system exists and understanding how they interact under pressure. DTI limits plus KiwiSaver timing plus title type risk plus due diligence sunk costs plus physical property hazards, mapped as a single structured process. It's the analysis a truly independent advisor would give you, laid out as a workbook you own permanently.

— Less Than One Building Inspection

A single building inspection costs $400 to $700. A registered valuation runs $700 to $1,200. A mortgage broker consultation starts at $800. A LIM report costs $300 to $400 every time you bid on a property.

This guide doesn't replace your solicitor or your mortgage application. But it gives you the DTI calculations, KiwiSaver withdrawal timeline, due diligence framework, leaky building identification system, and title structure analysis that ensure you walk into every appointment, viewing, and auction knowing exactly where you stand — instead of learning expensive lessons in real time.

If it prevents a single overbid at auction, identifies a single leaky building before you commission the building report, or catches a single KiwiSaver timing error before settlement day, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't make your home buying process clearer and your financial position stronger, you pay nothing.

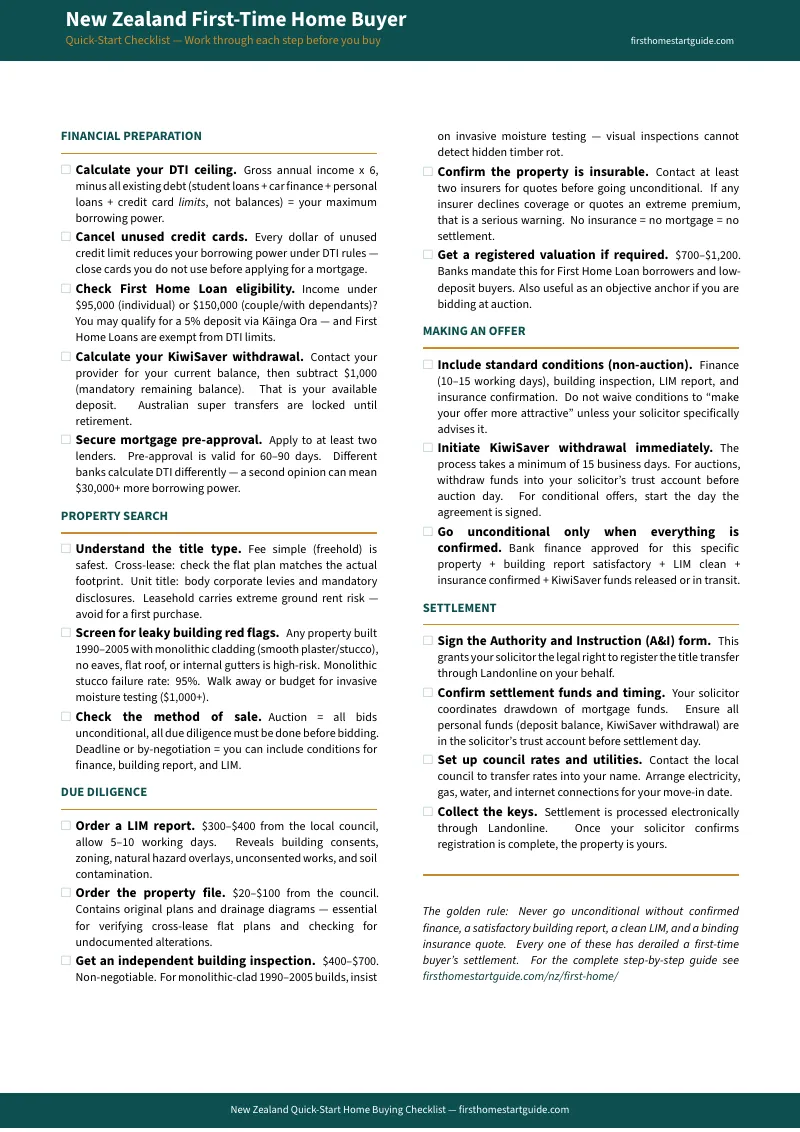

Download the free Quick-Start Checklist to see the step-by-step action plan covering DTI calculation, KiwiSaver withdrawal, and due diligence sequencing. When you're ready for the full Property Defence System — borrowing capacity analysis, leaky building identification, title structure decoder, auction strategies, and the complete settlement timeline — the guide is here.

You've saved the deposit. Now build the defence that gets you the keys without the catastrophe.