You Have Spent 40 Hours Researching HDB Flats. You Still Cannot Answer the One Question That Determines Whether You Are Buying Smart or Buying Blind.

How much cash will you actually walk away with when you sell this flat in ten years — after CPF accrued interest, after the subsidy clawback, after the income ceiling restriction narrows your buyer pool?

You can quote the Enhanced CPF Housing Grant cap. You have read the income ceiling is S$14,000. You know the BTO wait is four to five years. But you cannot connect these facts into a single financial picture. You cannot calculate whether deploying S$200,000 from your CPF Ordinary Account today will cost you S$56,700 in accrued interest at exit — or whether a Voluntary Housing Refund strategy neutralises that cost entirely. You cannot determine whether a Plus flat's 6% subsidy clawback and 10-year MOP make it a worse investment than a Standard flat in a less central location. You cannot model whether paying S$70,000 in Cash Over Valuation today for a resale flat outperforms waiting five years for a BTO when rent during the wait costs you S$150,000.

The fragments exist — HDB InfoWEB for eligibility rules, CPF Board for withdrawal limits, PropertyGuru for listings, StackedHomes for COV data, r/singaporefi for CPF debates. But nobody has built a single model that feeds your income, your CPF balance, and your target location through the full chain: grant stacking → loan quantum → stamp duty → COV buffer → CPF deployment → accrued interest projection → MOP restrictions → exit scenario. Until you run that chain, you are making a S$500,000 to S$800,000 decision on partial information.

The Singapore First-Time Home Buyer Guide is an HDB Financial Decision System — a structured walkthrough that translates every interlocking HDB policy, CPF rule, and stamp duty calculation into worked dollar-amount examples calibrated to actual 2026 income brackets and property prices. It replaces the cross-referencing between government portals, financial blogs, and Reddit threads with a single reference that tells you your real grant quantum after income tiering, your true cost of using CPF after compounding, your actual cash requirement for a resale purchase including COV, and your projected exit position under each classification tier.

What Is Inside the HDB Financial Decision System

A comprehensive guide and a quick-start checklist — covering every stage from HFE letter application through key collection, built specifically for the regulatory structures and market dynamics that make buying in Singapore unlike any other country:

The BTO vs Resale Financial Model

Not a pros-and-cons list — a side-by-side cost comparison with actual numbers. The guide calculates total cost of the BTO path (subsidised price + rent during the four-to-six-year wait + CPF growth foregone) against total cost of the resale path (market price + COV + immediate occupancy). It factors in the subsidy quantum for Standard, Plus, and Prime flats, models CPF Ordinary Account opportunity cost during the waiting period, and includes a breakeven framework showing at what rental cost and waiting duration the BTO advantage disappears for your income bracket. If you are paying S$2,500 a month in rent, five years of waiting costs S$150,000 before you have touched the flat — and the guide shows you exactly when that cost exceeds the BTO discount.

Standard, Plus, and Prime — The Exit Strategy That Changes Everything

The October 2024 reclassification replaced the old mature vs non-mature system with three tiers that have fundamentally different financial outcomes. Standard flats: 5-year MOP, whole-flat rental allowed, no clawback. Plus flats: 10-year MOP, permanent whole-flat rental prohibition, 6% subsidy clawback on resale price, income ceiling restriction on your future buyer. Prime flats: 10-year MOP, 9% clawback, same buyer restrictions. The guide includes a worked Internal Rate of Return comparison showing projected returns over 15 and 20-year holding periods — because a Prime flat purchased in 2026 with a five-year build and ten-year MOP cannot be sold until approximately 2041, and the clawback plus restricted buyer pool may make the return lower than a Standard flat in a less central location.

CPF Accrued Interest — The Compound Cost Nobody Calculates Until It Is Too Late

When you use CPF to fund your downpayment or service your mortgage, you owe the principal plus 2.5% annual compound interest back to your CPF upon sale. This is not a tax — it returns to your own retirement account. But it directly reduces the cash you walk away with. The guide provides full compounding tables: S$100,000 withdrawn for five years accumulates S$13,280 in accrued interest. S$200,000 for ten years: S$56,738. S$500,000 for ten years: S$141,845. Then it walks you through the Voluntary Housing Refund (VHR) strategy — manually refunding cash to CPF early to stop the interest clock, effectively converting your CPF OA into a risk-free 2.5% savings vehicle while eliminating the accrued interest burden at exit.

Grant Stacking — Your Real Numbers, Not the S$230,000 Headline

The theoretical maximum grant stack (S$120K EHG + S$80K Family Grant + S$30K PHG) requires a household income of S$1,500 or less — which simultaneously disqualifies you from borrowing enough to afford the flat. For a couple earning S$9,000 per month, the EHG is S$0. At S$7,000, it is approximately S$25,000. At S$5,000, it is S$75,000. The guide includes an income-tiered table at every S$500 bracket from S$1,500 to S$14,000, showing your actual EHG quantum, your CPF Housing Grant for resale, and your Proximity Housing Grant (S$30,000 to live with parents, S$20,000 within 4km) — so you budget around the grant you will actually receive, not the number in the headline.

The HFE Letter — Application, Timeline, and the Traps That Kill Your Loan Quantum

The HDB Flat Eligibility letter is the hard prerequisite for every BTO application and every resale OTP. Processing officially takes 21 working days. In practice, it stretches to six to eight weeks before major BTO launches. The guide details the exact document requirements: 15 months of payslips, 14 months of CPF contribution history, IRAS Notices of Assessment, Credit Bureau reports. For self-employed and commission-based workers: the 30% income haircut, the continuous employment proof requirements, and how to structure your documentation to avoid algorithmic rejection. The single biggest trap — a minor credit card missed payment can suppress your approved HDB loan quantum by more than S$200,000 without explanation.

HDB Loan vs Bank Loan — The Full 25-Year Comparison

HDB concessionary rate at 2.6% vs current bank floating rates at 3.5-4.0%. Both offer 75% LTV since 2024. The MSR cap (30% of gross monthly income) governs both. The guide provides a 25-year amortisation comparison for a S$400,000 loan, showing total interest paid under each option and the year-by-year cash flow difference. The flexibility trade-off: HDB loans have no early repayment penalty and no lock-in period; bank loans offer promotional rates for the first two to three years but revert to board rates. The guide models what happens when your bank rate rises from 2.6% to 4.0% after the promotional period expires.

Cash Over Valuation — The Cash Drain the Statistics Understate

Official data says the median COV is near S$0 and only one in three resale buyers pay it. Ground-level reality in mature estates (Tiong Bahru, Bishan, Clementi) runs S$50,000 to S$120,000 routinely. The guide covers COV trends by estate maturity and flat type, negotiation tactics using comparable transaction data, timing strategies around low-demand periods, and the cash flow impact — COV must be paid entirely in cash, not CPF, not loan. If you budgeted S$100,000 for renovation and S$80,000 of that goes to COV, your interior plans just collapsed.

Buyer's Stamp Duty and the Full Upfront Cash Requirement

BSD is tiered: 1% on the first S$180K, 2% on the next S$180K, 3% on the next S$640K. On a S$700,000 resale flat, that is S$15,600. The guide provides worked BSD calculations for S$500K, S$700K, and S$1M purchase prices, then maps the complete upfront cash requirement: option fee (S$1,000-S$5,000), exercise fee, BSD, valuation fee, agent commission (typically 1%), legal conveyancing fees (S$2,000-S$3,500), and the COV buffer. A complete picture of what you must have in cash on specific dates — not just a formula.

ABSD and the Upgrade Path

If you plan to hold your HDB and buy a private condo, you will pay 20% Additional Buyer's Stamp Duty on the condo — S$300,000 on a S$1.5M property. The decoupling strategy (transferring your HDB share to your spouse) is now illegal except for divorce, death, or bankruptcy. The guide walks through the sell-then-buy sequence: the ABSD remission window (sell within six months), the financial stress of temporary housing, the timing risk if the HDB sale completes before the condo purchase or vice versa, and whether the upgrade path is financially viable at your income level.

MOP Rules — What You Can and Cannot Do for Five to Ten Years

Standard flats: 5-year MOP. Plus and Prime: 10-year MOP. During MOP, you must physically reside in the flat. Bedroom rental is allowed with HDB approval. Whole-flat rental is prohibited for all during MOP and permanently prohibited for Plus and Prime. You cannot buy local or overseas private residential property during MOP. Overseas postings require HDB approval. Non-occupation can result in financial penalties or compulsory acquisition. The guide provides the definitive rules for every MOP scenario, including the EC timeline (5-year MOP → restricted resale → full privatisation at year 10).

Financial Planning Worksheets

CPF deployment calculator (how much OA to use vs retain for retirement), monthly mortgage affordability calculator calibrated to MSR and TDSR limits, total cost of ownership model (mortgage + maintenance + property tax + sinking fund + renovation amortisation), and a five-year cash flow projection showing how your finances evolve from purchase through MOP completion.

9 Standalone Printable Worksheets and Reference Cards

Every major tool in the guide is also extracted as a standalone PDF you can print, fill in, and bring to your HDB appointment or financial planning session — without flipping through the full guide:

- Grant stacking income-tiered reference table

- CPF accrued interest compounding tables with VHR strategy

- BTO vs resale fillable comparison worksheet

- Standard / Plus / Prime classification reference card

- HFE letter document preparation checklist

- Upfront cash requirement worksheet (BSD + COV + fees)

- ABSD upgrade path calculator

- Complete purchase timeline (BTO and resale paths)

- Financial planning worksheets (CPF deployment, mortgage affordability, total cost of ownership, cash flow projection)

Who This Guide Is For

- Couples earning S$7,000 to S$14,000 combined who are balloting for BTOs or evaluating resale flats, need to know their actual grant quantum after income tiering, must decide between deploying CPF or preserving it against accrued interest, and cannot find a single resource that models the full financial chain from grant eligibility to exit scenario

- Singles aged 35 and above who now qualify for 2-room Flexi BTOs in Plus and Prime locations, need to calculate whether their single-income MSR cap gives them enough loan quantum for these units, and want to understand how the 10-year MOP and rental restrictions affect their financial flexibility for the next fifteen years

- BTO ballot veterans who have failed two or three rounds and are pivoting to the resale market under emotional pressure, but have not recalculated their financial position for a market-price purchase with COV, larger BSD outlay, and different grant eligibility

- Self-employed and commission-based workers who face income documentation challenges with the HFE letter, risk algorithmic suppression of their loan quantum, and need to understand the 30% income haircut and how to structure their documentation to avoid rejection

- Upgraders planning the HDB-to-condo transition who need to understand the ABSD mathematics, the sell-then-buy sequence, the six-month remission window, and why decoupling is no longer available — before committing to a private property purchase that may not be financially feasible

Why Not Free Tools and Forums?

- The HDB InfoWEB and CPF Board portals give you the rules in legally precise bureaucratic language spread across dozens of interlocking sub-pages. They tell you the EHG exists and that the maximum is S$120,000. They do not tell you that at S$9,000 household income your EHG is S$0, that the income tiering formula reduces the grant by S$5,000 to S$10,000 per S$500 income bracket, or how your grant quantum interacts with your mortgage ceiling and CPF deployment strategy. You get eligibility inputs without a decision framework.

- PropertyGuru and 99.co dominate search results with "Singapore first time buyer guide" articles designed to generate listing enquiries. They cover the BTO application process and stamp duty basics but do not model CPF accrued interest over ten years, do not calculate the real IRR on Plus vs Standard flats, and do not address the specific cash flow problem of COV eating into your renovation budget. You get content marketing, not financial analysis.

- r/singaporefi and HardwareZone contain genuine financial modelling from sophisticated buyers — CPF OA optimisation debates, IRR calculations on Prime BTOs, crowdsourced HFE processing timelines. But they are buried in threads that contradict each other, mix 2023 rules with 2026 rules, and require you to read fifty posts to extract the three that apply to your situation. Sorting current from outdated takes longer than reading a guide that already reconciled the rules.

- Mortgage broker consultations are free because the broker earns commission from your loan. They will calculate your borrowing power accurately but will not model the CPF accrued interest implications of maximising your CPF deployment, will not advise you on whether a Standard flat yields a better 15-year return than a Plus flat, and will not tell you whether paying COV today outperforms waiting for a BTO. Their incentive is to close a transaction, not to optimise your financial outcome.

This guide fills the Singapore-specific gap — the space between knowing HDB's rules exist and knowing how they interact to determine your actual financial outcome. It is the analysis that would take a housing finance counsellor, a CPF specialist, and a property analyst to assemble: the grant stacking calculation, the CPF deployment model, the COV negotiation framework, the stamp duty worksheet, and the exit scenario projection — structured as a single reference you own permanently.

— Less Than One HFE Letter Processing Fee

A single property agent engagement runs S$5,000 to S$8,000 in commission on a S$600,000 flat. A mortgage broker consultation is free but optimised for their commission, not your CPF strategy. A Year-Two COV miscalculation can cost you S$50,000 to S$80,000 in cash you did not budget. Choosing maximum CPF deployment without modelling accrued interest can erode S$50,000 or more from your exit proceeds over ten years. Missing one grant tier because you did not check the income bracket table could mean leaving S$20,000 to S$30,000 in subsidies unclaimed.

This guide does not replace your property agent, your mortgage broker, or your conveyancing lawyer. But it gives you the financial modelling, grant calculation, CPF strategy, and exit scenario analysis that ensure you are making a S$500,000 to S$800,000 decision with a complete picture — instead of assembling it from government portals and forum threads while your HFE letter processing clock ticks down.

If it catches a single grant miscalculation, prevents a single CPF deployment error, flags a single COV negotiation gap, or maps a single exit scenario you had not modelled, it pays for itself before you finish reading it.

30-day money-back guarantee. If the guide does not sharpen your HDB buying analysis and protect your financial position, you pay nothing.

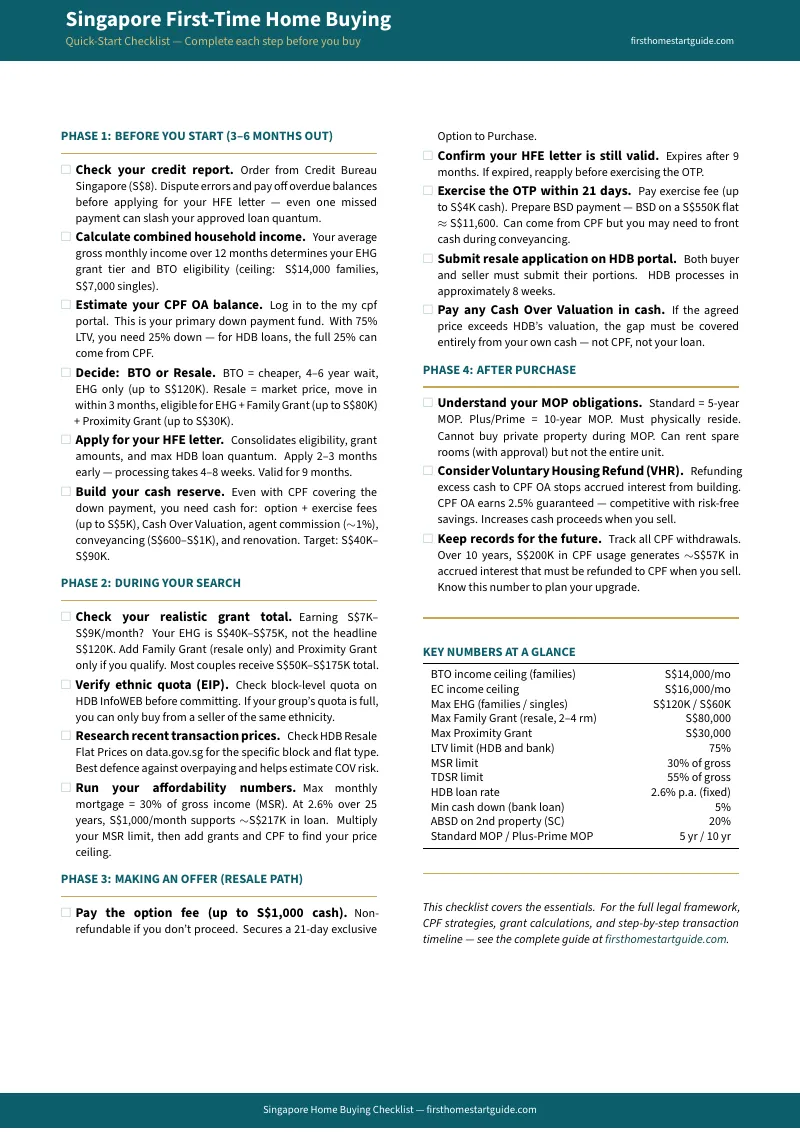

Download the free Singapore Quick-Start Home Buying Checklist to see the step-by-step framework covering HFE application, grant eligibility, CPF deployment, BTO ballot, resale viewings, and upfront cash requirements. When you are ready for the full CPF accrued interest tables, grant stacking worksheets, BTO vs resale financial model, and the complete guide with worked examples at every income bracket, the full toolkit is here.

Singapore rewards buyers who understand how the system works. This guide makes sure you do.