Your Agent Says "Good Investment." Your ABSD Bill Says S$300,000.

You already own property. You understand capital appreciation, rental yields, and the difference between freehold and 99-year leasehold. You are not looking for a beginner's guide to buying a condo. You are looking for an honest answer to the question that every agent, every bank seminar, and every developer showflat carefully avoids: does the math actually work?

Because the math in Singapore is unlike any other property market. A Singapore Citizen buying a second residential property at S$1,500,000 pays S$300,000 in Additional Buyer's Stamp Duty alone. Add Buyer's Stamp Duty and you are looking at S$344,600 in transaction taxes before you turn a single key. With a 45% LTV limit on a second mortgage, you need approximately S$1,170,000 in upfront capital. To recover the ABSD through rental yields at 3% net, you are looking at 12 to 15 years of uninterrupted tenancy just to break even on the tax.

That S$300,000 is the number that changes everything. And it is the number that commission-driven sources have no structural incentive to help you scrutinize.

The agent earns commission on the sale. The bank earns interest on the mortgage. The developer needs to move units before their own five-year ABSD deadline. PropNex runs expos. ERA runs masterclasses. Stacked Homes runs affiliate models. None of them publish the worked calculation showing what 20% ABSD does to your 10-year return. None of them model the CPF accrued interest trap that adds S$50,000 to S$100,000 to your decoupling costs. None of them compare the recovery timeline of paying ABSD against selling your HDB and executing a decoupled purchase at 0%.

The ABSD Decision Engine exists because you should not need a S$5,000 fee-only wealth planner to run the numbers that every property investor in Singapore needs to see. The Singapore Investment Property Guide is an objective, math-heavy playbook that covers ABSD scenarios, decoupling mechanics, TDSR and LTV constraints, HDB subletting rules, leasehold decay analysis, en bloc realities, rental yield calculations, S-REIT comparisons, and exit strategies. Every rate, every threshold, and every worked example uses 2026 figures. The recommendations follow the numbers, not a commission structure.

What's Inside the ABSD Decision Engine

A 13-chapter guide, 8 standalone worksheets and reference cards, and the worked calculations that no commission-driven source will publish. 10 PDFs total. Each chapter addresses a specific structural problem that Singapore property investors face. Not generic investment theory. Current regulations, real numbers, and scenarios you can apply to your own situation this week. Print the worksheets, fill in your numbers, and know exactly where you stand before any agent meeting or showflat visit.

The Full ABSD Landscape with Worked Recovery Math

Every ABSD rate for every buyer profile: SC, SPR, foreigner, entity, trustee, developer. But rates alone are useless without context. This chapter models the actual recovery timeline: how long it takes to earn back S$300,000 in ABSD through rental yields at various net yield assumptions, and why most independent financial planners advise against simply absorbing the tax. Includes the married couple ABSD remission rules, the six-month sell-by deadline that IRAS enforces without exception, and the developer five-year sell-all rule that creates purchasing windows for alert buyers.

Decoupling Mechanics: The Legal Pathway and the IRAS Crackdown

Step-by-step decoupling for private condos: Part-Purchase agreements, BSD on transferred shares, separate legal counsel requirements, and mortgage refinancing. The CPF accrued interest trap that adds tens of thousands to your costs if you used CPF for the original purchase. Why HDB decoupling has been banned since May 2016 and there are no workarounds. And the 99-to-1 crackdown: how IRAS audited 187 cases, found tax avoidance in 166, clawed back over S$60 million, and secured criminal convictions including imprisonment. The line between legitimate tax planning and prosecutable avoidance, explained with case references.

TDSR and LTV: How Much You Can Actually Borrow

The 55% TDSR cap stress-tested at 4.0% to 4.8%. The 30% haircut on variable and rental income. Financial asset monetization for asset-rich, income-lean investors. LTV limits by outstanding loan count (75% / 45% / 35%), and the further tightening for tenures exceeding 30 years or age 65. A full worked example: financing a S$1,500,000 investment property on S$15,000 gross monthly income with one existing mortgage. The total upfront capital figure that most buyers do not calculate until it is too late.

HDB Subletting Rules for MOP Completers

The complete regulatory framework for renting out your HDB flat: who can sublet (SCs only for whole-flat, SPRs are permanently barred), the Plus and Prime BTO whole-flat subletting ban (permanent, no exceptions), tenant eligibility, the Non-Citizen Quota (8% neighborhood / 11% block), lease duration limits, maximum occupancy by flat type, and the HDB portal registration process. If you are keeping your HDB and buying private, this chapter tells you exactly what you can and cannot do with the flat.

Leasehold Decay Analysis with District Case Studies

Why younger leasehold projects (lease start 2015+) achieved 6.48% annualized growth while older projects (1985-1994) achieved only 3.44% over the same period. The CPF pro-ration formula that shrinks your buyer pool as remaining lease declines. The Balas Curve inflection point. Case studies: Gardenvista in District 21 outperforming regional averages, and the Jurong East remaining-lease index shift where post-pandemic demand temporarily offset decay. The balance lease thresholds where banks reduce LTV and CPF restricts funding.

En Bloc Realities: Why Speculating on Collective Sales Is a Trap

Total collective sale values collapsed to S$22 million in 2025, less than 1% of the 2007 peak. Zero collective sales in 2024. Only two succeeded in 2025, both small freehold projects. The 80% / 90% consent thresholds. Developer ABSD constraints that make site acquisitions uneconomical. And the sinking fund depletion problem: when developments enter active en bloc discussions, maintenance spending halts. When 95% of attempts fail, owners are left in deteriorating buildings with thin reserves and rising levies.

Rental Yields by District and Property Type

Gross vs. net yield formulas. URA transacted rental data vs. asking rents. Vacancy rates by district. The property tax tiers for non-owner-occupied residential (12% to 36% on Annual Value). Rental income tax treatment at your marginal rate. The complete cost stack that turns an advertised 4% gross yield into a 2.5% net yield after tax, vacancy, maintenance, and management.

S-REITs vs. Direct Property: The Comparison Nobody Publishes

Because every agent who earns commission on a S$1.5M transaction has zero incentive to tell you that a diversified S-REIT portfolio historically delivers comparable total returns with no ABSD, no TDSR constraint, no tenant management, and daily liquidity. This chapter presents both sides: the leverage advantage and forced savings mechanism of direct ownership, and the liquidity, diversification, and tax efficiency of REITs. With numbers, not opinions.

Who This Guide Is For

- HDB MOP completers deciding whether to sell, sublet, or hold their flat while buying private property, and who need to model every scenario with real numbers before committing

- Singapore Citizens buying a second property who want an objective breakdown of whether paying 20% ABSD or executing a decoupled purchase makes more financial sense for their specific situation

- Private property owners expanding their portfolio who need to understand third-property ABSD rates, LTV limits on subsequent loans, and how rental income haircuts affect their borrowing capacity

- SPR investors navigating the 30% ABSD on a second property and the permanent prohibition on whole-flat HDB subletting

- Couples evaluating decoupling who need the full cost breakdown: BSD on transferred shares, CPF accrued interest refund, legal fees, refinancing, and the IRAS red lines they cannot cross

This guide is not for:

- First-time home buyers looking for BTO or resale HDB guidance (see our Singapore First Home Guide)

- Anyone looking for "secret" property strategies or get-rich-quick playbooks. This is a technical reference, not a seminar pitch

Why Free Resources Are Not Enough

Stacked Homes, 99.co, and PropertyGuru publish excellent editorial content. But none of them publish the ABSD recovery model. They will tell you the ABSD rate is 20%. They will not model how long it takes to recover that S$300,000 through rental income at various yield assumptions, or show you the side-by-side comparison of paying ABSD vs. selling and buying two properties at 0% ABSD. Their revenue models depend on developer advertising and agency affiliate partnerships. The analysis that might steer you away from a purchase is the analysis that does not get published.

Bank seminars exist to originate mortgages. DBS, OCBC, and UOB home loan events will explain SORA rates and refinancing options in detail. They will not tell you whether you should be borrowing at all. A bank earns interest on the loan it approves. It has no incentive to suggest that your S$1,170,000 in upfront capital might generate better risk-adjusted returns in a diversified S-REIT portfolio.

Developer showflats and agency expos exist to drive transactions. PropNex expos and ERA masterclasses provide access to data platforms and new launch schedules. But their entire business model depends on you signing an Option to Purchase. The scenarios where doing nothing is the optimal financial decision will never appear in their presentation deck.

Fee-only wealth planners charge S$2,000 to S$10,000 for a consultation. They provide genuinely independent advice, but the cost makes them inaccessible to most HDB upgraders. This guide delivers the same objective, math-first analysis at a fraction of that fee.

Satisfaction Guarantee

If the guide does not help you make a better-informed investment decision, email us and we will refund your purchase. No complicated process. The numbers speak for themselves.

Start with the Free Checklist

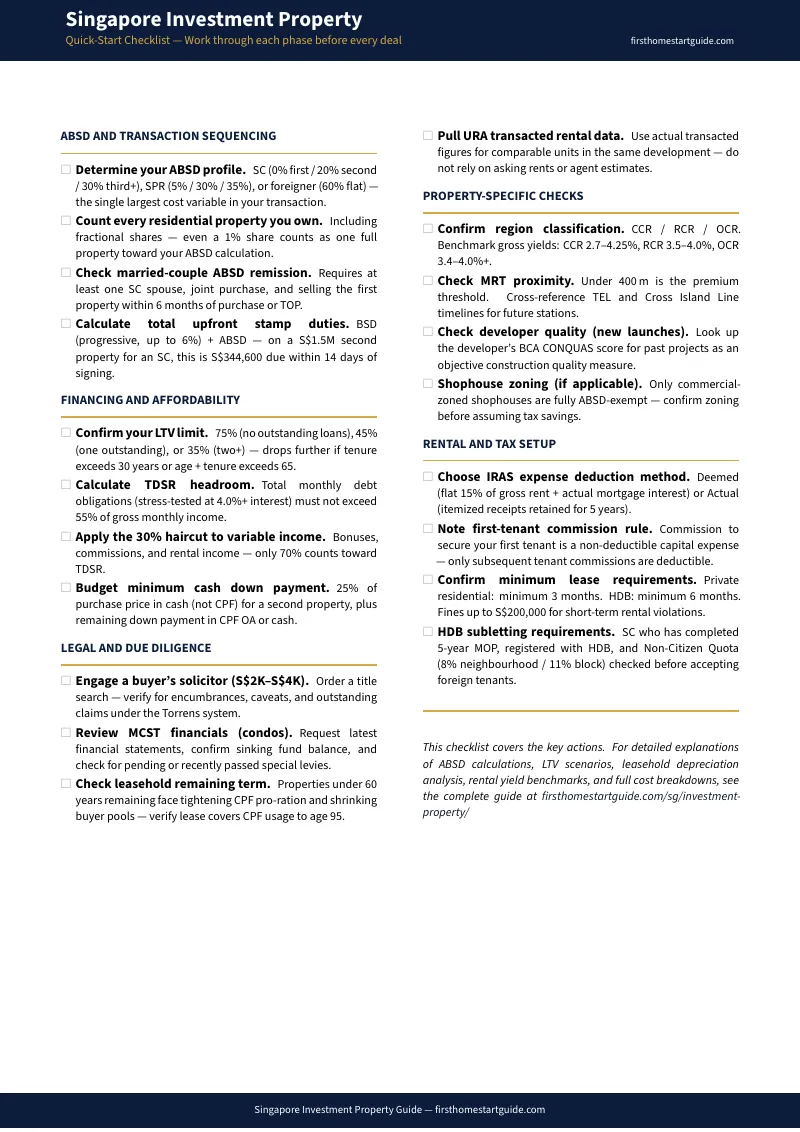

Download the Singapore Investment Property Quick-Start Checklist free — a step-by-step verification list covering ABSD calculations, TDSR and LTV checks, legal due diligence, leasehold analysis, and rental yield validation. Print it and bring it to every property viewing.

Or get the full toolkit — 13 chapters, 8 standalone worksheets and reference cards, and every worked calculation you need to make an informed investment decision — all for .