The Tax Rules Just Changed in Your Favour. The Credit Rules Changed Against You. The Investors Who Win From Here Are the Ones Who Understand Both Simultaneously.

You have $250,000 in usable equity in your Auckland home. Interest deductibility is back to 100%. The bright-line test is down to two years. Interest rates are falling. Everything says buy. You start modelling a $650,000 rental in Christchurch — the yield is 5.3%, the rent covers the mortgage at today's rates, and you can sell tax-free in 25 months.

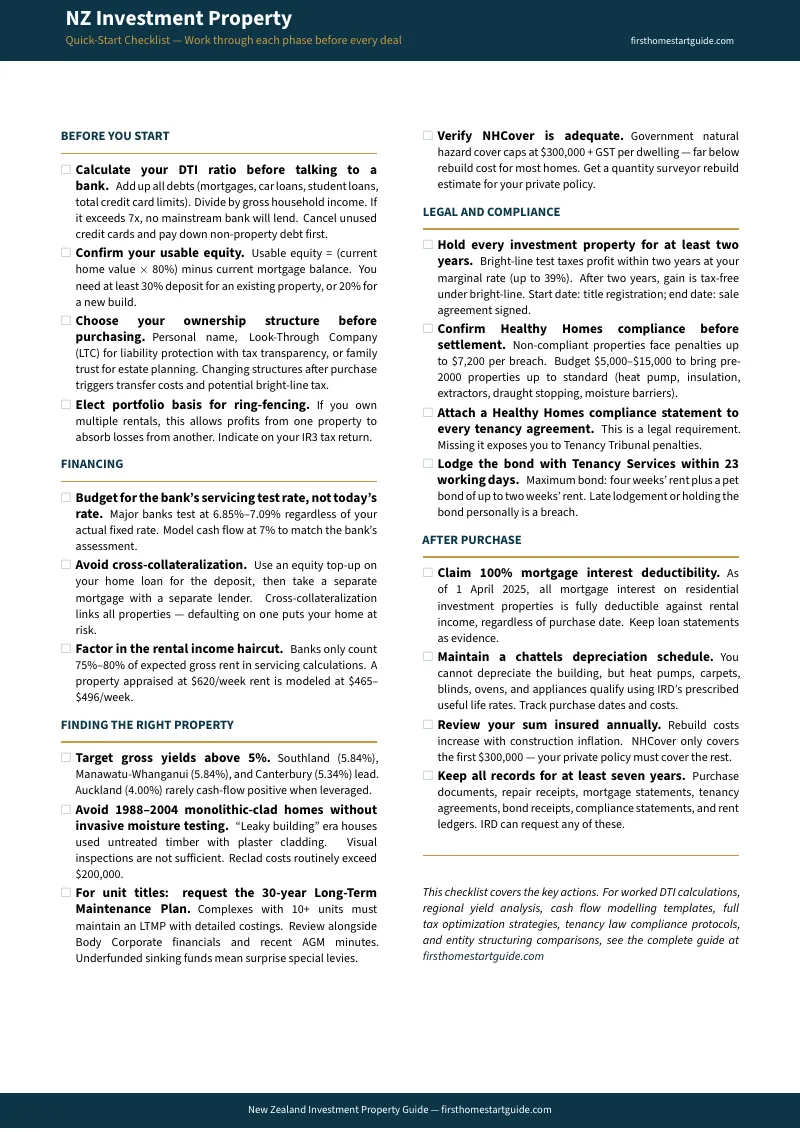

Then the DTI calculation kills the deal. Your existing mortgage is $620,000. You have a $15,000 car loan, a $12,000 student loan, and a credit card with a $10,000 limit you never use. Your household gross income is $160,000. Total current debt: $657,000. DTI ratio: 4.1x — comfortable. But add the new $487,500 mortgage (75% of $650,000) and your total debt hits $1,144,500. New DTI: 7.15x. The bank says no — the RBNZ caps investor lending at 7x. You need either $14,500 more gross income or a smaller loan. And that unused credit card you forgot about? The bank counted the full $10,000 limit, not the zero balance. Cancel it, and your DTI drops to 7.09x. Still over. The deal is dead unless you find a property that adds enough rental income to the denominator to pull the ratio below the cap.

This is the paradox of the 2026 New Zealand property market: the government gave you back every tax lever — 100% interest deductibility, a two-year bright-line, restored no-cause terminations — and then the Reserve Bank erected a credit wall that makes it mathematically impossible to use those levers unless you understand DTI arithmetic, LVR extraction mechanics, and high-yield regional targeting at a level most investors have never needed before. Free tools from IRD will confirm the deductibility rules. Mortgage broker content from Squirrel and Mortgage Lab will explain how equity release works. Opes Partners will tell you to buy a new build through their platform. None of them will show you how to simultaneously solve the DTI equation, optimise the tax position, comply with Healthy Homes and the 2024 Tenancy Act, and build a portfolio that survives a servicing test at 7%.

The New Zealand Investment Property Guide is a DTI-Era Investor Compliance System — not a motivational overview of property investment, but a structured framework that maps every regulatory constraint, tax rule, and credit restriction into a process you work through before you sign a sale and purchase agreement. It replaces months of cross-referencing IRD bulletins, RBNZ policy statements, Tenancy Services fact sheets, and conflicting PropertyTalk threads with a single reference that tells you exactly what the numbers should look like, exactly what the law requires, and exactly where deals collapse in this market.

What's Inside the DTI-Era Investor Compliance System

A 10-chapter guide, 5 standalone printable worksheets, and a 19-item due diligence checklist — covering every stage from DTI pre-qualification through post-purchase tax optimisation, built specifically for the regulatory complexity that makes investing in New Zealand in 2026 different from any year before it:

DTI and LVR Pre-Qualification Framework

The Reserve Bank's DTI restriction is the single most common deal-killer in New Zealand property investment right now. Most investors discover it when the bank declines them — not before. The guide walks through the exact DTI calculation: total debt (mortgages, car loans, student loans, and full credit card limits — not balances) divided by gross household income including projected rental income at the bank's 75–80% haircut rate. You model your ratio before talking to a lender, identify what to eliminate (that unused credit card limit counts), and calculate exactly how much rental income a target property must generate to keep you below the 7x cap. Combined with LVR analysis — 30% deposit for existing properties, 20% for new builds, and the December 2025 easing that gives banks 10% headroom on the investor threshold — you know your maximum purchase price before you start searching.

Tax Optimisation Under 100% Deductibility and Ring-Fencing

The restoration of full interest deductibility from 1 April 2025 is the most significant positive tax change for investors in a decade. But ring-fencing is still in force — your rental losses cannot offset your PAYE salary. High-income professionals on the 39% marginal rate routinely assume the old negative gearing playbook is back. It is not. The guide explains exactly how ring-fencing works, why the "portfolio basis" election is the single most powerful structural tool available to multi-property owners (it lets profits from a high-yield property absorb losses from a newly leveraged one), and how to calculate your net tax position across properties rather than property-by-property. It also covers the bright-line test at its current two-year threshold: start date is title registration, end date is signing the sale and purchase agreement, main home exclusion requires more than 50% use by area and time, and the transitional rules that apply to properties purchased between 2021 and 2024 when the old 10-year rule was in force.

Regional Yield Analysis for DTI-Compliant Portfolio Building

Under DTI restrictions, the old strategy of buying low-yield Auckland properties and waiting for capital gains is no longer viable — a property yielding 3.95% gross actively degrades your borrowing capacity for every subsequent purchase. The guide provides region-by-region yield data (Southland at 5.84%, Manawatu-Whanganui at 5.84%, Canterbury at 5.34%) and explains how to evaluate regional markets not just for rental return but for DTI impact — because the property that maximises your gross rental income per dollar of debt is the one that unlocks your next purchase. This is the mathematics of portfolio scaling under credit rationing, not speculation.

Healthy Homes and 2024 Tenancy Act Compliance

The July 2025 compliance deadline has passed. Every private rental in New Zealand must now meet the Healthy Homes Standards — specific quantified requirements for heating, insulation, ventilation, moisture, and draught stopping. Non-compliance carries penalties up to $7,200 per breach. The guide provides a compliance assessment framework so you can estimate remediation costs ($5,000–$15,000 for pre-2000 properties) before you buy, not after. It also covers the 2024 Tenancy Act amendments: the reinstated 90-day no-cause termination for periodic tenancies, the new pet bond (up to two weeks' rent, separate from the standard four-week bond), retaliatory termination protections with a 12-month enforcement window, and the simplified fixed-term expiry notice requirements.

Entity Structuring and Ownership Strategy

Personal name, Look-Through Company, or family trust — each structure has different implications for liability, tax, bright-line exposure, and portfolio transferability. Changing structures after purchase triggers a deemed disposal that can activate the bright-line test and incur transfer costs. The guide compares all three against the specific scenarios that NZ investors face: a married couple buying their first rental, a portfolio builder adding a fifth property, a high-income professional seeking liability protection. You decide before you sign, not after your accountant tells you it is too late.

Sale and Purchase Agreement, Due Diligence, and Settlement

NZ property transactions run through solicitors or licensed conveyancers using the Torrens title system and Landonline electronic transfer. The guide covers the full legal process: engaging a solicitor ($1,500–$3,000 for standard residential conveyancing), ordering the LIM report from council, commissioning a building inspection (critical for 1988–2004 monolithic-clad homes — the "leaky building" era where visual inspections are insufficient and reclad costs routinely exceed $200,000), investigating the title for restrictive covenants and easements, and structuring conditions that protect your position at auction, tender, and private treaty. For unit titles: how to read the 30-year Long-Term Maintenance Plan, what underfunded sinking funds mean for special levies, and what the Body Corporate disclosure documents should tell you before you commit.

Who This Guide Is For

This guide is for property investors operating in New Zealand's 2026 regulatory environment who:

- Have usable equity in their home and want to buy their first investment property — but need to understand how the DTI cap, LVR deposit requirements, and the bank's servicing test rate interact before they can determine what they can actually afford

- Own one to three rentals and paused acquisitions between 2021 and 2024 when interest deductibility was stripped away — and now need to recalculate their portfolio economics under 100% deductibility, model the DTI impact of their existing debt, and identify high-yield regions that won't degrade their borrowing capacity

- Earn above $180,000 and assumed that restored interest deductibility means negative gearing is back — and need to understand that ring-fencing still quarantines rental losses from PAYE income, that the portfolio basis election is the only legal mechanism for cross-property loss absorption, and that entity structuring decisions are irreversible after purchase

- Purchased a property between 2021 and 2024 under the 10-year bright-line and now want to sell — and need to confirm that the July 2024 rollback to two years applies retroactively, understand the exact start and end date mechanics, and verify whether the main home exclusion applies based on the 50% area-and-time threshold

- Are evaluating an older property and need to calculate the Healthy Homes remediation cost before settlement — not discover a $12,000 heat pump, insulation, and ventilation bill after they have already signed unconditional

- Want every NZ-specific regulation, tax calculation, credit restriction, and tenancy compliance requirement in one reference — instead of assembling it from IRD technical bulletins, RBNZ policy statements, MBIE Tenancy Services guides, PropertyTalk threads, and Opes Partners content that steers you toward their new-build inventory

Why Not Free Tools and Forums?

Free information on New Zealand property investment exists across dozens of sources. Here is what it actually delivers:

- IRD's property interest limitation rules page confirms that 100% deductibility is restored from 1 April 2025. It does not explain how to use the portfolio basis election to offset losses across properties, does not model how deductibility interacts with your DTI calculation, and does not warn that ring-fencing still prevents you from reducing your PAYE tax bill. You get the rule without the strategy.

- Opes Partners and the Property Academy Podcast produce high-quality, data-rich content and proprietary ROI calculators. Their business model is selling off-the-plan new builds to retail investors through a buyer's agency. Their content systematically favours new builds, underplays developer margin premiums, and does not cover the value-add potential of renovating existing housing stock — because that is not what they sell. Their yield data is excellent; their strategic framing is a sales funnel.

- Mortgage broker content (Squirrel, Mortgage Lab) will explain equity release mechanics and LVR requirements clearly. They stop at the border of tax strategy, regional yield analysis, tenancy compliance, and entity structuring — because those are outside their expertise and licensing. You get the financing step without the framework that determines whether financing is the right step.

- Reddit's r/PersonalFinanceNZ and PropertyTalk forums contain genuine experience from real NZ investors — mixed with outdated advice about interest deductibility phasing, bright-line scenarios that predate the July 2024 rollback, and DTI calculations that confuse credit card limits with balances. The default response to any complex question is "talk to your accountant at $200+/hour." Sorting current from outdated across a dozen threads costs more time than reading a guide that has already verified every figure against current legislation.

This guide fills the NZ-specific gap — the space between knowing that you want to invest in property and knowing how to actually structure, finance, comply with, and optimise an investment under the specific regulatory regime that exists right now. The DTI calculation, the ring-fencing portfolio basis election, the bright-line transitional rules, the Healthy Homes remediation budget, the pet bond mechanics, the leaky building risk assessment — these are not generic concepts. They are NZ-only constraints, and getting any one of them wrong costs more than this guide ever will.

— Less Than One Hour With Your Accountant

A single DTI miscalculation that includes an unused credit card limit you forgot to cancel costs you the deal entirely. One incorrect bright-line start date assumption turns a tax-free sale into a bill at your 39% marginal rate. A Healthy Homes non-compliance penalty runs up to $7,200 per breach. A cross-collateralisation structure you did not need to agree to puts your family home at risk if the investment property underperforms. A low-yield Auckland property that satisfies your instinct for familiar suburbs actively blocks your ability to borrow for the next purchase under DTI.

This guide does not replace your solicitor or your chartered accountant. But it gives you the DTI pre-qualification framework, tax optimisation strategy, compliance system, and regional yield analysis that ensure you identify every NZ-specific risk before you sign unconditional — instead of discovering them on your first declined mortgage application, your first unexpected tax bill, or your first Tenancy Tribunal penalty.

If it catches a single DTI miscalculation, prevents a single bright-line error, or saves you from buying a non-compliant property without budgeting for remediation, it pays for itself before you have finished reading it.

30-day money-back guarantee. If the guide does not sharpen your due diligence and protect your capital in New Zealand's current regulatory environment, you pay nothing.

Download the free New Zealand Quick-Start Checklist to see the 19-item due diligence framework covering DTI pre-qualification, equity extraction, financing structure, property selection, legal compliance, tax optimisation, and tenancy management. When you are ready for the full DTI modelling, regional yield analysis, tax strategy, and 10-chapter investment guide, the complete guide is here.

The numbers work on the spreadsheet. This guide tells you whether the Reserve Bank, the IRD, and the Tenancy Tribunal agree.