The Attorney Sitting Across From You at Closing Does Not Represent You.

Your offer was accepted on a three-bedroom home in Gwinnett County for $375,000. Your agent congratulated you. Your lender sent a Loan Estimate. You noticed a line item called "recording fees" and assumed it covered the standard paperwork. Then the Closing Disclosure arrived three days before closing with a new, separate line item you had never seen: Intangible Recording Tax --- $1,050. You called your loan officer. She said it is a Georgia state tax on recording the mortgage --- $3.00 per $1,000 of the loan amount --- and it is always paid by the buyer. You asked why it was not on the original estimate. She said it was "included in the aggregate." You asked your real estate agent if the seller would split it. He said no --- by law, the intangible tax is a buyer cost. Non-negotiable.

Then you arrived at the closing table and met the attorney who would supervise the transaction. You assumed this attorney --- the one your lender selected, the one sitting in the room reviewing your documents --- was there to protect your interests. You asked about an unresolved repair from the inspection. The attorney said he could not advise you on that. You asked about the earnest money disbursement. He said his obligation was to the lender's closing instructions, not to you. You asked who was representing you. Nobody answered.

The problem is not that Georgia is expensive. The problem is that Georgia is a mandatory attorney-closing state where the attorney at your closing table represents the lender, not you --- and that is just the first of a series of state-specific mechanics that quietly transfer risk to first-time buyers who do not know the rules. An intangible recording tax of $3.00 per $1,000 on your mortgage amount that national lenders routinely omit from preliminary estimates. A GAR Purchase and Sale Agreement where submitting a repair request does not pause the due diligence clock --- and missing the deadline by one hour forfeits your right to terminate. A homestead exemption system so fragmented across 159 counties that missing a single April 1 filing deadline waives hundreds to thousands of dollars in property tax savings for the entire year. A termite letter requirement governed by the Georgia Structural Pest Control Commission that most out-of-state buyers have never heard of. And a Georgia Dream down payment program that offers up to $12,500 in free equity but adds weeks of dual underwriting that can kill your offer in a competitive market.

The Georgia First-Time Home Buyer Guide is an Attorney-State Navigation System --- a structured walkthrough of every Georgia-specific contract mechanic, tax, legal risk, assistance program, and environmental hazard that determines whether your home purchase protects your capital or quietly puts it at risk. It replaces months of cross-referencing the DCA website, county tax assessor portals, GAR contract bulletins, closing attorney blogs, and panicked Reddit threads about the intangible tax with a single reference that tells you exactly how much closing really costs, exactly who represents whom at the closing table, and exactly what Georgia transactions look like when they go wrong.

The complete guide, a quick-start checklist, and 8 standalone printable tools --- covering the mandatory attorney-closing system, intangible recording tax calculations, Georgia Dream and Invest Atlanta down payment programs, the GAR contract's due diligence mechanics, county-by-county homestead exemptions, termite letter requirements, crawl space moisture risks, FHA and VA loan limits by county, USDA eligibility across 97% of the state, and regional market intelligence across Atlanta, Savannah, Columbus, Augusta, and Macon. Ten printable files:

- guide.pdf --- The full 10-chapter guide

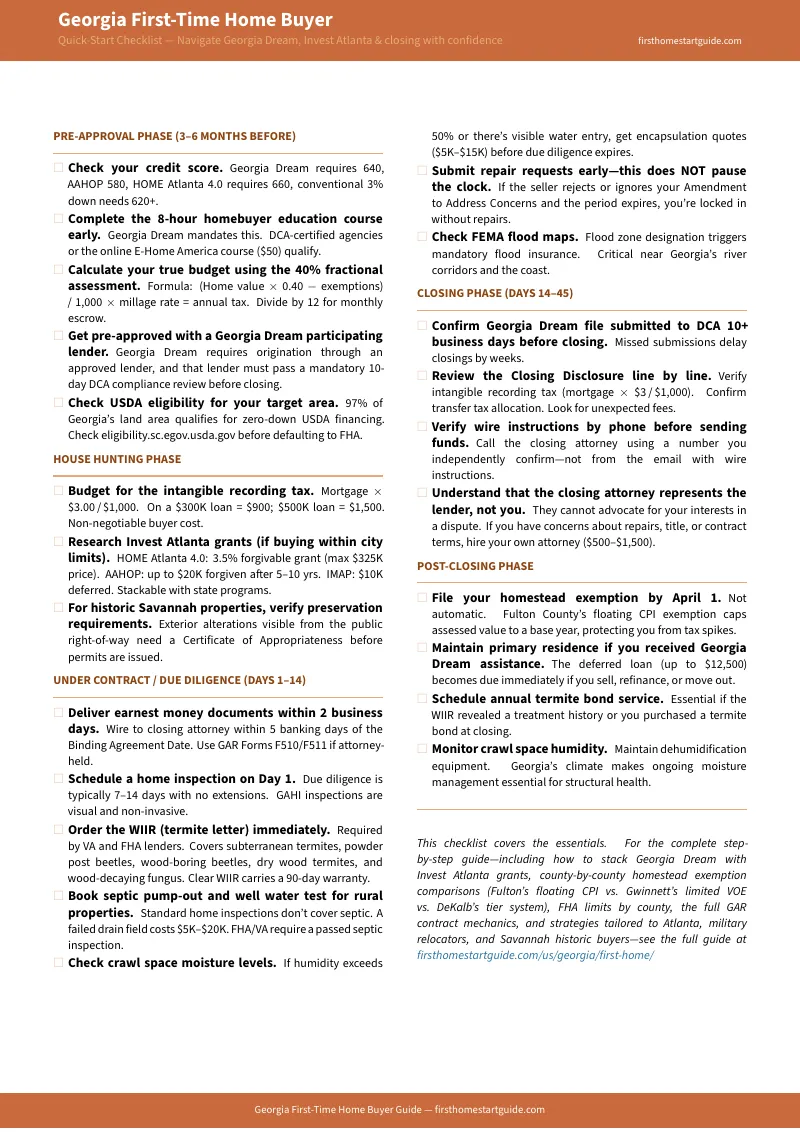

- checklist.pdf --- Quick-start home buying checklist

- closing-attorney-reference.pdf --- Who the closing attorney represents, when to hire your own, earnest money timelines

- dpa-worksheet.pdf --- Georgia Dream, Invest Atlanta, and municipal DPA programs with a fillable stacking calculator

- intangible-tax-calculator.pdf --- Tax formula, worked examples, transfer tax vs. intangible tax comparison

- homestead-exemption-reference.pdf --- Fulton, DeKalb, Cobb, and Gwinnett exemptions side by side with filing instructions

- financing-comparison.pdf --- FHA limits by county, loan program comparison, and USDA coverage notes

- inspection-checklist.pdf --- WIIR, crawl space, septic, well water, and due diligence items to bring to your inspection

- regional-market-reference.pdf --- Atlanta, Savannah, Columbus, Augusta, and Macon at a glance

- closing-timeline.pdf --- Your 30-to-45-day roadmap from offer to keys

What's Inside the Attorney-State Navigation System

A comprehensive 10-chapter guide with a quick-start checklist --- covering every stage from financial preparation through post-closing, built specifically for the contract mechanics, legal risks, assistance programs, and environmental realities that make Georgia fundamentally different from non-attorney-closing states:

The Closing Attorney Truth

Generic home buying guides tell you about title companies and escrow agents. In Georgia, neither exists. The Supreme Court of Georgia mandates that a licensed attorney must physically supervise every real estate closing --- telephonic or remote-only supervision is explicitly prohibited. The guide explains who the closing attorney actually represents (the lender), what they can and cannot do for you (explain documents, yes --- advocate for you in a dispute, no), the GAR forms that govern earnest money when the attorney holds it (F510 and F511), and exactly when you need to hire your own independent attorney ($500 to $1,500) to protect your interests. You get the fiduciary framework that prevents you from walking into the most expensive transaction of your life with no one in the room representing you.

The Intangible Recording Tax Decoded

This is Georgia's signature closing cost ambush. The intangible recording tax is levied at $1.50 per $500 (or $3.00 per $1,000) of your mortgage amount --- not the purchase price, the loan amount. On a $300,000 mortgage, that is $900. On a $500,000 mortgage, $1,500. On an Atlanta FHA max mortgage of $688,850, it is $2,067. The guide gives you the calculation formula, a worked example table across five common loan amounts, the distinction between the intangible tax (buyer pays, based on loan) and the transfer tax (typically seller pays, based on sale price), and the July 2025 legislative update that redefined "long-term note." You stop confusing the two taxes and start calculating your exact cash-to-close before the Closing Disclosure arrives.

Georgia Dream Down Payment Navigator

The Georgia Housing and Finance Authority administers one of the Southeast's most generous assistance programs --- up to $10,000 (Standard) or $12,500 (PEN/Choice) as a zero-interest deferred second mortgage. The guide maps all three tiers against their eligibility matrices: the 640 minimum credit score, the $130,290 household income limit for Metro Atlanta (1-2 persons), the $550,000 purchase price cap, the $20,000 liquid asset ceiling, the mandatory 8-hour homebuyer education course, and the personal investment requirement ($500 to $1,000 of your own funds). You get the dual-underwriting warning --- Georgia Dream adds a second round of state-level underwriting that routinely delays closings --- and the tactical framework for making Georgia Dream offers competitive in multiple-offer markets by building extra time into the contract and providing proof of DCA pre-review.

Invest Atlanta and Municipal Programs

If you are buying within the City of Atlanta, Invest Atlanta offers some of the most competitive incentives in the state --- and most buyers do not know they exist. HOME Atlanta 4.0 provides a 3.5% fully forgivable grant at closing (max purchase price $325,000). AAHOP provides up to $20,000 forgiven after 5 to 10 years with a minimum credit score of just 580. IMAP provides $10,000 deferred. The Vine City Renaissance Initiative adds $10,000 in the 30314 zip code, forgiven after 5 years. The Perry Bolton program provides up to $20,000 in Northwest Atlanta. The Atlanta Housing Authority offers $20,000 standard or $25,000 for public safety, educators, healthcare workers, and military. In Augusta, deferred forgivable loans up to $10,000 are fully forgiven after 5 years of continuous residency. The guide maps every program with eligibility criteria, stacking rules, and the specific buyer personas they target --- so you capture assistance that the DCA website never mentions.

The GAR Contract Mechanics

Nearly every residential transaction in Georgia is governed by the Georgia Association of Realtors Purchase and Sale Agreement. The guide decodes the 2026 version: the due diligence period that functions as an option period (terminate for any reason and keep your earnest money --- but only if you do it in writing before the exact deadline), the Amendment to Address Concerns that does not pause or extend the clock (the single most expensive mistake Georgia buyers make), the new unilateral closing extension rules (Section B.4.a --- 8 days, but only for specific lender or title-curing delays), the encroachment warranty limits, the emergency extensions during governor-declared states of emergency, and the liquidated damages framework that replaced specific performance. You understand exactly when your money goes hard and what leverage you lose if the due diligence period expires without a written termination.

County-by-County Homestead Exemptions

Georgia's homestead exemption system is so fragmented that missing a single deadline can cost you hundreds to thousands of dollars per year. The guide contrasts Fulton County's floating CPI exemption (caps your assessed value to a base year --- the most valuable long-term protection in Metro Atlanta), DeKalb's H1-through-H10 tier system with its confusing income thresholds, Cobb's age-62 full school tax exemption, and Gwinnett's Value Offset Exemption that only freezes the county portion while leaving you fully exposed to school tax increases. You get the April 1 filing deadline, the filing process, and the county-by-county comparison that lets you evaluate long-term tax affordability before you choose a neighborhood --- not after you have already closed.

Termite Letters and Crawl Space Moisture

Georgia's humid subtropical climate introduces structural risks that buyers from drier states will not anticipate. The guide explains the Official Georgia Wood Infestation Inspection Report (WIIR) --- what it covers (five specific wood-destroying organisms), who pays for it, why VA and FHA lenders mandate it before funding, the 90-day warranty on a clear report, and the Georgia Structural Pest Control Commission rules governing the inspection. It then covers crawl space moisture --- why ventilated crawl spaces in Georgia's humidity lead to wood rot, mold infiltration through HVAC systems, and energy cost spikes --- and the $5,000 to $15,000 encapsulation remediation that buyers discover during inspection and must negotiate before due diligence expires. You know what to inspect, what it costs, and what to negotiate before the clock runs out.

Mortgage Financing by County

Georgia has no high-cost counties under federal housing finance guidelines, which means FHA limits fall well below the conforming limit in the Atlanta metro. The guide provides the 2026 conforming loan limit ($832,750), the FHA limit by county ($688,850 for Metro Atlanta, $541,287 floor for 125 of Georgia's 159 counties), the gap analysis showing where FHA cannot reach, VA loan strategy for Fort Moore, Fort Eisenhower, Fort Stewart, and Robins AFB, and the USDA Rural Development program covering 97% of the state's land area with zero-down financing. You pair the right financing with the right geography instead of defaulting to FHA and leaving money on the table.

Five-Market Regional Intelligence

What $350,000 buys varies dramatically across Georgia. The guide covers the Atlanta Metro ($389,900 median, fierce competition below $400,000, North Fulton tech corridor vs. South Atlanta logistics hubs), Savannah (inventory surging 29.6%, historic district regulatory overhead, coastal flood and termite risks), Columbus ($215,000 median, +10.3% year-over-year, Fort Moore BAH alignment), Augusta (medical district demand, municipal DPA programs for essential workers), and Macon ($205,995 median, +5.6%, Robins AFB proximity). Each region includes typical competition levels, dominant buyer profiles, and the specific risks that trip up first-time buyers in that market.

Step-by-Step Transaction Timeline

The full process mapped from 6 months before closing through your first 90 days of ownership: pre-approval sequencing, the 8-hour homebuyer education course timing, inspection scheduling within the due diligence window, the DCA 10-business-day compliance review for Georgia Dream buyers, Closing Disclosure verification (specifically the intangible tax line item), wire fraud prevention protocol, and the post-closing homestead exemption filing. Every critical deadline mapped with what happens if you miss it.

Standalone Printable Tools

Every paid download includes 8 standalone tools you can print and bring to your lender meeting, home inspection, or closing attorney appointment:

- Closing Attorney Reference --- who represents whom at the closing table, GAR contract key points, and earnest money timelines

- Down Payment Assistance Worksheet --- Georgia Dream tiers, Invest Atlanta grants, municipal DPA, and a fillable stacking calculator

- Intangible Tax Calculator --- the formula, five worked examples, and the transfer tax vs. intangible tax comparison

- Homestead Exemption Reference --- Fulton, DeKalb, Cobb, and Gwinnett side by side with the April 1 filing deadline

- Financing Comparison --- FHA limits by county, loan programs compared, and USDA eligibility notes

- Inspection Checklist --- WIIR, crawl space moisture, septic, well water, and every due diligence item

- Regional Market Reference --- five Georgia markets at a glance with pricing, competition, and risks

- Closing Timeline --- your 30-to-45-day roadmap from offer to keys

Who This Guide Is For

- First-time buyers in the Atlanta metro competing in the fiercely contested sub-$400,000 bracket across Fulton, DeKalb, Cobb, and Gwinnett --- who need to understand how the intangible tax, dual Georgia Dream underwriting, and county-specific homestead exemptions affect their total cost of ownership, not just the sticker price

- Military families PCSing to Fort Moore, Fort Eisenhower, Fort Stewart, or Robins AFB who have VA loan pre-approval and BAH coverage but need to navigate the Peach Select VA program, the WIIR requirement, property tax exemptions for disabled veterans, and USDA-eligible areas surrounding military installations

- Healthcare workers, educators, and first responders in Augusta, Atlanta, or Macon who qualify for stacked assistance --- Georgia Dream PEN ($12,500) plus Federal Home Loan Bank Community Partners ($20,000) plus municipal DPA ($10,000) --- but need to know how to combine them without triggering eligibility conflicts

- Out-of-state relocators moving to Georgia from states that use title companies who need to understand why national home buying advice is structurally wrong for an attorney-closing state --- and what it means that the attorney at the closing table cannot advocate for them

- Savannah and coastal buyers targeting the Historic District, Starland, or Victorian neighborhoods who face Certificate of Appropriateness requirements, preservation easements, coastal flood insurance, and termite risks that apply to new construction as much as century-old homes

- Anyone buying in suburban or rural Georgia who wants to check whether their target property falls in USDA-eligible territory --- covering 97% of the state's land area with zero-down financing that avoids the dual-underwriting delays of Georgia Dream entirely

Why Not Free Tools and Forums?

Free information on buying a home in Georgia exists. Here is what it actually delivers:

- The DCA website gives you Georgia Dream program descriptions, income limits, and a list of participating lenders. It does not explain how dual underwriting delays your closing, warn you that the mandatory 8-hour homebuyer education course becomes a bottleneck if you wait until you are under contract, show you how to stack state assistance with Invest Atlanta grants or the Augusta municipal DPA, or help you decide between Georgia Dream and USDA when both apply. You get eligibility criteria without the decision framework.

- Reddit threads (r/Atlanta, r/Georgia, r/FirstTimeHomeBuyer) contain genuine warnings about the intangible tax and Georgia Dream delays from buyers who were blindsided. But they are mixed with buyers conflating the intangible tax with the transfer tax, incorrect claims about splitting the intangible tax with the seller, outdated income limits, and advice from non-attorney-closing states that does not apply here. Sorting current from dangerous takes longer than reading a guide that already did it.

- Real estate agent and lender blogs explain what the intangible tax is. They do not give you the calculation formula, the distinction between the two taxes, the July 2025 legislative update, or the county-by-county homestead exemption comparison that determines your long-term tax exposure. Agents are incentivized to close transactions, not to help you evaluate whether Fulton's floating CPI exemption makes a $375,000 home cheaper over 15 years than a $340,000 home in Gwinnett where school taxes rise uncapped.

- National home buying guides describe escrow agents, title companies, and inspection contingencies that do not exist in Georgia. Following their advice here --- assuming a title company handles your closing, assuming you can freely extend the inspection period while negotiating repairs, assuming property taxes work like they do in Texas or Florida --- will cost you money at best and legal exposure at worst. Georgia's attorney-closing system and GAR contract mechanics are structurally incompatible with generic national advice.

This guide fills the Georgia-specific gap --- the space between knowing how to buy a home in general and knowing how to buy one in a state where the closing attorney represents the lender instead of you, an intangible recording tax adds hundreds to thousands of dollars that your Loan Estimate did not clearly disclose, the GAR contract's due diligence clock does not pause for repair negotiations, 159 counties each administer their own homestead exemptions with an unyielding April 1 deadline, and subterranean termites attack new construction as readily as century-old homes. It is the risk analysis that would take a Georgia real estate attorney, a DCA program specialist, and a licensed pest control inspector to assemble --- structured as a reference you own permanently.

--- Less Than Your Intangible Tax on a $40,000 Mortgage

A single consultation with a Georgia real estate attorney runs $200 to $400 per hour. Missing the due diligence deadline by one hour can cost you your entire earnest money deposit. Failing to file your homestead exemption by April 1 means paying full property taxes for the entire year --- in Fulton County, that can be thousands of dollars with no recourse. Not knowing how to calculate the intangible tax means discovering a $900 to $2,067 charge on your Closing Disclosure three days before closing, when it is too late to adjust your budget.

This guide does not replace your real estate agent, your lender, or your closing attorney. But it gives you the intangible tax calculator, the Georgia Dream eligibility navigator, the county-by-county homestead exemption comparison, the GAR contract timeline, and the termite and crawl space inspection framework that ensure you identify every Georgia-specific risk before your money goes hard --- instead of discovering them when you are already under contract and the due diligence clock is counting down.

If it prevents a single intangible tax surprise, catches a single homestead exemption deadline, or alerts you to crawl space remediation costs before your due diligence expires --- it pays for itself before you finish reading it.

30-day money-back guarantee. If the guide does not sharpen your Georgia home buying analysis and protect your capital, you pay nothing.

Download the free Georgia Quick-Start Home Buying Checklist to see the step-by-step framework covering pre-approval, due diligence management, inspections, and closing. When you are ready for the full intangible tax calculator, Georgia Dream navigator, county homestead comparison, and the complete 10-chapter guide, the full toolkit is here.

Georgia's attorney-closing system rewards buyers who understand it and punishes those who don't. This guide makes sure you're on the right side.